What Is a Blended Interest Rate?

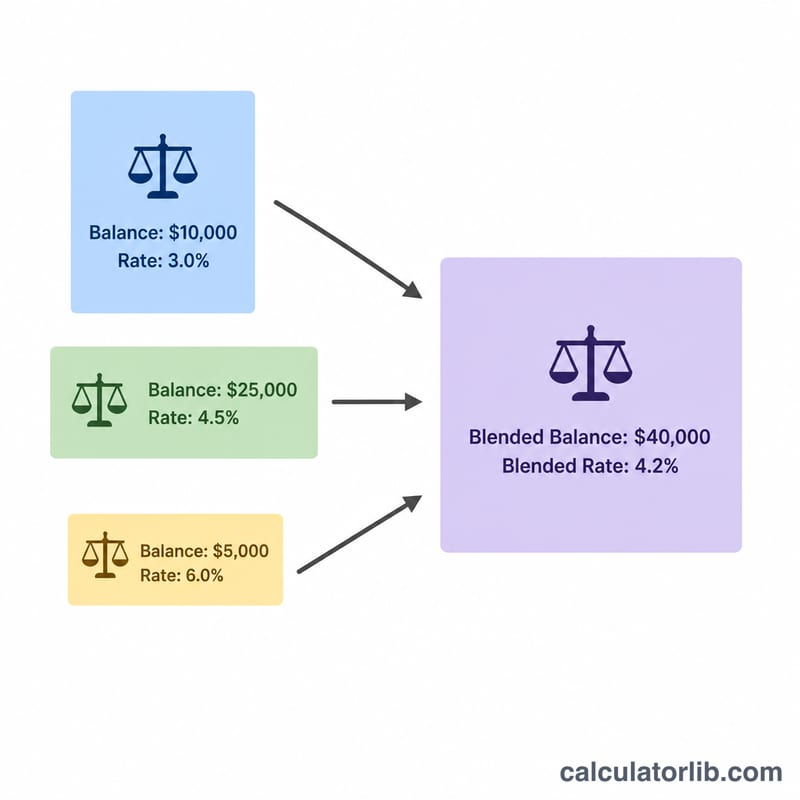

A blended interest rate — also called a weighted average rate — is the single effective rate you earn (or pay) across several balances that carry different rates. Instead of a simple average, it weights each rate by how much money sits in that account, so a large balance has more influence than a small one. This tool works for savings accounts, CDs, multiple loans, or any mix of balances and rates.

How to Use It

Enter the balance and its annual interest rate for each account (up to four). Leave unused rows blank or at zero. The calculator instantly returns your blended rate, the total of all balances, and an estimate of the annual interest those balances would earn at the blended rate.

The Formula Explained

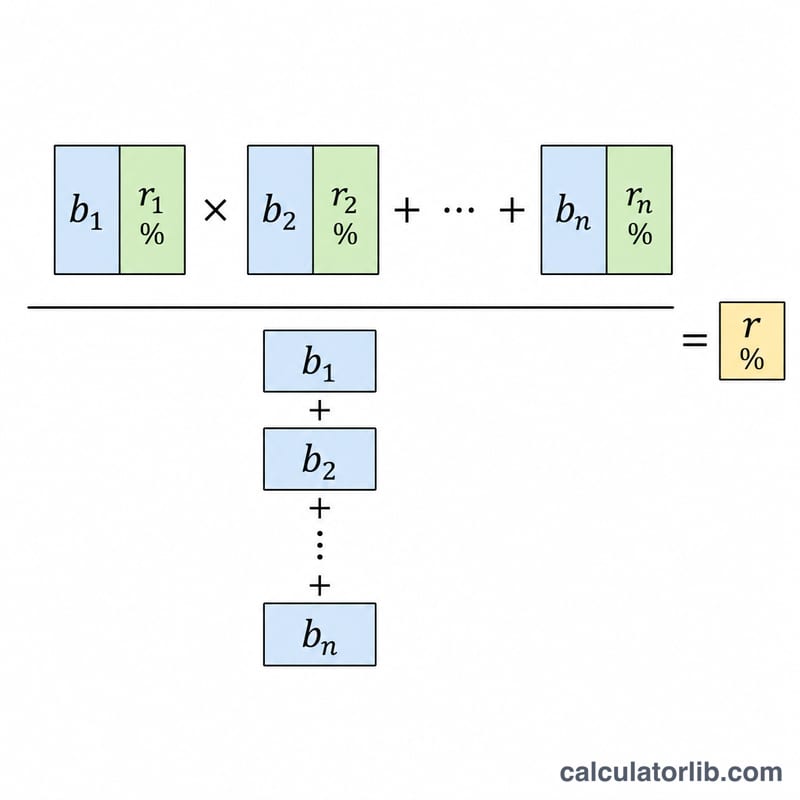

The blended rate is the sum of each balance multiplied by its rate, divided by the total of all balances:

$$\text{Blended} = \dfrac{\sum (\text{Balance}_i \times \text{Rate}_i)}{\sum \text{Balance}_i}$$Because each rate is weighted by its balance, the result always lands between the lowest and highest individual rate.

Worked Example

Suppose you have $10,000 earning 4% and $5,000 earning 2%. The weighted total is $$(10{,}000 \times 4) + (5{,}000 \times 2) = 40{,}000 + 10{,}000 = 50{,}000.$$ The total balance is \(15{,}000\). So the blended rate is $$50{,}000 \div 15{,}000 \approx 3.333\%.$$ Applied to $15,000, that yields about $500 of annual interest.

Interpreting Your Blended Rate

The blended rate is the single effective interest rate that, if applied to your entire combined balance, would produce the same total interest as your accounts earning their individual rates. It answers the question: “overall, what rate is my money actually earning?”

- It always lands between the lowest and highest individual rate. A weighted average can never exceed the best rate in the mix or fall below the worst. If every account earns the same rate, the blended rate equals that rate.

- It is pulled toward the rate on the largest balance. The bigger an account's share of the total, the more weight its rate carries. A small balance at a high rate moves the average only slightly, while most of your money sitting at a low rate keeps the blended rate low.

- It is a snapshot of current balances. The result reflects the balances you entered right now. As you deposit, withdraw, or transfer funds between accounts, the weights shift and the blended rate changes.

- It does not account for compounding frequency. The calculation uses the nominal rates as entered. Accounts that compound daily versus annually can yield different actual returns even at the same stated rate — compare those using an effective annual rate (APY) calculation if precision matters.

- It ignores fees, taxes, promotional expirations, and tiered rates. Monthly fees, interest-bearing tiers, or introductory rates that later reset are not captured here; they would lower or change your true net return.

Use the blended rate to gauge how efficiently your overall savings are working and to see the impact of moving money toward higher-yield accounts. This is general educational information, not personal financial advice — consult a qualified professional for decisions about your specific situation.

FAQ

Is this just a simple average? No. A simple average would give 3% in the example above. The blended rate gives 3.333% because more money sits in the higher-rate account.

Can I use it for loans or credit cards? Yes. Enter loan balances and their APRs to find your blended borrowing rate.

Will the blended rate ever exceed my highest rate? No — a weighted average always falls between your minimum and maximum individual rates.