What this calculator does

The After-Tax Savings Interest Calculator shows how much of your savings interest you actually keep once income tax is taken out. In most countries interest from savings accounts, CDs, and money-market accounts is taxable as ordinary income, so the headline rate your bank advertises is not the rate you really earn. This tool converts a gross interest rate into a net, after-tax figure.

How to use it

Enter three values: your savings balance (principal), the annual interest rate your account pays, and your marginal tax rate (the percentage of each extra dollar of income that goes to tax). The calculator returns the after-tax interest you would earn in one year, plus your gross interest, the tax owed, and your effective after-tax rate.

The formula explained

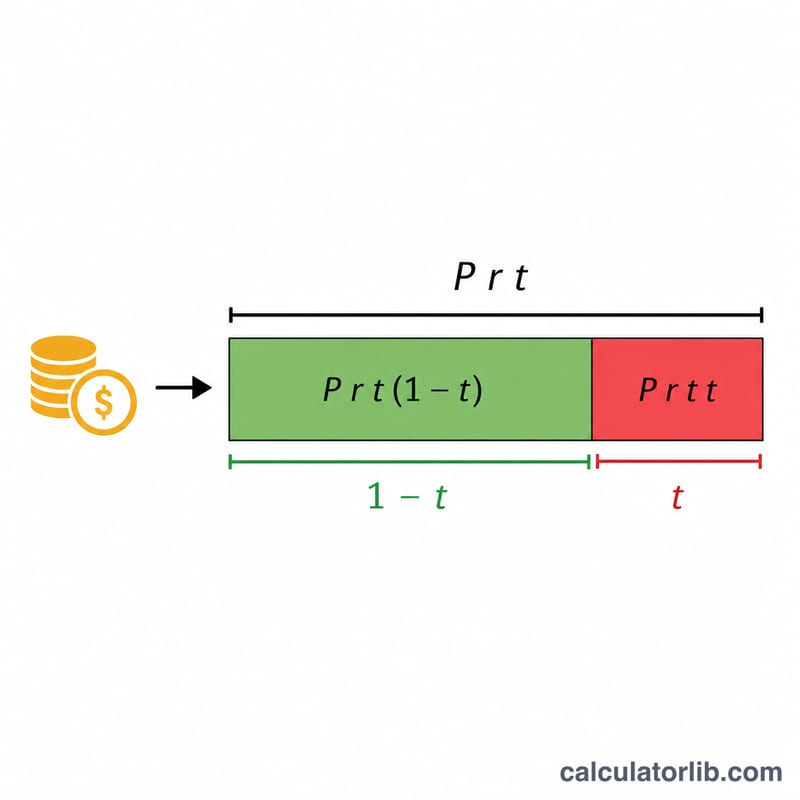

Gross annual interest is simply principal × rate. Because that interest is taxed, you keep only the portion left after tax: multiply by (1 − tax rate). The same logic applies to the rate itself, giving an effective after-tax rate of rate × (1 − tax rate). This is a one-year, simple-interest estimate and does not compound.

$$I_{net} = P \times r \times (1 - t)$$The effective after-tax rate is:

$$r_{net} = r \times (1 - t)$$

Worked example

Suppose you have $10,000 earning 5% per year and your marginal tax rate is 22%. Gross interest is \(\$10{,}000 \times 0.05 = \$500\). Tax owed is \(\$500 \times 0.22 = \$110\). After-tax interest is

$$\$500 \times (1 - 0.22) = \$390$$and your effective after-tax rate is

$$5\% \times 0.78 = 3.9\%$$

After-Tax Interest Across Different Scenarios

The table below shows how the same balance can leave you with very different amounts of usable interest once income tax is applied. Each row uses the formula \(\text{Net} = P \times \frac{r}{100} \times \left(1 - \frac{t}{100}\right)\), where \(P\) is the principal, \(r\) the gross annual rate, and \(t\) the marginal tax rate. The effective after-tax rate is simply \(r \times (1 - t/100)\).

| Principal | Gross rate | Tax rate | Gross interest (1 yr) | Tax owed | Net interest | Effective after-tax rate |

|---|---|---|---|---|---|---|

| $5,000 | 3% | 0% | $150.00 | $0.00 | $150.00 | 3.00% |

| $5,000 | 4.5% | 22% | $225.00 | $49.50 | $175.50 | 3.51% |

| $10,000 | 3% | 22% | $300.00 | $66.00 | $234.00 | 2.34% |

| $10,000 | 5% | 35% | $500.00 | $175.00 | $325.00 | 3.25% |

| $50,000 | 4.5% | 22% | $2,250.00 | $495.00 | $1,755.00 | 3.51% |

| $50,000 | 5% | 35% | $2,500.00 | $875.00 | $1,625.00 | 3.25% |

Notice that the effective after-tax rate depends only on the gross rate and the tax rate — not on the size of the balance. A 4.5% account in a 22% bracket always nets 3.51%, whether you hold $5,000 or $50,000.

Key Terms Defined

- Principal — the amount of money in the account that earns interest. In this calculator it is the starting balance over the period being measured.

- Gross (nominal) rate — the stated annual interest rate the bank advertises, before any tax is deducted. A $10,000 balance at a 4% gross rate earns $400 in gross interest over a year.

- Marginal tax rate — the tax rate applied to your next dollar of income, i.e. the rate of your highest tax bracket. Savings interest is generally taxed at this marginal rate because it stacks on top of your other income.

- Net interest — the interest you actually keep after income tax: \(\text{gross interest} \times (1 - t/100)\).

- Effective after-tax rate — the gross rate reduced by tax, \(r \times (1 - t/100)\). It expresses your real yield as a percentage so you can compare accounts on an equal footing.

- Marginal vs. effective tax rate — the marginal rate is the rate on your last dollar (the relevant one for taxing additional interest), while the effective rate is total tax divided by total income (always lower than the marginal rate in a progressive system). This calculator uses the marginal rate because interest is taxed at the top of your income.

Interpreting Your Result

The effective after-tax rate is the single most useful number this calculator produces. It tells you the true percentage yield your money earns once the tax authority takes its share. For example, a 5% account in a 35% bracket has an effective after-tax rate of only \(5 \times (1 - 0.35) = 3.25\%\) — roughly the same as a 4.5% account taxed at 22%.

Comparing accounts. Always compare the after-tax rates, not the headline gross rates. An account paying a higher gross rate can leave you with less if it is taxed at a higher marginal rate, though for most people all savings interest is taxed at the same marginal rate, so the highest gross rate usually still wins.

Comparing to inflation. To know whether your savings are gaining or losing purchasing power, compare the effective after-tax rate to inflation. If inflation is 3% and your after-tax rate is 2.34%, your money is losing real value even though the balance is growing in nominal terms.

Higher brackets keep less. Because interest is taxed at your marginal rate, the same account is worth more to a saver in a 0% bracket than to one in a 35% bracket. As your taxable income rises into higher brackets, each dollar of interest is worth less after tax.

Tax-free allowances change the picture. Interest earned inside a tax-sheltered account — such as a UK ISA, a Canadian TFSA, or a US Roth account — is typically not subject to income tax, so the effective after-tax rate equals the gross rate. Many countries also offer a personal savings allowance that shields a band of interest from tax entirely. Where these apply, set the tax rate to 0% (or to the rate on only the taxable portion) to reflect your situation.

This is general information for educational purposes, not professional financial or tax advice. Tax rules and allowances vary by country and by individual circumstances; consult a qualified adviser for guidance specific to you.

FAQ

Is this just for the US? No. The math is universal — just use whatever marginal tax rate applies to interest income in your country. Some places have tax-free savings allowances; if your interest is tax-free, enter 0%.

Does it account for compounding? No. It estimates one year of simple interest. For multi-year growth, reinvest the after-tax interest each year.

What tax rate should I enter? Use your marginal (top) rate, since interest is added on top of your other income and taxed at the highest bracket it falls into.