What Is the Required Monthly Deposit Calculator?

This calculator tells you exactly how much you need to set aside each month to hit a future savings target. By accounting for compound interest, it shows that you often need to contribute less than the goal divided by the number of months — because your money earns returns along the way. It works for any currency and is useful for building an emergency fund, saving for a home deposit, a vacation, or a child's education.

How to Use It

Enter three values: your savings goal (the future amount you want), the expected annual interest rate as a percentage, and the number of years you plan to save. The calculator converts the rate to a monthly rate and the timeline to months, then solves for the level monthly deposit that grows to your goal.

The Formula Explained

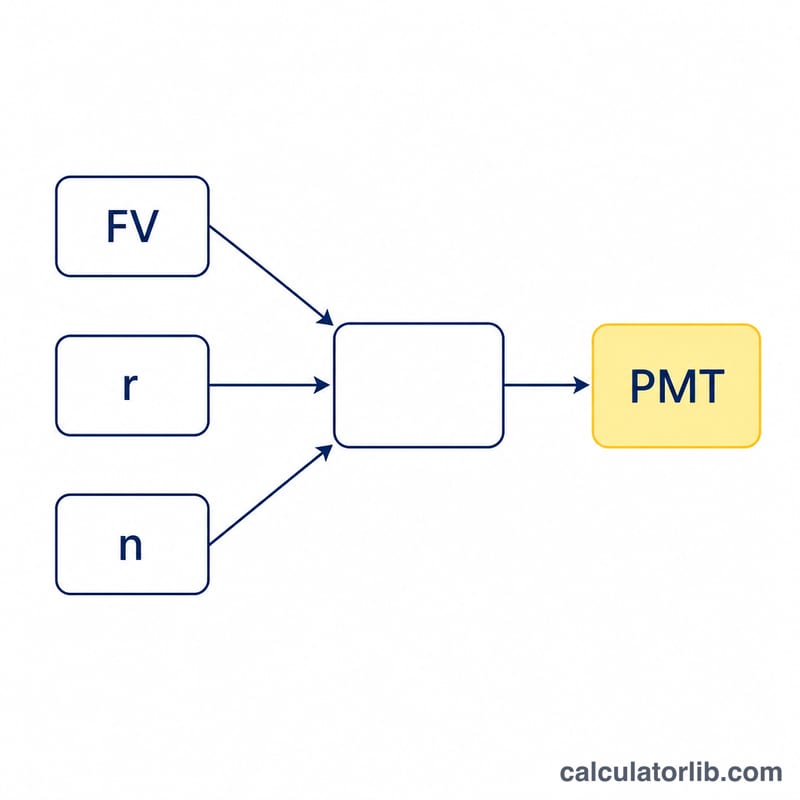

The future value of a series of equal end-of-month deposits is an ordinary annuity. Rearranging the annuity formula to solve for the payment gives:

$$\text{PMT} = \frac{\text{FV} \times r}{(1 + r)^{n} - 1}$$

where FV is the goal, r is the monthly rate (annual rate \(\div 12\)), and n is the number of monthly deposits (years \(\times 12\)). If the interest rate is zero, the deposit is simply \(\text{FV} \div n\).

Worked Example

Suppose you want $100,000 in 20 years at 5% annual interest. The monthly rate is \(0.05 \div 12 \approx 0.0041667\) and \(n = 240\) months. Then \((1.0041667)^{240} \approx 2.7126\), so the denominator is \(1.7126\). $$\text{PMT} = \frac{100{,}000 \times 0.0041667}{1.7126} \approx \$243.29 \text{ per month}$$ Over 240 months you deposit about $58,389, and interest supplies the rest.

FAQ

Are deposits made at the start or end of the month? This tool uses end-of-month (ordinary annuity) deposits, the most common assumption.

Is interest compounded monthly? Yes — the annual rate is divided by 12 and compounded each month.

What if my rate is 0%? The calculator falls back to simply dividing your goal by the number of months.