What Is the Break-Even Point (Revenue)?

The break-even point in revenue is the amount of sales dollars a business must generate to cover all of its costs — both fixed and variable — so that profit is exactly zero. Below this point you lose money; above it, every additional dollar of sales contributes to profit. Expressing break-even in revenue (rather than units) is especially useful for businesses that sell many different products or services, because it works directly with overall margins.

How to Use This Calculator

Enter three numbers: your total fixed costs for the period (rent, salaries, insurance, etc.), the selling price per unit, and the variable cost per unit (materials, commissions, shipping). The calculator computes your contribution margin per unit, your contribution margin ratio, and the break-even sales revenue, plus the equivalent number of units.

The Formula Explained

First, the contribution margin ratio is found as (Price − Variable Cost) ÷ Price. This tells you what fraction of every sales dollar is available to cover fixed costs. Then break-even revenue is simply Fixed Costs ÷ Contribution Margin Ratio. The higher your margin ratio, the fewer sales dollars you need to break even.

Worked Example

Suppose fixed costs are $50,000, the price per unit is $40, and the variable cost is $24. The contribution margin is $40 − $24 = $16, giving a CM ratio of 16 ÷ 40 = 0.40 (40%). Break-even revenue = $50,000 ÷ 0.40 = $125,000. That equals $125,000 ÷ $40 = 3,125 units.

Break-Even Across Different Scenarios

The table below compares several illustrative businesses. Break-even revenue is found by dividing fixed costs by the contribution margin (CM) ratio, and break-even units are found by dividing fixed costs by the contribution margin per unit. For these examples we assume a selling price of \(\$100\) per unit so the contribution margin per unit equals the CM ratio multiplied by \(\$100\).

| Business | Fixed Costs | CM Ratio | CM per Unit (at $100 price) | Break-Even Revenue | Break-Even Units |

|---|---|---|---|---|---|

| Lean service firm | $20,000 | 60% | $60 | $33,333 | 333 |

| Boutique retailer | $50,000 | 40% | $40 | $125,000 | 1,250 |

| Light manufacturer | $100,000 | 40% | $40 | $250,000 | 2,500 |

| Low-margin distributor | $100,000 | 20% | $20 | $500,000 | 5,000 |

Notice how the low-margin distributor needs four times the sales revenue of the lean service firm to break even, even though its fixed costs are only five times larger — a thinner contribution margin dramatically raises the sales required to cover costs.

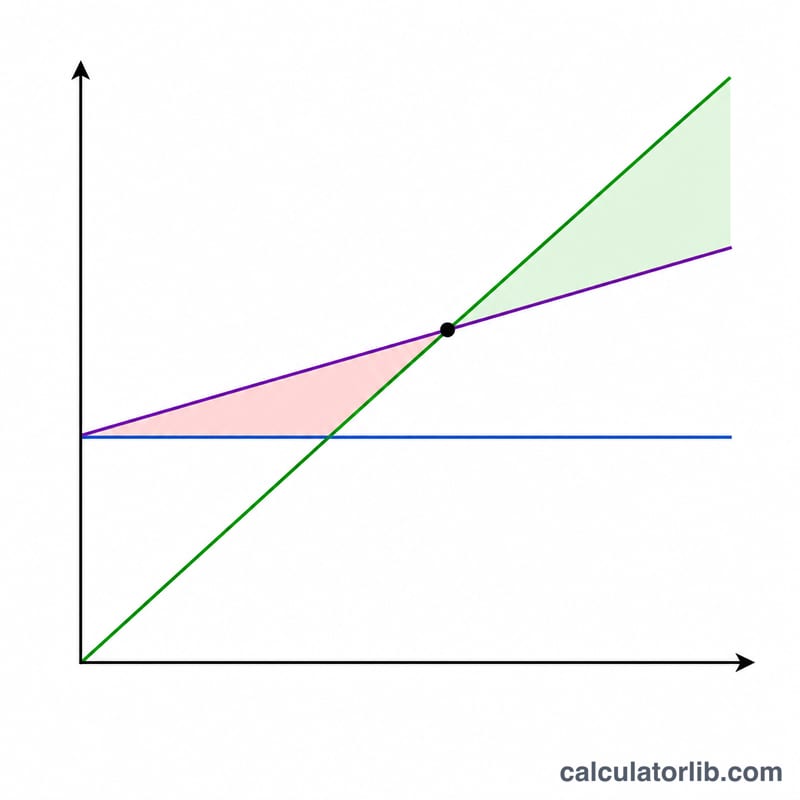

Interpreting Your Break-Even Revenue

Your break-even revenue is the level of sales at which total contribution margin exactly covers all fixed costs, producing a profit of zero. Selling one dollar below it produces a loss; selling above it produces profit at the rate of your CM ratio. For example, a business with a 40% CM ratio earns roughly $0.40 of operating profit on every additional sales dollar above break-even.

The CM ratio is the single biggest lever on this figure. Because break-even revenue equals fixed costs divided by the CM ratio, a higher CM ratio lowers the break-even revenue. Raising prices, cutting variable cost per unit, or shifting toward higher-margin products all increase the CM ratio and reduce the sales needed to break even.

Once you know your break-even point, the margin of safety measures how much cushion you have:

$$\text{Margin of Safety} = \text{Actual Sales} - \text{Break-Even Sales}$$It is often expressed as a percentage of actual sales. A larger margin of safety means revenue can fall further before the business slips into a loss. For instance, if actual sales are $160{,}000 and break-even is $125{,}000, the margin of safety is $35{,}000, or about 22% of sales.

Remember that these results rely on assumptions holding steady: that fixed costs stay fixed over the relevant range, that the contribution margin ratio remains constant, and that the sales mix does not change. If you add staff, sign a bigger lease, offer discounts, or face rising input costs, recompute your break-even point with the updated figures.

Key Terms Defined

- Fixed Costs

- Costs that do not change with the volume of units sold within a relevant range — for example rent, salaried staff, insurance, and equipment depreciation. They must be covered regardless of how much you sell.

- Variable Costs

- Costs that rise and fall directly with units produced or sold, such as raw materials, packaging, payment-processing fees, and per-unit shipping. They are usually stated as a cost per unit.

- Selling Price per Unit

- The amount of revenue received for each unit sold before any costs are deducted.

- Contribution Margin

- The selling price per unit minus the variable cost per unit. It is the portion of each sale that “contributes” first to covering fixed costs and then to profit: \(\text{CM} = \text{Price} - \text{Variable Cost}\).

- Contribution Margin Ratio (CM Ratio)

- The contribution margin expressed as a fraction of the selling price: \(\text{CM Ratio} = (\text{Price} - \text{Variable Cost}) / \text{Price}\). It tells you how many cents of each sales dollar are available to cover fixed costs and profit.

- Break-Even Point

- The sales level — in revenue dollars or in units — at which total revenue equals total costs, so profit is exactly zero. In dollars it equals fixed costs divided by the CM ratio.

FAQ

What is the difference between break-even units and break-even revenue? Units divide fixed costs by the per-unit contribution margin; revenue divides fixed costs by the contribution margin ratio. Multiply break-even units by price to get break-even revenue.

What if my price equals my variable cost? The contribution margin is zero, so you can never break even no matter how much you sell — every sale just covers its own variable cost.

Should taxes be included? The standard break-even model ignores income tax because profit at break-even is zero, so tax on zero profit is zero.