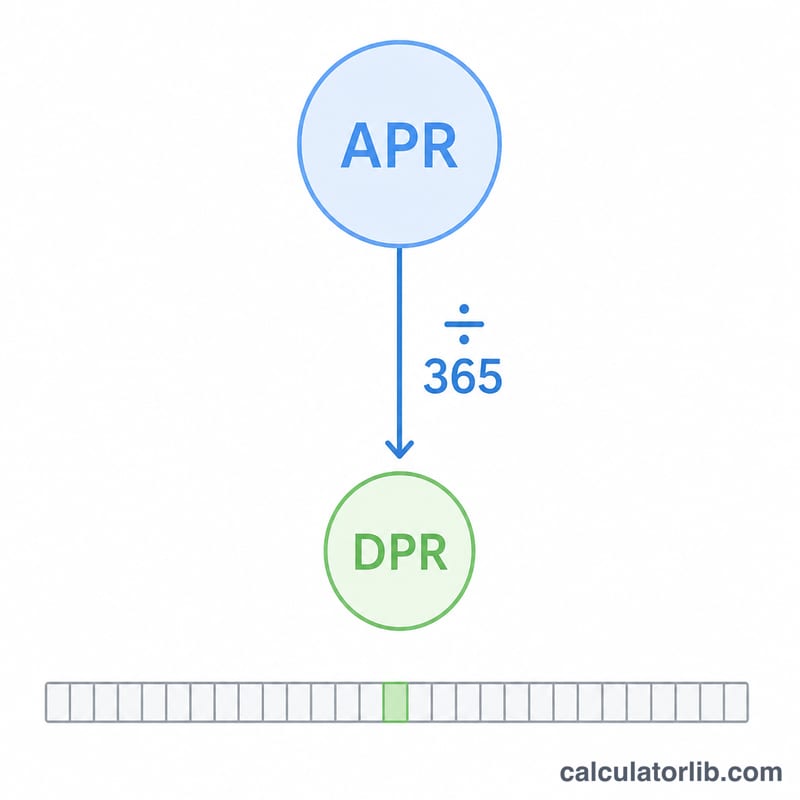

What Is the Daily Periodic Rate?

The daily periodic rate (DPR) is the interest rate a credit card issuer applies to your balance each day. Most card statements quote an annual percentage rate (APR), but interest is actually calculated daily. To find the DPR, simply divide the APR by the number of days in a year — typically 365. This calculator converts your APR into a DPR and estimates how much interest you would pay over one billing cycle.

How to Use This Calculator

Enter your card's APR as a percentage (for example, 19.99). Optionally, enter your average daily balance and the number of days in your billing cycle (usually 30 or 31). The tool returns your daily periodic rate, the effective rate over the whole cycle, and the dollar interest charged on the balance you provided.

The Formula Explained

The core formula is \(\text{DPR\%} = \dfrac{\text{APR}}{365}\). For a 19.99% APR, that works out to \(19.99 / 365 \approx 0.05477\%\) per day. Issuers then multiply this daily rate by your balance and by the number of days in the cycle to determine the finance charge. Some lenders use 360 days; this calculator uses the more common 365-day convention.

$$\text{Interest} = \text{Balance} \times \frac{\text{APR}}{365 \times 100} \times \text{Days}$$

Worked Example

Suppose your APR is 18%, your average daily balance is $1,000, and your billing cycle is 30 days. The DPR is \(18 / 365 = 0.049315\%\) per day. Over 30 days the effective rate is about \(1.4795\%\). The interest charged is

$$1{,}000 \times 0.00049315 \times 30 \approx \$14.79$$

FAQ

Why 365 and not 12 months? Credit card interest compounds daily, so issuers convert the annual rate to a daily figure rather than a simple monthly one.

Does my grace period matter? Yes — if you pay your statement balance in full each month, you typically pay no interest on new purchases regardless of the DPR.

Is this exact for my card? It's a close estimate. Your issuer's exact method, day-count basis, and compounding may differ slightly.