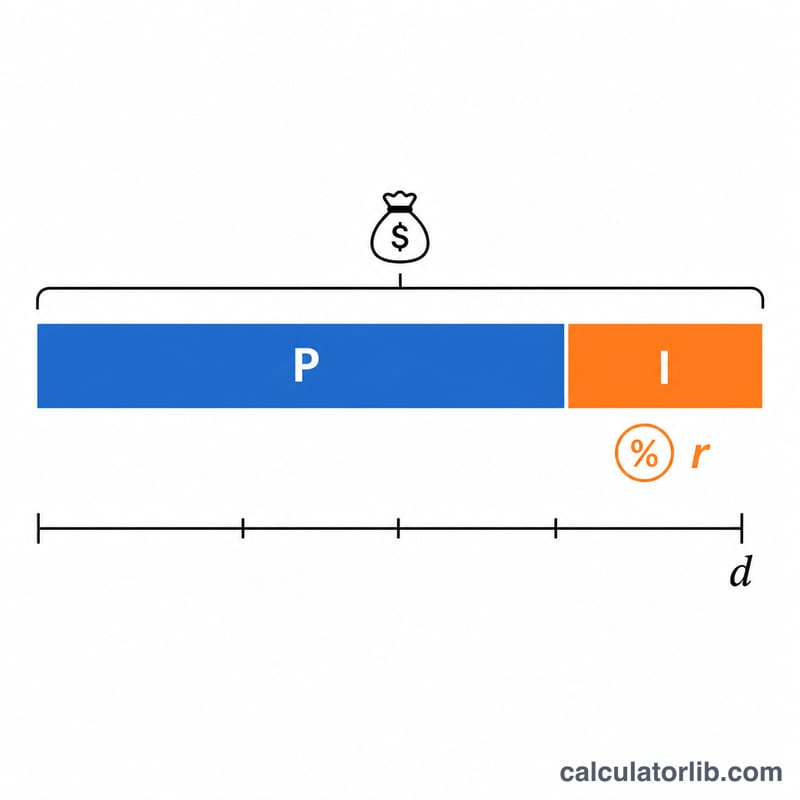

What Is a Simple Interest Loan Payoff?

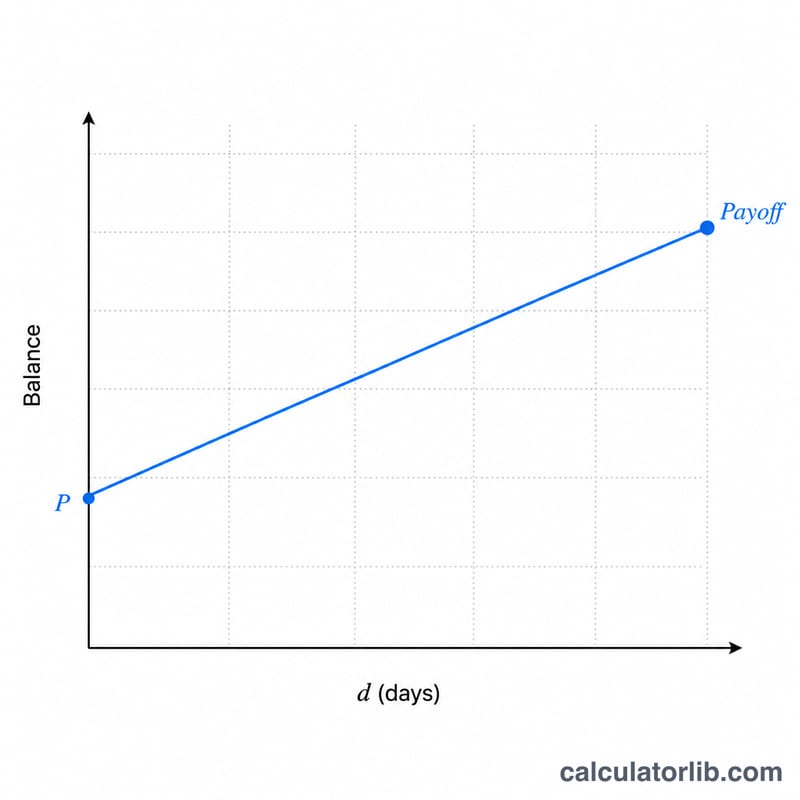

Many auto loans, personal loans, and short-term notes use simple interest, where interest accrues daily on the outstanding principal rather than compounding. Because interest is calculated on the principal only, the amount you owe to pay off the loan on a given day equals your current balance plus the interest that has built up since your last payment.

How to Use This Calculator

Enter three values: your current principal balance, the loan's annual interest rate (APR as a percent), and the number of days until you intend to pay it off. The calculator returns the accrued interest, the daily interest cost, and your total payoff amount.

The Formula Explained

Daily interest is the annual rate divided by 365, multiplied by the principal. Over \(d\) days:

$$\text{Interest} = \text{Principal} \times \left(\frac{\text{rate}}{365}\right) \times \text{days}$$

$$\text{Payoff} = \text{Principal} + \text{Interest}$$

This uses a 365-day year convention, which is common for U.S. consumer loans. Some lenders use 360 days, so verify your loan agreement for exact figures.

Worked Example

Suppose you owe $10,000 at a 6% annual rate and want to pay it off in 90 days. The daily rate is \(0.06 \div 365 = 0.00016438\). \(\text{Interest} = 10{,}000 \times 0.00016438 \times 90 = \) $147.95. Your payoff amount is \(10{,}000 + 147.95 = \) $10,147.95, with about $1.64 in interest accruing each day.

FAQ

Does simple interest compound? No. Simple interest accrues only on the principal, so it does not earn interest on previously accrued interest.

Why does the day count matter so much? Because interest accrues daily, paying off even a few days earlier reduces your total cost by the daily interest amount.

Is this the same as my loan's official payoff quote? It's an estimate. Your lender may use a 360-day year, add fees, or include unpaid prior interest, so request an official payoff statement before sending final funds.