What is a CD?

A certificate of deposit (CD) is a savings product offered by banks and credit unions that pays a fixed interest rate over a fixed term (usually 3 months to 10 years). In exchange for locking up your money, you typically earn a higher rate than a standard savings account. Withdraw early and most CDs charge an early-withdrawal penalty equal to several months of interest.

The Compound Interest Formula

$$FV = P \cdot \left(1 + \frac{r/100}{n}\right)^{n \cdot t}$$

- \(P\) = principal (initial deposit)

- \(r\) = annual interest rate (as a decimal)

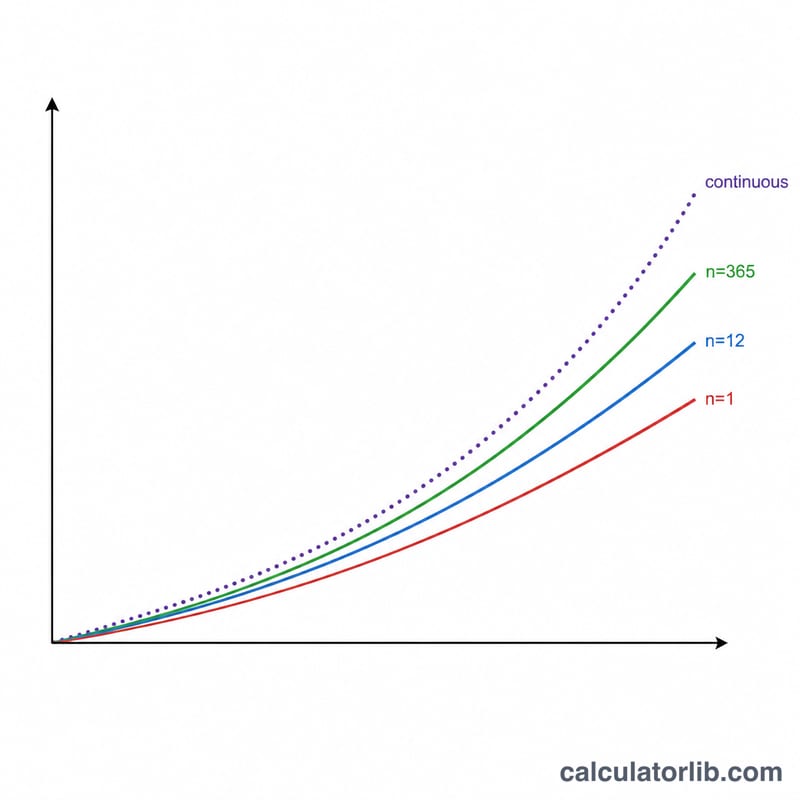

- \(n\) = compounding periods per year (1 annual, 4 quarterly, 12 monthly, 365 daily)

- \(t\) = time in years (including any extra months)

For continuous compounding (the theoretical maximum), use \(FV = P \cdot e^{r \cdot t}\).

Worked Example

$10,000 deposit, 5% annual rate, 3-year term, compounded monthly:

- \(n = 12\), \(r = 0.05\), \(t = 3\)

- $$FV = 10{,}000 \times (1 + 0.05/12)^{36} = 10{,}000 \times 1.16147 = \mathbf{\$11{,}614.72}$$

- Total interest earned = $1,614.72

- Effective annual yield (APY) = \(\left(1 + 0.05/12\right)^{12} - 1 = 5.116\%\) (versus the stated 5% APR)

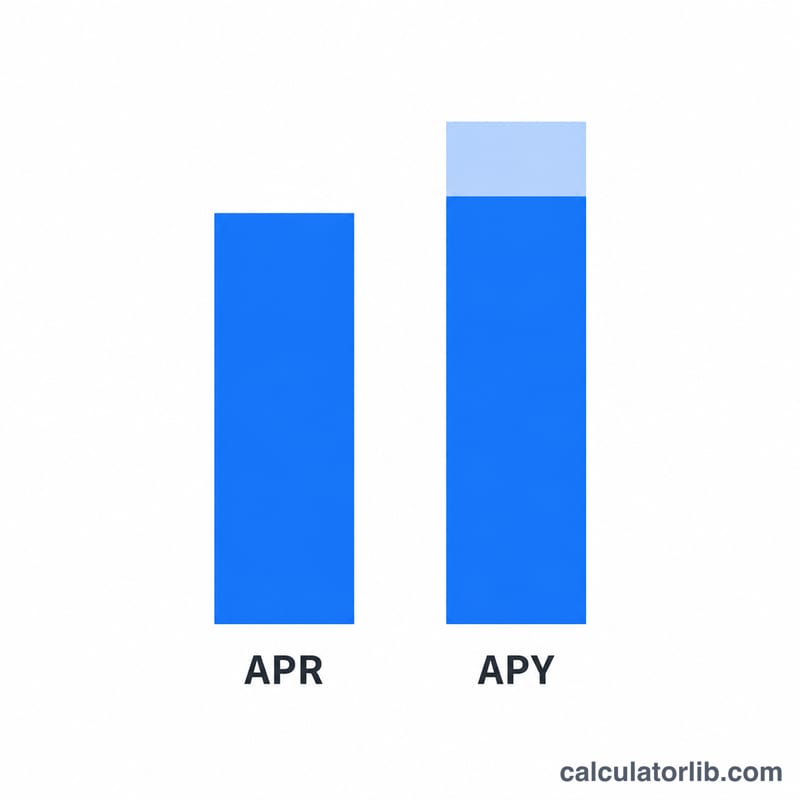

APR vs APY

The APR (annual percentage rate) is the nominal annual rate, ignoring compounding. The APY (annual percentage yield) is the actual return after compounding within one year. Banks must disclose APY for deposit accounts in the U.S. (Truth in Savings Act). When comparing CDs, always look at APY — a 5% APR compounded daily earns more than a 5% APR compounded annually.

Tax Considerations

CD interest is taxed as ordinary income at your marginal federal rate (and state, if applicable). For a CD in a regular taxable account, the after-tax interest is what you actually keep. Set the tax rate field to your marginal tax rate (e.g., 22%, 24%, 32%) for an after-tax projection. CDs in tax-deferred accounts (IRA, 401k) defer the tax until withdrawal.

CD Strategies

- CD ladder: spread your money across CDs with staggered maturities (e.g., 1, 2, 3, 4, 5 years). When the 1-year matures, reinvest into a new 5-year CD. Eventually you have a 5-year CD maturing every year — high rates with annual liquidity.

- Bump-up CD: lets you bump your rate higher once during the term if rates rise. Usually starts with a slightly lower rate than a standard CD.

- No-penalty CD: can be withdrawn anytime without penalty. Lower rate but useful when interest rates may fall.

- Brokered CDs: sold through brokerages (Fidelity, Schwab) — wider rate selection, but they trade in the secondary market with rate-driven price changes.

Caveats

- Early-withdrawal penalty. Typical: 3 months interest for ≤1y term, 6 months for 1–5y, 12 months for 5y+. Check the deposit agreement.

- Inflation risk. A 5% CD earning 5% with 3% inflation has only ~2% real return.

- FDIC/NCUA insurance. Each depositor insured up to $250,000 per bank per ownership category. Spread larger deposits across institutions.