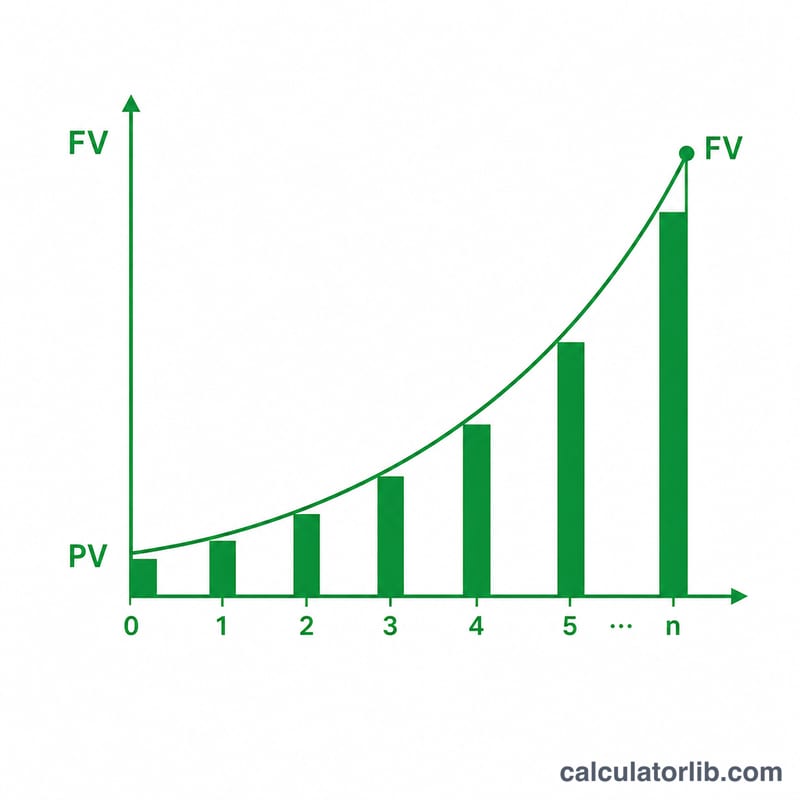

What Is the Appreciation Calculator?

The Appreciation Calculator estimates how much an asset will be worth in the future when it grows in value at a steady annual rate. Appreciation is the opposite of depreciation — instead of losing value, the asset gains value over time. This tool applies compound growth, so each year's gain is calculated on the previous year's total value. It works for real estate, collectibles, fine art, land, stocks, and any asset you expect to rise in value.

How to Use It

Enter three values: the present value of the asset, the expected annual appreciation rate as a percentage, and the number of years you plan to hold it. The calculator returns the projected future value plus the total gain. You can use fractional years (for example, 2.5) and any rate you expect for your market.

The Formula Explained

The core equation is $$FV = PV \times (1 + r)^{n}$$ where PV is the present value, r is the annual rate expressed as a decimal (5% = 0.05), and n is the number of years. Raising \((1 + r)\) to the power of \(n\) captures compounding — value builds on top of value each year.

Worked Example

Suppose you buy a property for $250,000 and expect it to appreciate 4% per year for 8 years. Then $$FV = 250{,}000 \times (1.04)^{8} = 250{,}000 \times 1.36857 \approx \$342{,}142.$$ The total gain is about $92,142. That extra value comes purely from the assumed appreciation rate compounding annually.

Interpreting Your Result

The number this calculator returns is a nominal projection that assumes one constant appreciation rate compounded every year. It answers a simple "what if" question: if the asset grew at exactly this rate each year, what would it be worth after the chosen number of years? It is a mathematical model, not a forecast.

Real markets do not move at a constant rate. Actual asset prices rise and fall year to year, sometimes sharply. A constant-rate projection smooths over that volatility, so the path your asset actually takes will almost certainly differ from the smooth curve implied here, even if the long-run average eventually matches your assumed rate. Because the formula compounds, errors in the rate or the time horizon grow larger the further out you project.

Nominal versus inflation-adjusted (real) value. The result is a nominal figure expressed in future dollars. If general prices also rise over the period, the future amount buys less than the same number of dollars today. To gauge purchasing power, compare the projected value against an inflation estimate for the same period; the real (inflation-adjusted) gain is what remains after subtracting the effect of inflation. For example, an asset that appreciates 4% per year while inflation runs near 3% per year has gained far less in real terms than the nominal figure suggests.

Gains shown here exclude taxes, fees, and carrying costs. The projection is gross appreciation only. It does not account for capital gains tax on a sale, transaction or brokerage costs, ongoing expenses such as property taxes, insurance, storage, or maintenance, or any income the asset might produce (such as rent or dividends). Net proceeds after those items can be substantially lower than the headline future value, and for income-producing assets the price-appreciation figure alone understates total return.

This section is general educational information about how the calculation works, not personalized financial advice.

FAQ

Is appreciation guaranteed? No. The calculator assumes a fixed rate, but real markets fluctuate. Use a conservative estimate for planning.

Does it account for inflation or fees? No. It shows nominal value only. Subtract expected inflation from your rate to estimate real (inflation-adjusted) growth.

Can I use it for any currency? Yes. The math is currency-agnostic — the future value is in the same currency you enter for present value.