What This Calculator Does

This tool answers a common money question: "How much do I need to put away each month to reach my goal?" Given a future value target, a starting balance already saved, an annual interest rate, and a time horizon in years, it returns the fixed monthly deposit required. Deposits and the starting balance are both assumed to earn compound interest monthly.

How to Use It

Enter your future value goal (the amount you want to have), your current starting balance, the annual interest rate you expect, and the number of years until your target date. The calculator returns the monthly deposit, the total you personally contribute, how much your starting balance grows to on its own, and the interest earned along the way.

The Formula Explained

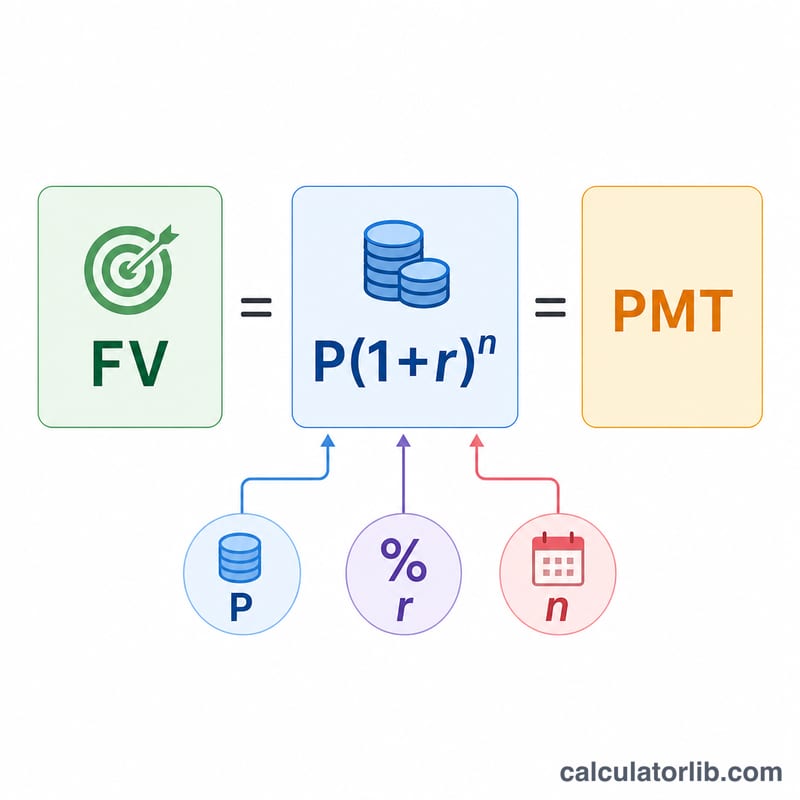

The required payment is derived from the future value of an annuity plus the future value of the lump-sum starting balance:

$$PMT = \dfrac{(FV - P(1+r)^n)\,r}{(1+r)^n - 1}$$

Here FV is your goal, P is the starting balance, \(r\) is the monthly rate (annual rate ÷ 12), and \(n\) is the number of months (years × 12). The term \(P(1+r)^n\) is what your starting balance grows to by itself; the rest of the gap must be filled by monthly deposits.

Worked Example

Suppose you want $50,000 in 10 years, already have $5,000 saved, and expect 6% annually. Then \(r = 0.005\), \(n = 120\), and \((1+r)^n \approx 1.81940\). Your $5,000 grows to about $9,097. The remaining $40,903 must come from deposits: $$PMT \approx \frac{40{,}903 \times 0.005}{0.81940} \approx \$249.59 \text{ per month}.$$

FAQ

What if the interest rate is 0%? With no interest, the calculator simply divides the gap (goal minus starting balance) evenly across all months.

Are deposits made at the start or end of the month? This model assumes end-of-month (ordinary annuity) deposits, the most common convention.

Does it account for taxes or inflation? No — results are nominal. For real purchasing power, use an inflation-adjusted rate of return.