What Is a Mortgage Payoff Calculator?

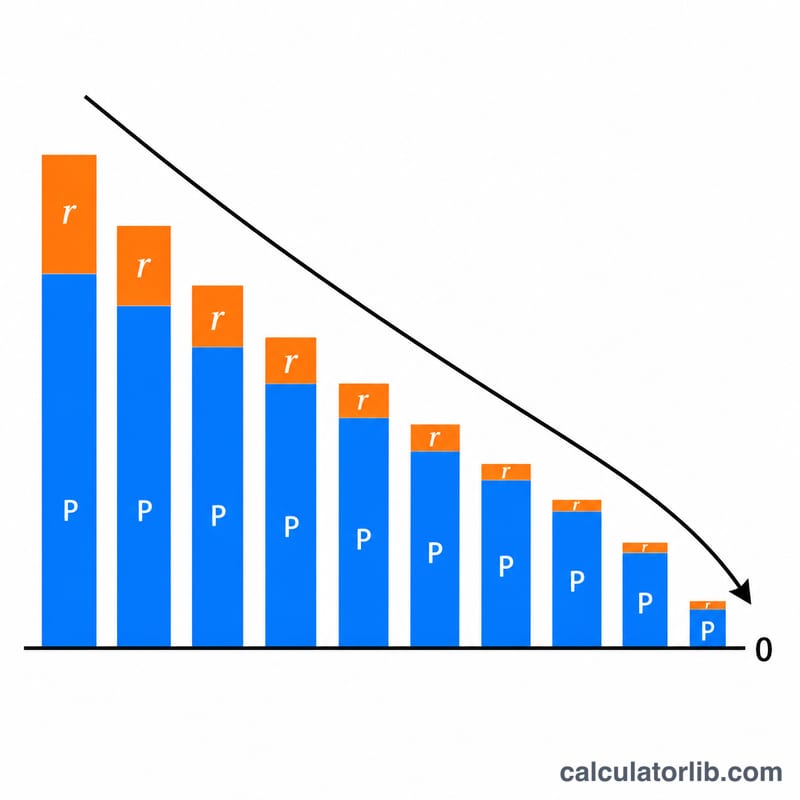

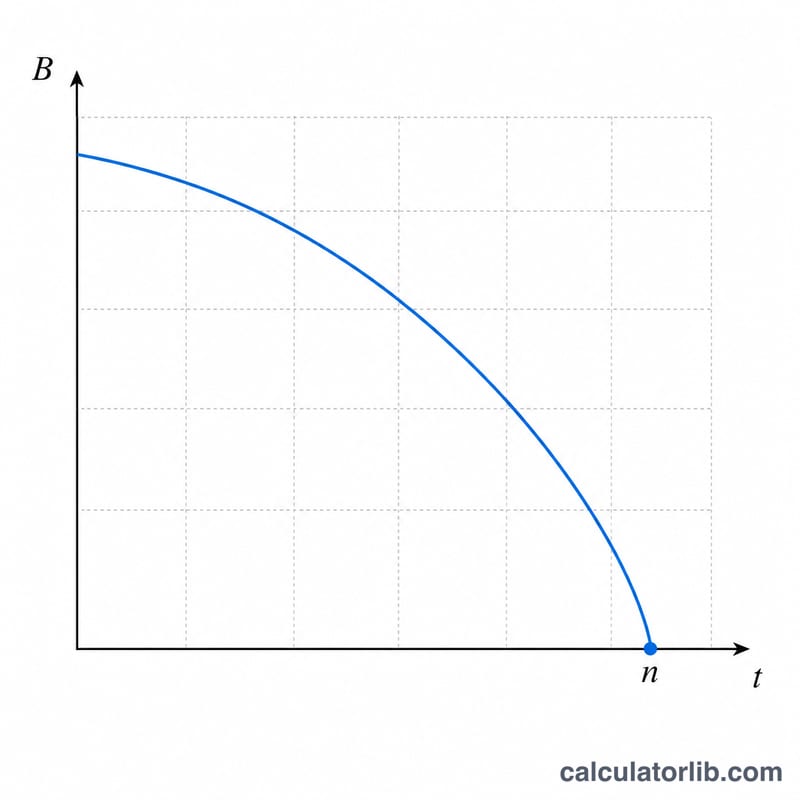

A mortgage payoff calculator tells you how long it will take to fully repay your home loan given your current balance, your annual interest rate, and the fixed monthly payment you make. Instead of waiting decades to find out, you can instantly see the number of months and years remaining, along with the total amount and total interest you'll pay over the life of the loan.

How to Use It

Enter three values: your current loan balance (the principal you still owe), your annual interest rate as a percentage, and your fixed monthly payment. The calculator returns the exact number of months to payoff (rounded up to whole months), the equivalent years, the total you will pay, and the total interest portion. Increasing your monthly payment is the fastest way to shorten the timeline.

The Formula Explained

The payoff time comes from the amortization equation solved for the number of payments:

$$n = \frac{-\ln\left(1 - \frac{P \cdot r}{PMT}\right)}{\ln(1 + r)}$$

Here P is the principal balance, PMT is the monthly payment, and \(r\) is the monthly interest rate, equal to the annual rate divided by 12 (and by 100 to convert from a percent). If your monthly payment is less than or equal to one month of interest (\(P \cdot r\)), the loan can never be repaid and the logarithm is undefined — the calculator flags this.

Worked Example

Suppose you owe $200,000 at 6% annual interest and pay $1,500 per month. The monthly rate is \(r = 0.06 / 12 = 0.005\). Then \(P \cdot r = 1{,}000\), and \((P \cdot r)/PMT = 1{,}000 / 1{,}500 = 0.6667\). So $$n = \frac{-\ln(1 - 0.6667)}{\ln(1.005)} = \frac{-\ln(0.3333)}{0.0049875} \approx \frac{1.0986}{0.0049875} \approx 220.3 \text{ months}$$ or about 18.4 years.

FAQ

Why does my payment have to exceed the interest? If a payment only covers interest, none of it reduces the principal, so the balance never falls and the loan is never repaid.

Does this include taxes and insurance? No — enter only the principal-and-interest portion of your payment for an accurate payoff estimate.

How can I pay off faster? Raise your monthly payment or make extra principal payments; even small increases can cut years off the timeline.