What this calculator does

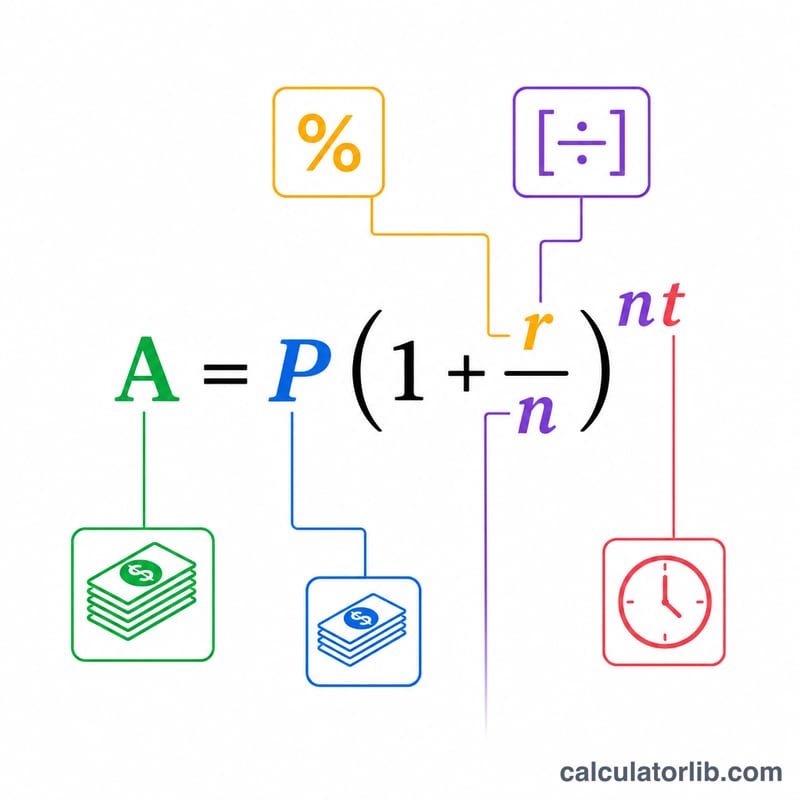

This tool computes compound interest using the standard formula \(A = P\left(1 + \frac{r}{n}\right)^{nt}\), where A is the total accrued amount, P is the principal, r is the decimal annual rate, n is the number of compounding periods per year, and t is the time in years. It also supports continuous compounding via \(A = P\,e^{rt}\). The unique feature is that you can solve for any one of four unknowns: total amount (A), principal (P), annual rate (R) or time (t).

How to use it

Pick what you want to calculate from the "Calculate:" menu. Fill in the values you know, choose a compounding frequency, and the calculator returns the unknown plus a full \(A = P + I\) breakdown. When solving for principal you may supply either the known total amount (A) or the interest earned (I). Rates are entered as a percentage and converted internally to \(r = R/100\). Currency fields accept thousands separators, which are stripped automatically.

The formula explained

For discrete compounding, the base growth factor \(\left(1 + \frac{r}{n}\right)\) is raised to the power \(nt\). Rearranging gives the other unknowns: \(P = \dfrac{A}{\left(1 + \frac{r}{n}\right)^{nt}}\); from interest, \(P = \dfrac{I}{F - 1}\) where F is the growth factor; \(R = 100 \cdot n\left(\left(\frac{A}{P}\right)^{1/(nt)} - 1\right)\); and \(t = \dfrac{\ln(A/P)}{n \cdot \ln\left(1 + \frac{r}{n}\right)}\). For continuous compounding the analogues use \(e^{rt}\), with \(r = \ln(A/P)/t\) and \(t = \ln(A/P)/r\).

Worked example

Deposit \(P = \$10{,}000\) at \(R = 3.875\%\) compounded Monthly (\(n = 12\)) for \(t = 7.5\) years. Then \(r/n = 0.0032292\), the exponent \(nt = 90\), and \((1.0032292)^{90} \approx 1.336637\). So $$A = 10{,}000 \times 1.336637 = \$13{,}366.37,$$ and interest \(I = A - P = \$3{,}366.37\).

FAQ

What does "Continuously" mean? It applies \(A = P\,e^{rt}\), the limit as compounding periods become infinitely frequent. It yields a slightly higher amount than daily compounding.

Why must A be greater than P to solve for rate or time? Because solving requires \(\ln(A/P)\), which must be positive for a real, positive answer when interest is being earned.

Is this currency-specific? No. The dollar sign is just a label; the math is universal for any currency.