What Is the Real Rate of Return?

The real rate of return is the growth of your money after accounting for inflation. A bank account paying 5% sounds great, but if prices are rising 3% per year, your actual gain in purchasing power is much smaller. This calculator uses the Fisher equation to convert a nominal interest rate into a real, inflation-adjusted rate so you can see how much your money is truly growing.

How to Use It

Enter the nominal interest rate (the headline rate quoted by your bank, bond, or investment) as a percentage, then enter the expected or actual annual inflation rate. The calculator returns the exact real rate using the Fisher equation, along with the common approximation (nominal minus inflation) for comparison.

The Formula Explained

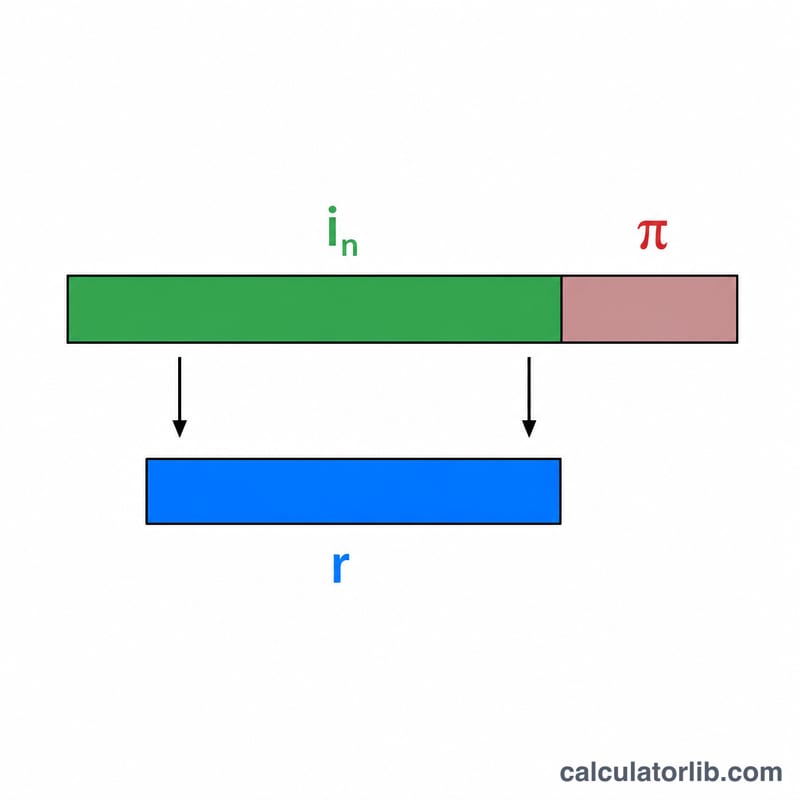

The exact relationship is:

$$\text{real rate} = \frac{1 + \text{nominal rate}}{1 + \text{inflation rate}} - 1$$

Because both rates compound, you cannot simply subtract one from the other for a precise answer. The popular shortcut real ≈ nominal − inflation works well only when both numbers are small; at higher rates it overstates your real return.

Worked Example

Suppose your savings earn a nominal 5% while inflation runs at 3%. The exact real rate is $$\left(\frac{1 + 0.05}{1 + 0.03}\right) - 1 = \frac{1.05}{1.03} - 1 = 0.019417,$$ or about 1.94%. The quick approximation would give \(5\% - 3\% = 2\%\), which slightly overstates the true 1.94%.

Real Return Across Common Scenarios

The exact real rate uses the Fisher equation, \(\left(\frac{1+i}{1+\pi}-1\right)\times100\), where \(i\) is the nominal rate and \(\pi\) is inflation. The common approximation simply subtracts: \(\text{real}\approx i-\pi\). The two agree closely at low rates but diverge as rates climb, and the exact figure is always slightly below the approximation.

| Nominal Rate | Inflation Rate | Exact Real Rate (Fisher) | Approximation (\(i-\pi\)) | Notes |

|---|---|---|---|---|

| 2% | 3% | -0.97% | -1.00% | Negative — purchasing power erodes |

| 5% | 3% | 1.94% | 2.00% | Modest real gain |

| 8% | 6% | 1.89% | 2.00% | Gap widens at higher inflation |

| 10% | 2% | 7.84% | 8.00% | Strong real growth |

| 3% | 3% | 0.00% | 0.00% | Break-even — purchasing power held flat |

| 4% | 8% | -3.70% | -4.00% | Sharply negative in high-inflation periods |

Notice that whenever the nominal rate equals inflation the real rate is exactly zero, and whenever inflation exceeds the nominal rate the real rate turns negative regardless of the positive headline yield.

Interpreting Your Real Rate of Return

The real rate of return tells you how much your purchasing power actually changed once inflation is stripped out of a nominal interest rate or investment return. The Fisher equation makes this precise:

$$\text{Real Rate} = \left(\frac{1 + \frac{i}{100}}{1 + \frac{\pi}{100}} - 1\right)\times 100$$- Positive real rate: your nominal return outpaced inflation, so the money you hold buys more goods and services than before. Each percentage point of real return represents genuine growth in purchasing power.

- Zero real rate (break-even): your nominal return exactly matched inflation. The dollar amount grew, but it buys the same basket of goods it did at the start — you stood still in real terms.

- Negative real rate: inflation outran your nominal return. Even though the account balance may have risen, it commands fewer real goods than before, so purchasing power eroded.

Because the equation divides growth factors rather than subtracting rates, the exact real rate is always slightly lower than the quick \(i-\pi\) shortcut, and the difference grows as both rates rise. The break-even nominal rate is simply the rate that makes the numerator equal the denominator — that is, a nominal rate equal to the inflation rate, which produces a real rate of exactly zero.

This is general educational information, not professional financial advice. Real returns ignore taxes, fees, and timing of cash flows, all of which affect actual outcomes; consult a qualified professional for decisions specific to your situation.

FAQ

Can the real rate be negative? Yes. If inflation is higher than your nominal rate, your purchasing power shrinks and the real rate is negative.

Why is the exact answer lower than nominal minus inflation? The denominator \((1 + \text{inflation})\) divides the entire nominal growth, so the compounding interaction reduces the result compared with simple subtraction.

Which inflation rate should I use? Use a recent or expected annual inflation figure such as the Consumer Price Index (CPI) for your region.