What Is a Loan Prequalification Calculator?

A loan prequalification calculator gives you an early, rough estimate of how large a loan you might be approved for before you formally apply. It works by translating your income and existing debt obligations into an affordable monthly payment, then converting that payment into a loan principal using standard amortization math. Lenders commonly use a debt-to-income (DTI) ratio as the central guardrail, so this tool puts that same logic in your hands.

How to Use It

Enter your gross monthly income (before taxes), your existing monthly debt payments (credit cards, car loans, student loans, etc.), the maximum DTI ratio you want to assume (lenders often cap around 36–43%), the annual interest rate, and the loan term in years. The calculator shows the maximum loan amount, the monthly payment available for the new loan, and the total interest you would pay over the full term.

The Formula Explained

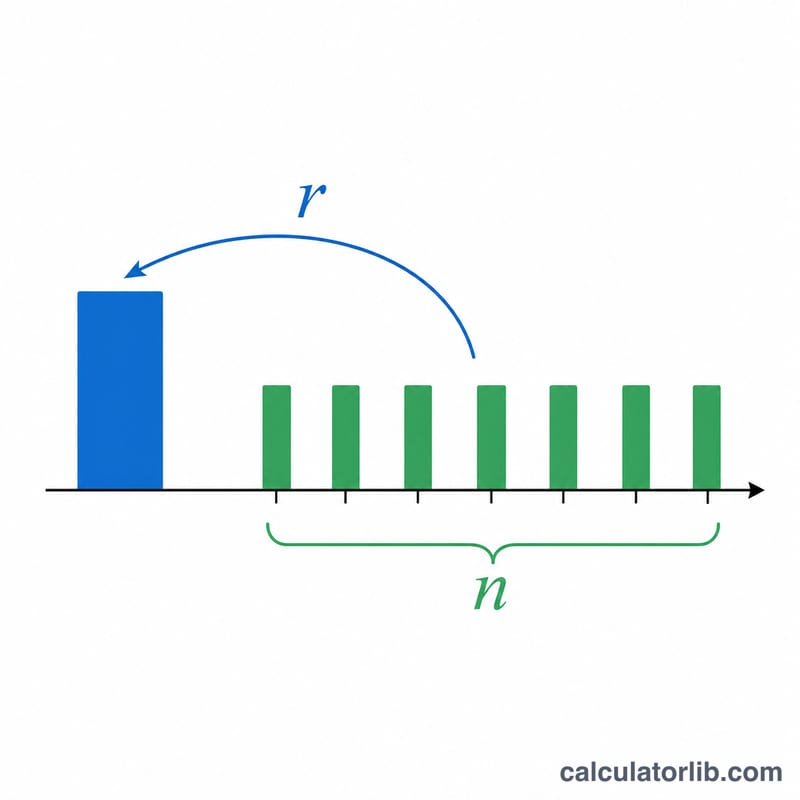

First, the maximum total monthly payment is your income multiplied by the DTI ratio. Subtracting existing debts leaves the payment available for the new loan. That payment is then run through the present-value-of-an-annuity formula: $$\text{MaxLoan} = \text{MaxPayment} \cdot \frac{1-(1+r)^{-n}}{r}$$ where \(r\) is the monthly interest rate (annual rate \(\div\) 12 \(\div\) 100) and \(n\) is the number of monthly payments (years \(\times\) 12).

Worked Example

Suppose your gross monthly income is $6,000, you have $500 in existing debts, and you use a 36% DTI. Your maximum total payment is $2,160, leaving $1,660 for the new loan. At 6.5% over 30 years (\(r = 0.0054167\), \(n = 360\)), the maximum loan is about $262,600.

FAQ

Is prequalification the same as approval? No. Prequalification is an informal estimate; final approval depends on credit score, documentation, and the lender's full underwriting.

What DTI should I use? Many lenders prefer total DTI at or below 36%, though some allow up to 43% or higher with strong credit.

Why subtract existing debts? Lenders look at your total obligations. Existing payments reduce how much of your DTI capacity is free for a new loan.