What this calculator does

The Extra Payment Loan Payoff Calculator shows how paying a little more each month accelerates your loan payoff and lowers the total interest you pay. It compares your current loan to a new scenario and reports the change in months, monthly payment and total interest. It works for any standard amortizing loan with monthly compounding — auto loans, personal loans, student loans and mortgages — in any single currency.

How to use it

Pick a mode. In Make Extra Loan Payments, enter how much extra you will add each month and the tool solves for the new, shorter term and the interest you save. In Reduce Loan Term, enter a desired number of months and the tool solves for the payment required to hit that term. Then fill in your current balance, annual interest rate (as a percent) and your current monthly payment.

The formula explained

The monthly rate is \(i = \text{annual rate} / 100 / 12\). The number of payments to fully amortize a balance is $$n = \dfrac{-\ln\!\left(1 - \dfrac{PV \cdot i}{PMT}\right)}{\ln(1 + i)}$$ The payment must exceed the first month's interest (\(PMT > PV \cdot i\)), or the balance never falls. Total interest is found by simulating the loan month by month — each month interest equals the balance times \(i\), the rest of the payment reduces principal, and the final payment is trimmed so the balance lands exactly on zero.

Worked example

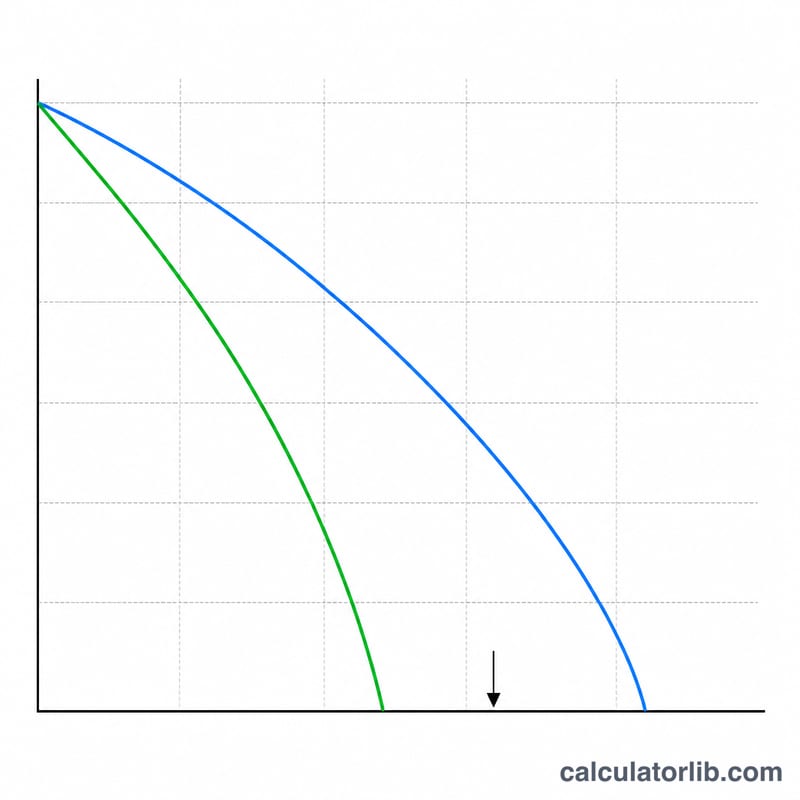

Balance $25,000, rate 3.125%, current payment $550, extra $200. The monthly rate is \(0.0026042\). At $550 the loan takes about 48 months with roughly $1,642 of interest. At $750 it takes about 35 months with roughly $1,186 of interest. That is 13 fewer months (about 1 year 1 month) and about $456 saved in interest.

FAQ

Why does the term round to a whole month? The exact number of payments is usually fractional; the realized term is the nearest whole month, with the last payment slightly smaller.

Why might totals differ a few dollars from other tools? Interest is simulated month by month, so it captures the partial final payment more precisely than a closed-form estimate.

What if my payment is too small? If the payment is at or below the first month's interest, the loan can never be paid off and the calculator tells you so.