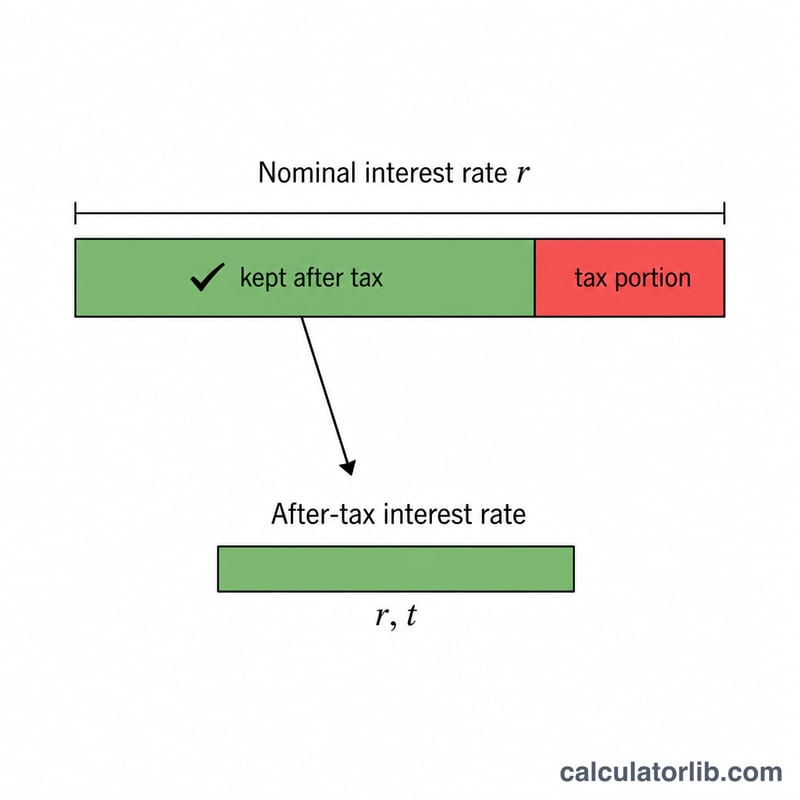

What Is After-Tax Yield?

The after-tax yield is the effective return you actually keep on a deposit, savings account, bond, or certificate of deposit once income tax on the interest is taken out. A headline (nominal) rate of 5% sounds attractive, but if a quarter of your interest goes to tax, your real earning rate is lower. This calculator converts a nominal rate into the yield you truly receive.

How to Use It

Enter the nominal interest rate advertised on the account, then enter your marginal tax rate that applies to interest income. The calculator instantly shows your after-tax yield, your original nominal rate for comparison, and how much yield is lost to tax. This lets you compare taxable and tax-free products on an apples-to-apples basis.

The Formula Explained

The math is simple: after-tax yield = nominal rate × (1 − tax rate):

$$\text{After-Tax Yield} = r \times \left(1 - \frac{t}{100}\right)$$The tax rate is expressed as a decimal, so a 25% tax rate becomes \(0.25\), leaving you 75% (\(0.75\)) of the interest. Multiplying the nominal rate by that fraction gives the rate you keep.

Worked Example

Suppose a savings account pays a nominal 5% and your tax rate on interest is 25%. After-tax yield:

$$5 \times (1 - 0.25) = 5 \times 0.75 = \mathbf{3.75\%}$$So although the bank advertises 5%, your effective return is 3.75%, with 1.25 percentage points lost to tax.

Interpreting Your After-Tax Yield

The after-tax yield is the percentage return you actually keep after income tax is applied to the interest earned on a deposit. Because the taxman takes a share of the nominal interest, the after-tax yield is always lower than the stated rate (unless your tax rate is zero). It is calculated as:

$$\text{After-Tax Yield} = \text{Nominal Rate} \times \left(1 - \frac{\text{Tax Rate}}{100}\right)$$

For example, a deposit paying a 5% nominal rate held by someone in a 22% marginal tax bracket produces an after-tax yield of \(5 \times (1 - 0.22) = \) 3.9%.

Why it matters for comparisons. The after-tax yield is the directly comparable figure when you weigh a taxable product (such as a standard savings account or CD) against a tax-free product (such as certain municipal bonds or a tax-advantaged account). A taxable account quoting a higher nominal rate may actually deliver less to your pocket than a tax-free account quoting a lower rate. Reducing every option to its after-tax yield puts them on the same footing.

Taxable-equivalent yield (the reverse comparison). When you already know the rate on a tax-free product and want to know what a taxable product would have to pay to match it, use the taxable-equivalent yield:

$$\text{Taxable-Equivalent Yield} = \frac{\text{Tax-Free Rate}}{1 - \dfrac{\text{Tax Rate}}{100}}$$

For instance, a 4% tax-free rate for someone in a 22% bracket is equivalent to a taxable rate of \(4 \div (1 - 0.22) \approx 5.13\%\) — a taxable account must beat 5.13% to come out ahead. This is simply the inverse of the after-tax calculation.

What this figure does not capture. The basic after-tax yield assumes simple interest applied to the nominal rate and ignores the effect of compounding (which the annual percentage yield, or APY, reflects). It also ignores inflation, which erodes real purchasing power, and any account fees, minimum-balance requirements, or differences in how and when interest is taxed. Treat it as a clean apples-to-apples interest comparison, not a complete forecast of real returns.

Key Terms Explained

- Nominal interest rate

- The stated annual interest rate on a deposit before any taxes, fees, or compounding adjustments are applied. It is the headline rate a bank advertises.

- Marginal tax rate

- The tax rate applied to your next (highest) dollar of income. Because interest is typically taxed as ordinary income, your marginal rate — not your average rate — is the correct figure to use when computing after-tax yield.

- After-tax yield

- The effective return retained after income tax on the interest. Calculated as the nominal rate multiplied by \((1 - \text{tax rate})\); it is the figure used to compare taxable products on an even basis.

- Taxable-equivalent yield

- The pre-tax rate a taxable product would need to match a given tax-free rate, found by dividing the tax-free rate by \((1 - \text{tax rate})\). It lets you compare a tax-free yield against taxable alternatives.

- APY (Annual Percentage Yield)

- The effective annual rate of return that accounts for the effect of compounding interest within the year. Two accounts with the same nominal rate but different compounding frequencies will have different APYs.

- Tax-exempt / tax-free yield

- The yield on an investment whose interest is exempt from some or all income tax (for example, certain municipal bonds). Because no tax is deducted, its after-tax yield equals its nominal yield, which can make a lower stated rate competitive with a higher taxable rate.

FAQ

Does this account for compounding? No — it converts a simple nominal rate to its after-tax equivalent. Compare it against the comparable nominal/APY basis of other products.

Which tax rate should I enter? Use your marginal rate on interest income, since interest is usually taxed at your ordinary income rate.

How do I compare to a tax-free bond? A tax-free yield can be compared directly to this after-tax yield — whichever is higher is the better net return.