What Is Bank Reconciliation?

Bank reconciliation is the process of matching the cash balance on your bank statement to the balance in your accounting records (the book or ledger balance). Differences arise from timing and items one party has recorded but the other has not. This calculator adjusts both sides and tells you whether they reconcile.

How to Use It

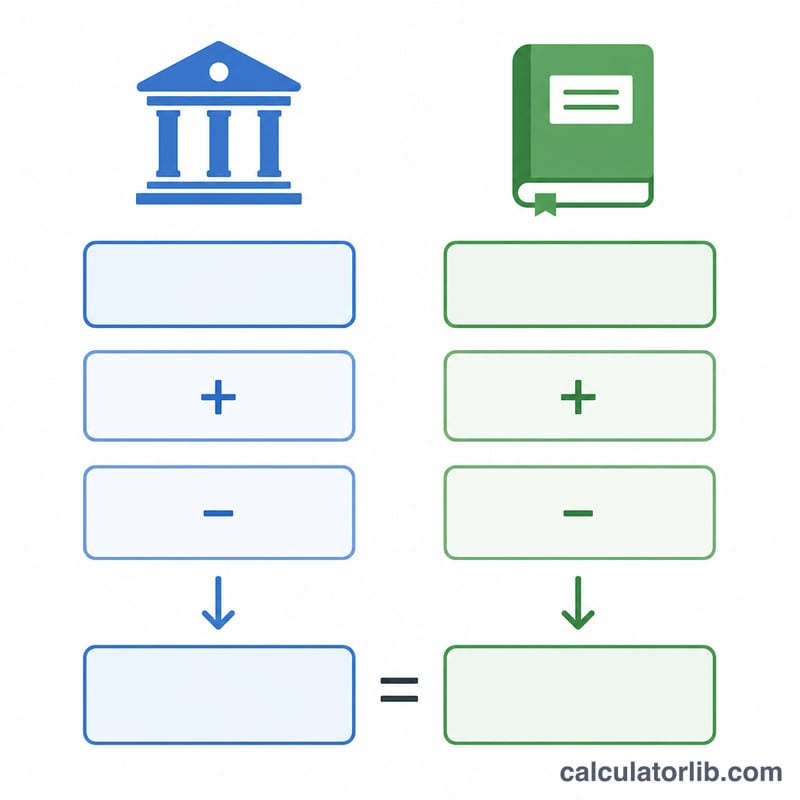

Enter your bank statement balance and your book balance. Then add the reconciling items: deposits in transit (recorded by you but not yet by the bank) and outstanding checks (written but not yet cleared) adjust the bank side; interest earned, service charges, and NSF/returned checks adjust the book side. When the two adjusted balances are equal, your accounts are reconciled.

The Formula Explained

$$\text{Adjusted Bank} = \text{Bank Balance} + \text{Deposits in Transit} - \text{Outstanding Checks}$$ $$\text{Adjusted Book} = \text{Book Balance} + \text{Interest} - \text{Service Charges} - \text{NSF}$$ The accounts reconcile when Adjusted Bank equals Adjusted Book (difference of zero).

Worked Example

Bank balance $10,000, deposits in transit $1,500, outstanding checks $2,000 → $$\text{Adjusted Bank} = 10{,}000 + 1{,}500 - 2{,}000 = \$9{,}500$$ Book balance $9,450, interest $50, no fees → $$\text{Adjusted Book} = 9{,}450 + 50 = \$9{,}500$$ The difference is $0, so the accounts are reconciled.

Where Each Reconciling Item Belongs

Bank reconciliation adjusts two starting figures — the bank statement balance and your book (ledger) balance — until both arrive at the same true cash balance. Each reconciling item belongs to exactly one side, and adds to or subtracts from it. The general rules are summarized below.

| Reconciling item | Side adjusted | Sign | Why |

|---|---|---|---|

| Deposits in transit | Bank | + | You recorded the deposit; the bank has not yet credited it. |

| Outstanding checks | Bank | − | You recorded the payment; the check has not yet cleared the bank. |

| Interest earned | Book | + | The bank paid interest you have not yet recorded. |

| Service charges / bank fees | Book | − | The bank deducted a fee you have not yet recorded. |

| NSF (returned) checks | Book | − | A deposited check bounced; the bank reversed it but your books still show it. |

| Bank error | Bank | + or − | Correct the bank side toward the true amount until the bank fixes it. |

| Book error | Book | + or − | Correct your ledger toward the true amount of the mis-recorded entry. |

The bank side follows \(\text{Adjusted Bank} = \text{Bank} + \text{Deposits in Transit} - \text{Outstanding Checks}\), while the book side follows \(\text{Adjusted Book} = \text{Book} + \text{Interest} - \text{Service Charges} - \text{NSF}\). When the two adjusted figures match, the account is reconciled.

Key Terms Defined

- Book (ledger) balance

- The cash balance according to your own records — your check register, accounting software, or general ledger — before reconciling adjustments.

- Bank statement balance

- The ending cash balance the bank reports for the period, reflecting only transactions the bank has already processed.

- Deposit in transit

- Money you have received and recorded as a deposit but that the bank had not yet credited as of the statement date. Added to the bank side.

- Outstanding check

- A check you have written and recorded that the payee has not yet cashed, so it has not cleared the bank. Subtracted from the bank side.

- Interest earned

- Interest the bank credited to the account that you have not yet entered in your books. Added to the book side.

- Service charge

- A bank fee — monthly maintenance, wire, or overdraft charge — deducted by the bank but not yet recorded in your books. Subtracted from the book side.

- NSF (returned) check

- A “non-sufficient funds” check you deposited that the payer’s bank refused to honor. The bank reverses the credit, so it is subtracted from the book side.

- Adjusted balance

- The corrected cash figure each side reaches after applying all reconciling items. When the adjusted bank balance equals the adjusted book balance, the account is reconciled.

Interpreting Your Result

The calculator compares your adjusted bank balance with your adjusted book balance and reports the difference between them.

Difference of $0 — reconciled. When the two adjusted balances are equal, every recorded transaction is accounted for on both sides and the account is reconciled. For example, a bank balance of $5,000 with $1,200 in deposits in transit and $700 in outstanding checks gives an adjusted bank balance of $5,500. If the adjusted book balance also equals $5,500, the difference is $0 and you are done.

A non-zero difference — something is missing or wrong. A remaining difference means at least one reconciling item is unrecorded, entered on the wrong side, or recorded with the wrong amount or sign. It does not by itself reveal which side is at fault, only that the two views of cash disagree.

When the difference is not zero, recheck the following, roughly in order of how often they cause discrepancies:

- Outstanding checks and deposits in transit — confirm each timing item is included once and on the bank side.

- Interest, service charges, and NSF items — verify these bank-initiated entries were posted to your books on the correct side.

- Transposition errors — if the difference is evenly divisible by 9 (for example $90, $270, or $810), digits may have been swapped, such as entering 54 as 45.

- Doubled or omitted entries — if the difference equals the exact amount of a known transaction, that item may be recorded twice or not at all.

- Sign errors — an item added where it should be subtracted creates a difference equal to twice that item’s amount.

This is general educational information about the reconciliation process, not financial or accounting advice. For account-specific concerns, consult your financial institution or a qualified accountant.

FAQ

Why don't my balances match initially? Timing differences (uncleared checks/deposits) and bank-only items (fees, interest) cause temporary gaps that the reconciliation removes.

What if there's still a difference? A non-zero difference signals a missing item or an error — recheck your deposits in transit, outstanding checks, and any fees.

Are NSF checks added or subtracted? NSF (non-sufficient funds) checks are subtracted from the book balance because the deposit you recorded did not actually clear.