What Is the Cash Conversion Cycle?

The Cash Conversion Cycle (CCC) measures how many days a company's cash is tied up in its operating process — from the moment it pays suppliers for inventory until it finally collects cash from customers. A lower (or even negative) CCC means cash returns to the business faster, improving liquidity and reducing the need for external financing.

How to Use This Calculator

Enter three figures, each expressed in days: Days Inventory Outstanding (DIO), Days Sales Outstanding (DSO), and Days Payable Outstanding (DPO). The calculator returns your CCC in days along with your operating cycle. Pull these inputs from your financial statements using standard turnover ratios.

The Formula Explained

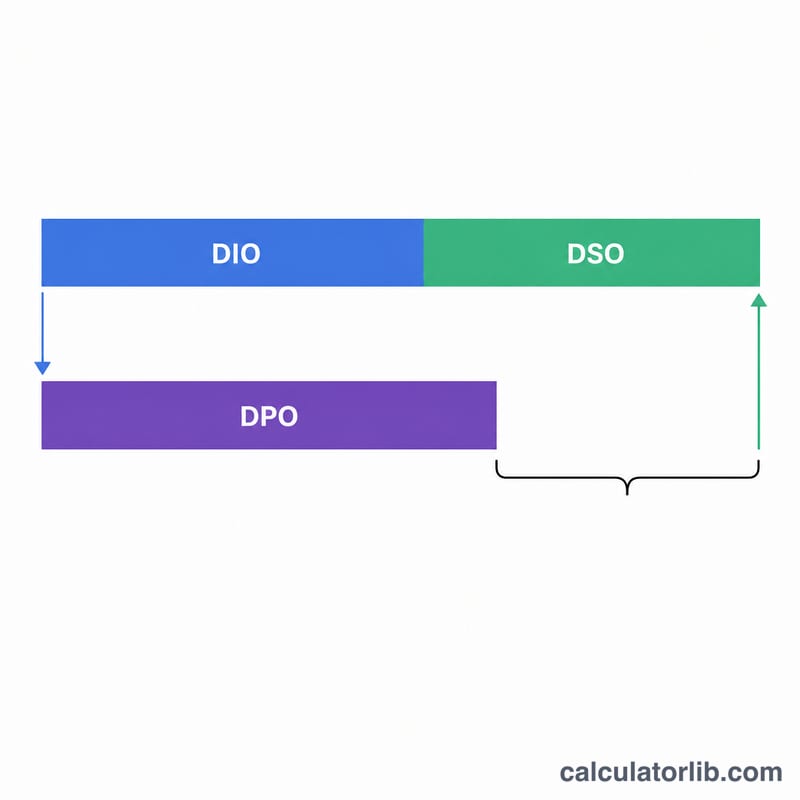

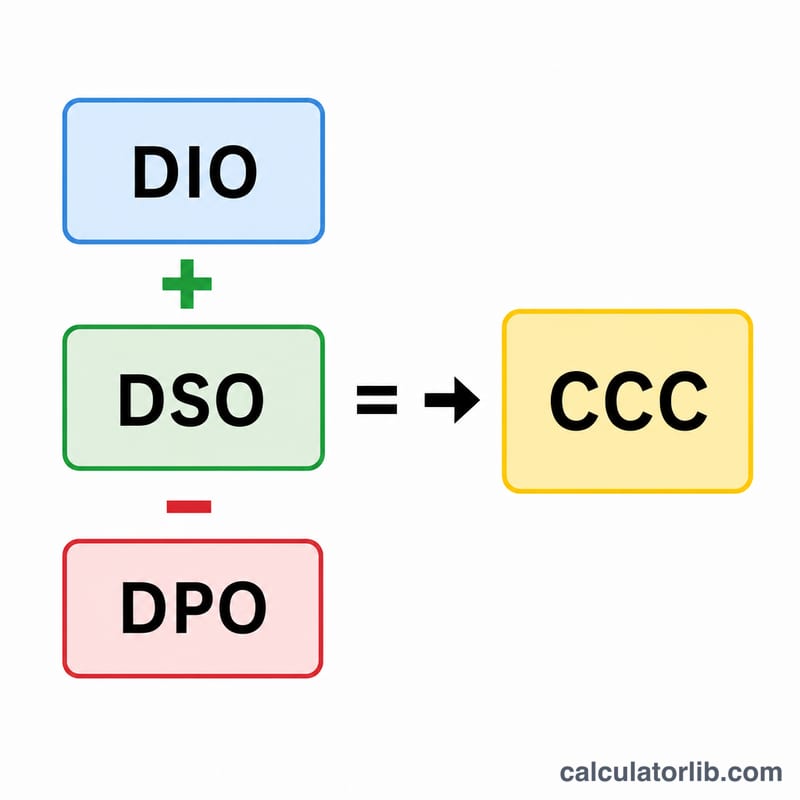

The cycle is built from three components:

$$\text{CCC} = \text{DIO} + \text{DSO} - \text{DPO}$$

DIO = \((\text{Average Inventory} \div \text{COGS}) \times 365\) — how long inventory sits before being sold. DSO = \((\text{Average Accounts Receivable} \div \text{Revenue}) \times 365\) — how long it takes to collect from customers. DPO = \((\text{Average Accounts Payable} \div \text{COGS}) \times 365\) — how long you take to pay suppliers. Adding DIO and DSO gives the operating cycle; subtracting DPO credits the financing you receive from suppliers.

Worked Example

Suppose a company holds inventory for 60 days (DIO), collects receivables in 40 days (DSO), and pays suppliers in 30 days (DPO). Then $$\text{CCC} = 60 + 40 - 30 = \textbf{70 days}.$$ Cash is locked up for 70 days per cycle. If the firm negotiated 50-day payment terms instead, the CCC would drop to 50 days, freeing significant working capital.

FAQ

Can the CCC be negative? Yes. Retailers like Amazon often have a negative CCC because they collect from customers before paying suppliers, effectively using supplier credit to fund operations.

Is a lower CCC always better? Generally yes, since it improves liquidity. But an extremely low CCC achieved by stretching payables too far can strain supplier relationships, and very low inventory may cause stockouts.

What period should I use? Most analysts annualize using 365 days. Be consistent — use the same period basis for DIO, DSO, and DPO.