What is the Payback Period?

The payback period is the time required for the cumulative cashflows of an investment to equal its initial cost. It answers a simple question: "How long until I get my money back?" It's one of the easiest investment metrics to understand, which is why it's commonly quoted alongside ROI and IRR.

Simple vs Discounted Payback

- Simple Payback Period just adds the nominal cashflows year by year. It ignores the time value of money — a dollar in year 5 counts the same as a dollar in year 1.

- Discounted Payback Period first discounts each cashflow back to present value at a chosen discount rate, then sums them. It's longer than simple payback (because future dollars are worth less), and it's a more honest measure for capital budgeting.

If the discount rate is 0, the two are equal. Set the discount rate to your cost of capital (e.g., 8–12% for a typical mid-market firm) for the discounted version.

The Formula

For constant or growing cashflows where \(CF_t = CF_1 \cdot (1 + g)^{t-1}\):

Simple: find smallest N where $$N \text{ where } \sum_{t=1}^{N} CF_t \geq I_0$$

Discounted: find smallest N where $$N \text{ where } \sum_{t=1}^{N} \frac{CF_t}{(1+r)^t} \geq I_0$$

The fractional year is interpolated linearly within the final year — the calculator returns 3.16 years if payback occurs 16% of the way through year 4.

Worked Example

$100,000 investment, $30,000 first-year cashflow growing 5%/year, no discount rate:

| Year | Cashflow | Cumulative |

|---|---|---|

| 1 | $30,000 | $30,000 |

| 2 | $31,500 | $61,500 |

| 3 | $33,075 | $94,575 |

| 4 | $34,729 | $129,304 |

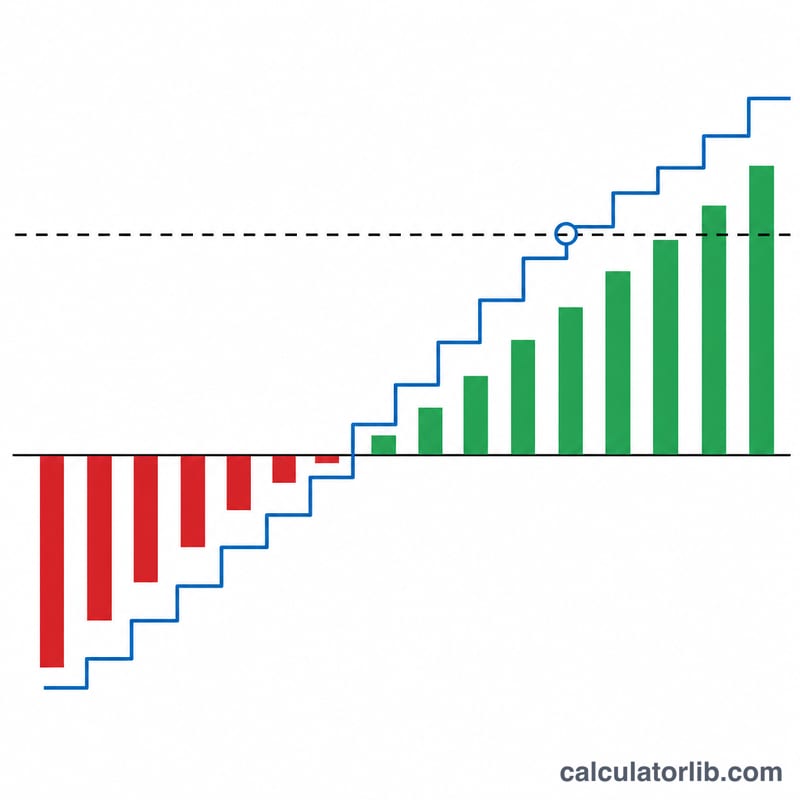

Payback occurs in year 4. The fraction = $$(\$100{,}000 - \$94{,}575) / \$34{,}729 = 0.156$$ so the simple payback period is 3.16 years.

With a 10% discount rate, each cashflow is reduced (year 4's $34,729 becomes $23,719 in PV), pushing the discounted payback to about 3.92 years.

When Payback Period is Useful

- Risk screening: shorter payback = lower risk. A 2-year payback project is safer than a 7-year one even if both have the same NPV.

- Liquidity-constrained firms: when you need cashback fast to fund the next investment.

- High-uncertainty environments: in volatile industries, projecting cashflows beyond payback is unreliable, so payback is a sensible focal metric.

Limitations

- Ignores cashflows after payback. Two projects with 3-year payback are treated equal even if one continues paying for 10 more years and the other stops.

- Simple version ignores discounting. Use discounted payback when comparing projects with different time profiles.

- Doesn't measure profitability. Payback tells you "when," not "how much." Always pair with NPV or IRR for capital allocation decisions.