What Is the Future Value of a Lump Sum?

The future value (FV) of a lump sum tells you how much a single, one-time investment will be worth after a number of years once compound interest is added. Unlike a recurring deposit, here you invest once and let it grow. This calculator works for any currency — simply enter the amount in your own currency.

How to Use the Calculator

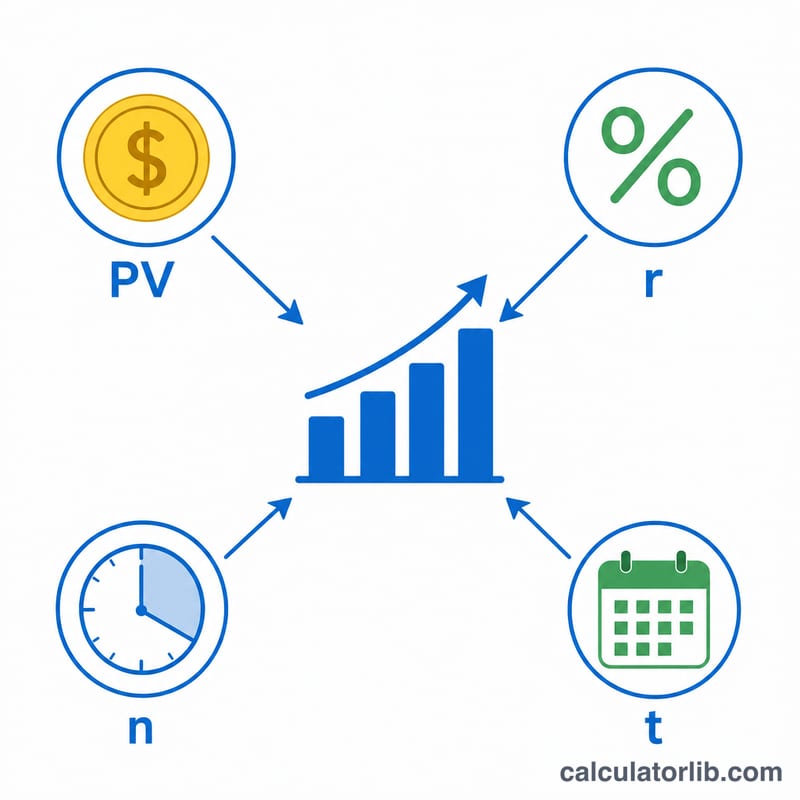

Enter your present value (the amount you invest today), the annual interest rate as a percentage, the number of years you'll stay invested, and how often interest compounds (annually, semi-annually, quarterly, monthly, or daily). The tool returns the future value plus the total interest earned.

The Formula Explained

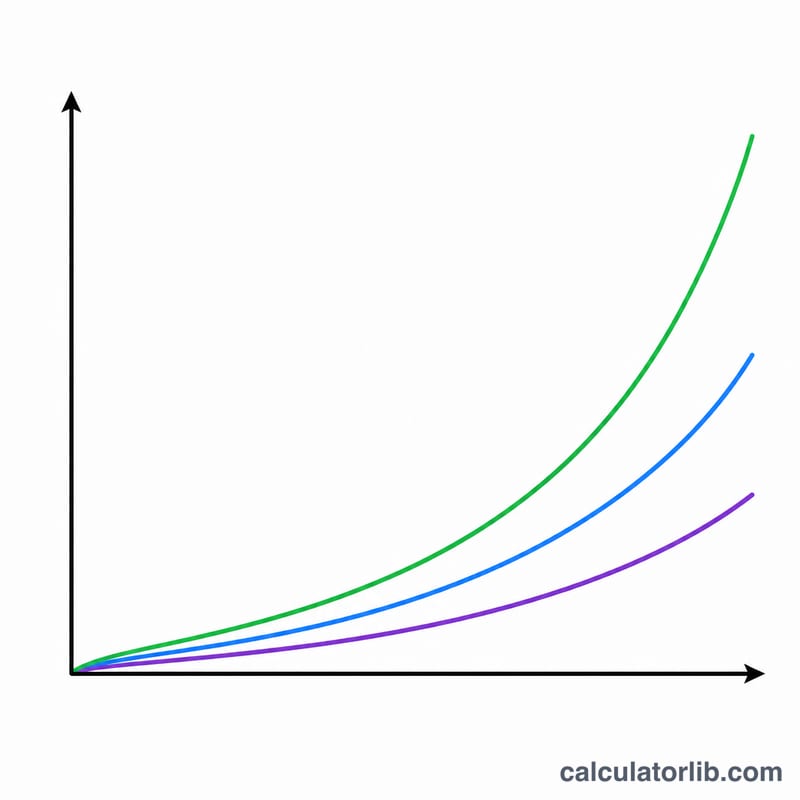

The compound interest formula is $$FV = PV \times \left(1 + \frac{r}{n}\right)^{n \cdot t}$$ Here PV is your initial amount, r is the annual rate written as a decimal (5% = 0.05), n is the number of compounding periods per year, and t is the number of years. More frequent compounding (higher \(n\)) produces a slightly larger result because interest starts earning interest sooner.

Worked Example

Suppose you invest 10,000 at a 5% annual rate, compounded monthly, for 10 years. Then \(r = 0.05\), \(n = 12\), \(t = 10\). $$FV = 10{,}000 \times \left(1 + \frac{0.05}{12}\right)^{120} \approx 10{,}000 \times 1.6470 \approx 16{,}470.09$$ The total interest earned is about 6,470.09.

FAQ

Does compounding frequency really matter? Yes, but the effect is modest. The same 5% rate over 10 years grows 10,000 to about 16,289 annually versus 16,470 monthly.

What rate should I use? Use the expected annual return of your investment. Savings accounts, bonds, and stocks all differ — be conservative for long-term planning.

Is inflation included? No. The result is in nominal terms. To estimate real (inflation-adjusted) value, subtract your expected inflation rate from the interest rate.