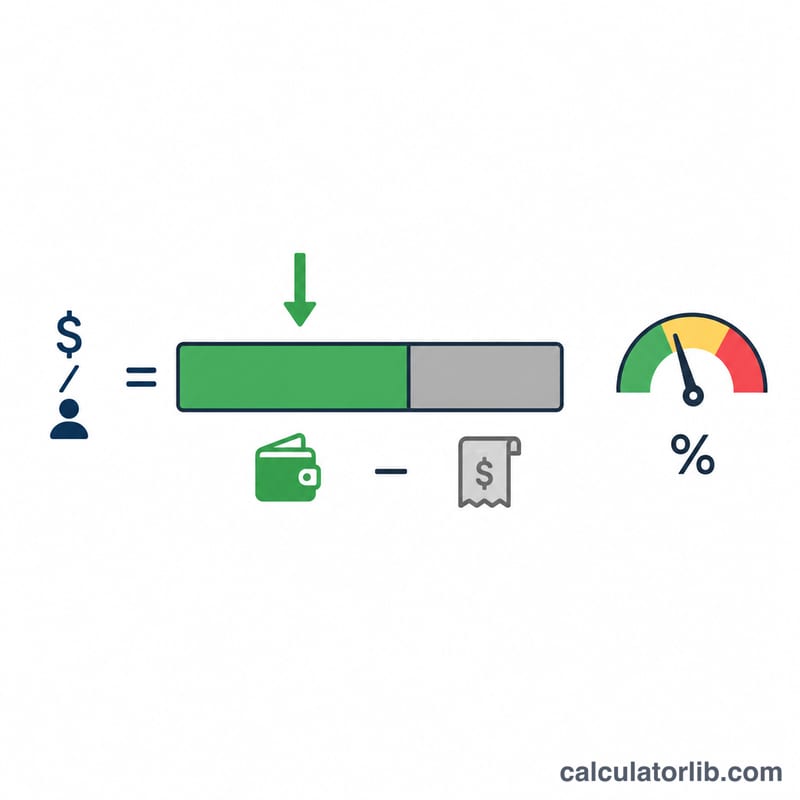

What is the ACB Loan Affordability Calculator?

This calculator estimates the largest monthly loan payment (EMI) you can comfortably take on, based on your gross monthly income, the maximum debt-to-income (DTI) ratio a lender allows, and the debt payments you already make. It gives you a quick reality check before applying for a personal loan, car loan or mortgage. The DTI approach is used by lenders worldwide, so the tool is currency-agnostic — just enter all figures in the same currency.

How to use it

Enter your gross monthly income, the maximum DTI ratio the lender uses (commonly 36%–43%, sometimes up to 50%), and your existing monthly debt payments such as credit cards, car loans and other EMIs. The calculator shows the maximum EMI room left for a new loan, your total allowable debt budget, and how much of that budget your current debts already consume.

The formula explained

First the lender's debt ceiling is calculated as \(\text{Income} \times \text{DTI}\). This is the most you should spend on all debt combined. Subtracting your existing debt payments leaves the room available for a new loan: $$\text{Max EMI} = (\text{Income} \times \text{DTI}) - \text{Existing Debts}$$ If existing debts already exceed the ceiling, the result is zero — meaning no additional borrowing is advisable.

Worked example

Suppose you earn 5,000 a month, the lender's maximum DTI is 40%, and you already pay 500 in existing debts. Your total debt ceiling is \(5{,}000 \times 0.40 = 2{,}000\). Subtract existing debts: \(2{,}000 - 500 = 1{,}500\). So you can afford an EMI of up to 1,500 per month on a new loan, and your existing debts use 25% of the allowed budget.

Standard DTI Thresholds by Loan Type

Lenders rarely allow your total debt payments to exceed a set share of gross monthly income. The maximum debt-to-income (DTI) ratio you plug into this calculator should reflect the program you are targeting. The table below lists widely used guideline thresholds.

| Loan type / program | Front-end DTI (housing only) | Back-end DTI (all debts) |

|---|---|---|

| Conventional mortgage (traditional guideline) | ~28% | ~36% |

| Conventional (with strong credit/reserves) | — | up to ~45% |

| Qualified Mortgage (QM) rule | — | 43% |

| FHA loan | ~31% | ~43%, up to ~50% with compensating factors |

| VA loan | — | ~41% (residual income test also applies) |

| Personal / auto loan (typical) | — | ~36%–43% |

Front-end DTI counts only housing-related costs (mortgage principal and interest, property tax, homeowner's insurance, and any HOA dues) as a percentage of gross monthly income. Back-end DTI adds all other recurring debt obligations — car loans, student loans, credit-card minimums, personal loans and alimony/child support — to housing costs. Because the back-end ratio captures every obligation, it is the figure most lenders underwrite to, and it is the value most appropriate for the DTI field in an affordability check.

These are general guideline figures; individual lenders and automated underwriting systems set their own overlays, so confirm the cap that applies to your situation.

Affordable EMI Across Income & DTI Scenarios

The maximum affordable EMI is the total debt budget allowed by your DTI cap minus the debt payments you already carry: \[\text{Max EMI} = \text{Income} \times \frac{\text{DTI \%}}{100} - \text{Existing Debts}.\] The "Total debt budget" column shows the full allowable monthly debt load, and the "Max EMI room" column shows what remains for a new loan after subtracting existing payments.

| Monthly income | DTI % | Existing debts | Total debt budget | Max EMI room |

|---|---|---|---|---|

| $3,000 | 36% | $300 | $1,080 | $780 |

| $5,000 | 40% | $500 | $2,000 | $1,500 |

| $8,000 | 43% | $1,200 | $3,440 | $2,240 |

| $10,000 | 50% | $2,000 | $5,000 | $3,000 |

Notice how existing obligations directly erode the available EMI room: at $5,000 income and a 40% cap the total allowable debt is $2,000, but $500 of pre-existing payments leaves only $1,500 for a new loan. Once you know an affordable EMI, you can work backward to a loan amount using an EMI/payment calculator with a chosen interest rate and term.

Interpreting Your Affordable EMI

The number this calculator returns is a ceiling, not a target. It marks the largest monthly payment that keeps your total debt within the chosen DTI limit — borrowing exactly to that ceiling leaves no buffer for rate changes, emergencies or rising living costs.

- Lenders look beyond DTI. Approval and pricing also depend on credit score, employment history, down payment, the loan term, and the offered interest rate. A strong profile may earn an exception above guideline DTI; a weak one may be capped below it.

- A result of zero (or negative) means your existing debt payments already consume the entire allowable budget at that DTI percentage. In that case there is no room for additional EMI until you either reduce existing debt, increase income, or qualify under a higher DTI threshold.

- EMI affordability is not the same as loan amount. A given affordable EMI translates into very different principal sums depending on the interest rate and tenure: a longer term or lower rate supports a larger loan for the same payment. Use a payment/loan calculator to convert your affordable EMI into a borrowable principal.

- Gross vs. net. Standard DTI math uses gross (pre-tax) monthly income, so the EMI ceiling it produces can be a larger share of your take-home pay than the percentage suggests.

This is general information, not personalized financial advice. Treat the figure as one input among several when assessing what you can comfortably repay.

Key Terms Explained

- EMI (Equated Monthly Installment)

- The fixed amount paid each month toward a loan, covering both principal and interest, until the balance is repaid over the loan term.

- Debt-to-Income Ratio (DTI)

- The percentage of gross monthly income that goes to debt payments. Lenders use it to gauge repayment capacity; lower ratios indicate more borrowing room.

- Gross income

- Total monthly earnings before taxes, retirement contributions and other deductions. DTI calculations conventionally use gross income.

- Net income

- Take-home pay after taxes and deductions. It reflects actual cash available but is not the standard basis for DTI underwriting.

- Existing debt payments

- Recurring monthly obligations already in place — credit-card minimums, auto, student or personal loans, and court-ordered support — that are subtracted from the allowable budget to find remaining EMI room.

- Front-end DTI

- The share of income devoted to housing costs only (principal, interest, taxes, insurance, HOA dues).

- Back-end DTI

- The share of income devoted to all recurring debts, housing plus every other obligation. This is the broader ratio most lenders underwrite to.

- Debt ceiling

- The maximum total monthly debt allowed under your DTI cap, calculated as income multiplied by the DTI percentage. Subtracting existing debts from this ceiling yields the affordable EMI.

FAQ

What DTI should I use? Many lenders cap total DTI at 36%–43%. Use the figure your lender provides; if unsure, 40% is a reasonable planning default.

Should I use gross or net income? Lenders typically calculate DTI on gross (pre-tax) income, so this tool assumes gross income.

Why is my result zero? If your existing debt payments already meet or exceed the income × DTI ceiling, there is no room for additional borrowing under that ratio.