What This Calculator Does

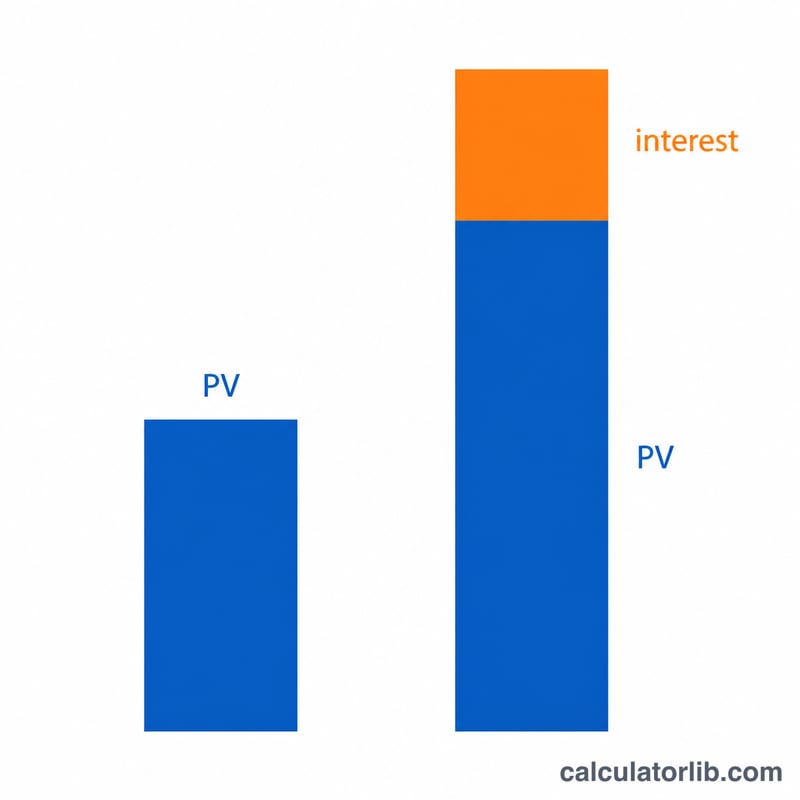

This tool computes the future value (FV) of a single present-value lump sum invested today at a constant interest rate. There are no recurring deposits or withdrawals (it is not an annuity) — just one amount left to grow. It also reports the Future Value Interest Factor (FVIF), the multiplier by which your money grows: \(FV = PV \times FVIF\).

How to Use It

Enter four values, all in consistent units:

- Present Value (PV) — the one-time amount you invest now.

- Number of Periods (t) — usually years; decimals are allowed (7.5 = 7 years 6 months).

- Interest Rate (R) — the nominal stated rate per period, as a percent.

- Compounding (m) — how many times per period interest is applied: 1 = annual, 2 = semiannual, 4 = quarterly, 12 = monthly, 365 = daily. Enter

cfor continuous compounding.

The Formula Explained

First convert the rate: \(r = R / 100\). For periodic compounding, the per-sub-period rate is \(i = r / m\) and the total number of sub-periods is \(n = m \times t\), giving \(FVIF = (1 + i)^{n}\). For continuous compounding the factor is \(e^{r \cdot t}\). In both cases \(FV = PV \times FVIF\).

$$FV = PV \left(1 + \frac{r}{m}\right)^{m \cdot t}$$

Worked Example

Invest $15,000 for 10 years at 5.25% compounded monthly. Then \(r = 0.0525\), \(i = 0.0525/12 = 0.004375\), \(n = 120\), so \(FVIF = 1.004375^{120} \approx 1.68852\) and

$$FV = 15{,}000 \times 1.68852 \approx \mathbf{\$25{,}327.86}$$With continuous compounding instead, \(FVIF = e^{0.525} \approx 1.69046\), so \(FV \approx \$25{,}356.89\).

FAQ

What is FVIF? The Future Value Interest Factor is the growth multiplier applied to your principal. An FVIF of 1.68852 means each dollar becomes about $1.69.

Can the rate be zero or negative? Yes. A rate of 0 gives \(FVIF = 1\) (\(FV = PV\)); a negative rate models depreciation.

Why does continuous compounding give more? More frequent compounding lets interest start earning interest sooner; continuous is the theoretical limit as \(m\) approaches infinity.