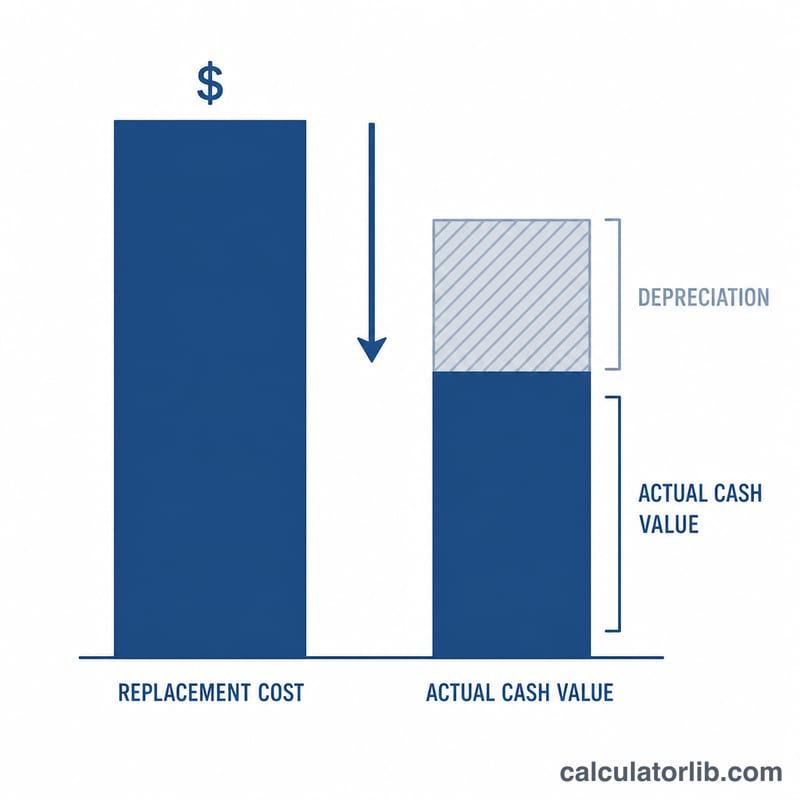

What Is Actual Cash Value?

Actual Cash Value (ACV) is the amount an item is worth today after accounting for depreciation — the wear, age, and obsolescence that reduce its value over time. Insurance companies frequently use ACV to settle claims, paying you the depreciated value of damaged or lost property rather than the full cost to buy a new replacement.

How to Use This Calculator

Enter the replacement cost (what it would cost to buy the same item brand new today) and the depreciation percentage that applies based on the item's age and condition. The calculator instantly returns the actual cash value and the dollar amount lost to depreciation.

The Formula Explained

The core equation is:

$$\text{ACV} = \text{Replacement Cost} \times \left(1 - \frac{\text{Depreciation}}{100}\right)$$If an item depreciates by 30%, it retains 70% of its replacement value, so you multiply the replacement cost by 0.70. The depreciation amount is simply the replacement cost minus the ACV.

Worked Example

Suppose a sofa would cost $1,000 to replace new, and it has depreciated 30% over its life. Then $$\text{ACV} = \$1{,}000 \times (1 - 0.30) = \$1{,}000 \times 0.70 = \$700.$$ The depreciation amount is \(\$1{,}000 - \$700 = \$300\). An ACV insurance policy would pay you $700 for that sofa.

ACV Across Different Depreciation Scenarios

ACV is found by reducing the replacement cost by the depreciation percentage: $$\text{ACV} = \text{Replacement Cost} \times \left(1 - \frac{\text{Depreciation \%}}{100}\right)$$ The first block fixes replacement cost at $2,000 and varies the depreciation percentage. The second block fixes depreciation at 50% and varies the replacement cost.

| Replacement Cost | Depreciation % | Depreciation Amount | ACV |

|---|---|---|---|

| $2,000 | 0% | $0 | $2,000 |

| $2,000 | 20% | $400 | $1,600 |

| $2,000 | 40% | $800 | $1,200 |

| $2,000 | 60% | $1,200 | $800 |

| $2,000 | 80% | $1,600 | $400 |

| $500 | 50% | $250 | $250 |

| $1,000 | 50% | $500 | $500 |

| $2,000 | 50% | $1,000 | $1,000 |

| $5,000 | 50% | $2,500 | $2,500 |

Notice ACV falls in direct proportion to the depreciation percentage when replacement cost is held constant, and rises proportionally with replacement cost when the percentage is held constant.

Interpreting Your ACV Result

The Actual Cash Value is the depreciated settlement figure that an ACV (rather than replacement-cost) policy is designed to pay for a covered loss. It represents what the item was worth at the time of loss after accounting for age, wear, and obsolescence — not what a brand-new equivalent costs today.

The difference between the replacement cost and the ACV is the recoverable depreciation gap: under a pure ACV policy this gap is generally an out-of-pocket cost you would bear to replace the item new. For a $2,000 item at 40% depreciation, the ACV is $1,200, leaving a $800 gap versus buying new. Under a replacement-cost (RCV) policy, that depreciation may be reimbursed after you actually replace the item and submit proof.

A few factual points to keep in mind when reading the number:

- Deductibles still apply. Your policy deductible is subtracted from the settlement, so the amount actually paid can be lower than the ACV shown here.

- Insurer schedules may differ. Adjusters use their own depreciation tables, condition assessments, and useful-life assumptions, so an official offer can differ from this straight-line estimate.

- Depreciation is bounded. Many insurers cap depreciation so an item retains some minimum value, and depreciation generally does not exceed the replacement cost (ACV does not go below $0).

- Replacement cost is the new-purchase basis. ACV is derived from the current cost to buy a comparable new item, then reduced — it is not the original purchase price.

This is general information about how the ACV formula works and is not insurance, legal, or financial advice; consult your policy documents and your insurer for how depreciation and settlement are determined in your specific claim.

FAQ

What's the difference between ACV and replacement cost value? ACV pays the depreciated value, while replacement cost value (RCV) pays the full cost to buy new without subtracting depreciation. RCV coverage usually costs more.

How do I estimate depreciation percentage? A common method is straight-line depreciation: divide the item's age by its expected useful life. A 3-year-old item with a 10-year life is roughly 30% depreciated.

Can ACV ever exceed replacement cost? No. Depreciation only reduces value, so ACV is always less than or equal to the replacement cost (equal only when depreciation is 0%).