What Is a Retirement Paycheck Calculator?

A retirement paycheck calculator turns a lump-sum savings balance into a steady monthly income stream. It answers the question many retirees ask: "If I have a certain amount saved, how much can I pay myself each month so the money lasts a fixed number of years while still earning interest?" The calculation uses the standard amortizing-annuity formula — the same math that powers loan payments, run in reverse to drain a balance.

How to Use It

Enter three values: your total retirement savings balance, the annual return rate you expect your investments to earn during retirement, and the number of years you want the income to last. The tool returns your sustainable monthly paycheck, the equivalent annual income, the total amount paid out over the period, and how much of that came from interest growth.

The Formula Explained

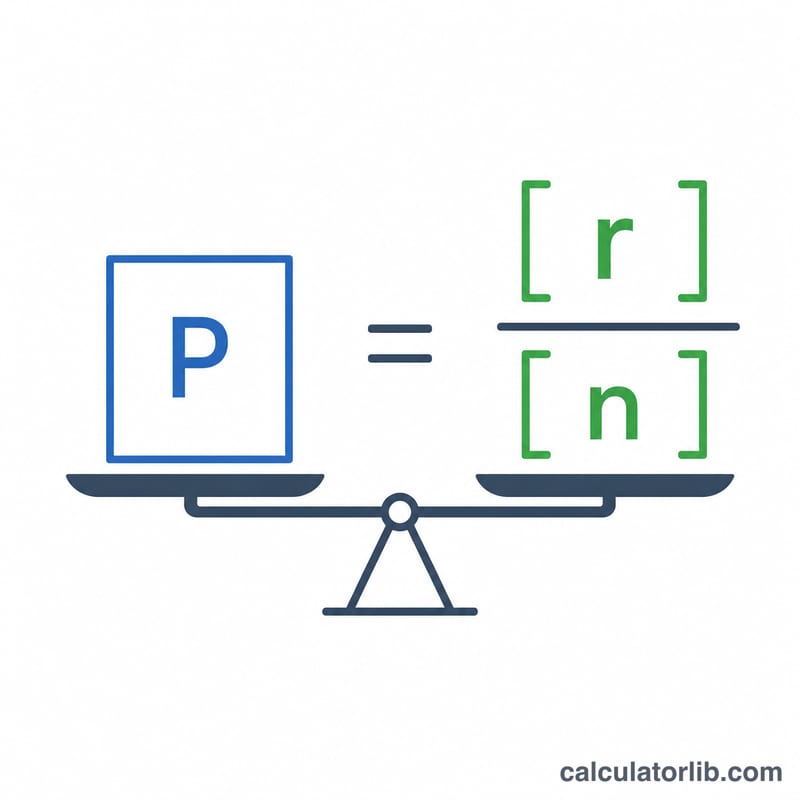

The monthly payment is

$$PMT = P \times \frac{r/12}{1 - (1 + r/12)^{-n}}$$where \(P\) is the principal, \(r\) is the annual rate as a decimal, and \(n\) is the number of months (years \(\times\) 12). The \(r/12\) term is the monthly interest rate; the denominator discounts all future payments back to present value. If the rate is 0%, the formula simplifies to \(P \div n\).

Worked Example

Suppose you retire with $500,000, expect a 5% annual return, and want income for 25 years. Then \(i = 0.05/12 \approx 0.0041667\) and \(n = 300\).

$$PMT = 500{,}000 \times \frac{0.0041667}{1 - 1.0041667^{-300}} \approx \$2{,}922.95 \text{ per month}$$or about $35,075 per year. Over 25 years you'd withdraw roughly $876,886 — meaning interest contributed nearly $377,000.

FAQ

Does this account for inflation? No. It assumes a constant payment in today's dollars. To preserve purchasing power, use a lower "real" return rate (expected return minus inflation).

What happens at the end of the period? The balance reaches zero — this is a full payout (annuity-style) calculation, not a perpetual withdrawal.

Is the return rate guaranteed? No. Actual market returns vary year to year. Treat the result as a planning estimate, not a promise.