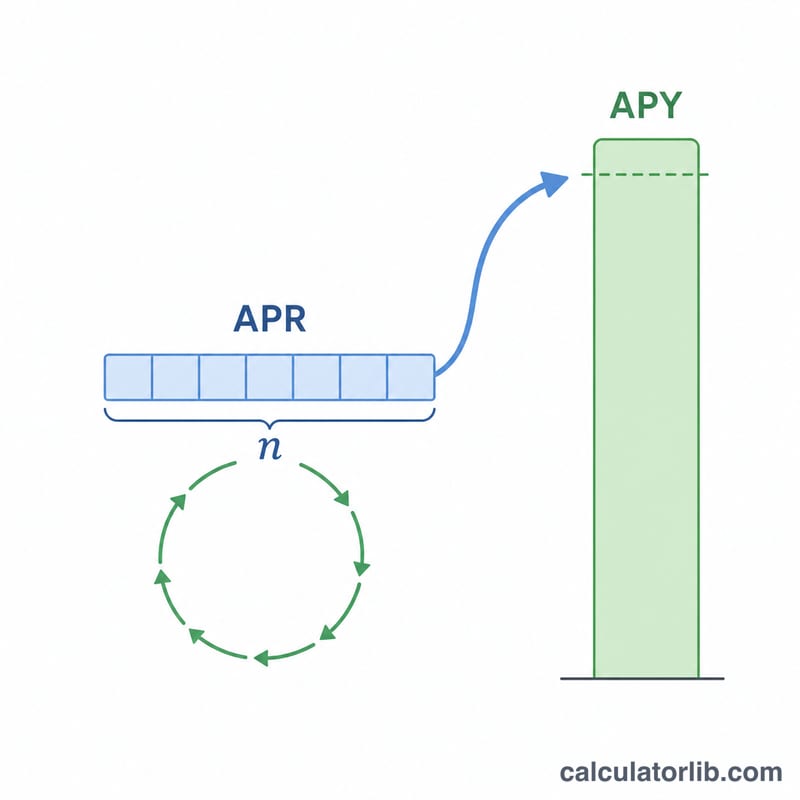

What Is the APY from APR Calculator?

This tool converts a nominal Annual Percentage Rate (APR) into the Annual Percentage Yield (APY), also called the effective annual rate. APR is the stated yearly interest rate, but when interest compounds more than once a year, the amount you actually earn (or pay) is higher. APY captures that compounding effect, giving you the true annual return.

How to Use It

Enter your nominal APR as a percentage and choose how often interest compounds — annually, semi-annually, quarterly, monthly, or daily. The calculator instantly returns the APY along with the compounding gain (APY minus APR).

The Formula Explained

The conversion uses:

$$\text{APY} = \left(1 + \frac{\text{APR}}{n}\right)^{n} - 1$$Here APR is expressed as a decimal and \(n\) is the number of compounding periods per year. Dividing APR by \(n\) gives the periodic rate; raising the growth factor to the power \(n\) compounds it across the whole year; subtracting 1 isolates the yield.

Worked Example

Suppose an account advertises a 5% APR compounded monthly (\(n = 12\)). Then $$\text{APY} = \left(1 + \frac{0.05}{12}\right)^{12} - 1 = (1.0041667)^{12} - 1 \approx 0.051162,$$ or about 5.1162%. The compounding gain is roughly 0.1162 percentage points over the plain 5% APR.

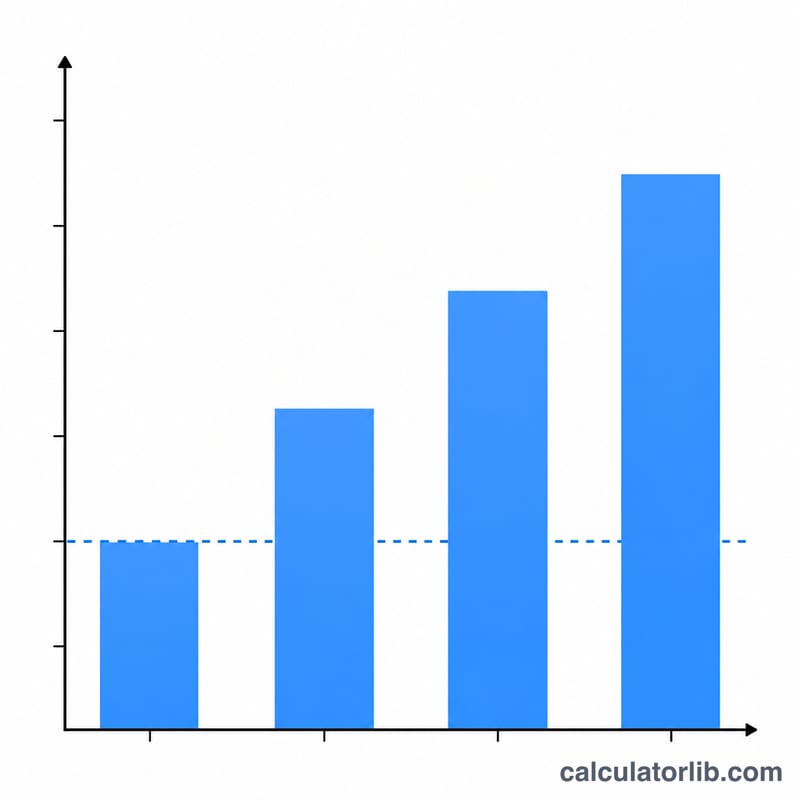

APR to APY Across Compounding Frequencies

The more often interest compounds, the higher the effective Annual Percentage Yield (APY) for a given nominal APR. The table below fixes the APR at 5% and applies the formula \(\text{APY} = \left(1 + \frac{\text{APR}/100}{n}\right)^{n} - 1\) for each compounding frequency. The compounding gain column shows how many extra percentage points the compounding adds over the plain 5% nominal rate.

| Compounding | Periods per year (n) | APY | Compounding gain vs APR |

|---|---|---|---|

| Annual | 1 | 5.0000% | 0.0000% |

| Semi-annual | 2 | 5.0625% | 0.0625% |

| Quarterly | 4 | 5.0945% | 0.0945% |

| Monthly | 12 | 5.1162% | 0.1162% |

| Daily | 365 | 5.1267% | 0.1267% |

Worked example (monthly): With APR = 5% and n = 12, the periodic rate is \(0.05/12 = 0.0041667\). Then \(\text{APY} = (1 + 0.0041667)^{12} - 1 = 1.051162 - 1 = 0.051162\), or about 5.1162%. Notice the gains shrink as you move from annual to daily — most of the benefit of compounding is captured by the time you reach monthly, with diminishing returns toward continuous compounding (which would give \(e^{0.05}-1 \approx 5.1271\%\)).

Key Terms Explained

- APR (Annual Percentage Rate)

- The nominal annual interest rate stated for an account or loan, before accounting for intra-year compounding. An APR of 5% compounded monthly does not mean you earn exactly 5% over the year — it means each month accrues at \(5\%/12\). APR is convenient for quoting and comparing stated rates, but it understates the true yearly return when compounding occurs more than once per year.

- APY / Effective Annual Rate (EAR)

- The effective annual rate of return after all within-year compounding is included. APY (the term used for deposits and savings) and EAR (the more general term) are computed the same way: \(\text{APY} = \left(1 + \frac{\text{APR}/100}{n}\right)^{n} - 1\). It is the single figure that lets you compare accounts with different compounding schedules on an apples-to-apples basis.

- Nominal rate

- Another name for the stated annual rate (the APR) that has not been adjusted for compounding frequency. "Nominal" here means "named" or "stated," not "adjusted for inflation" (a different economic use of the word).

- Periodic rate

- The interest rate applied to each individual compounding period, equal to \(\text{APR}/n\). For a 5% APR compounded monthly, the periodic (monthly) rate is \(5\%/12 \approx 0.4167\%\). Repeatedly applying the periodic rate over \(n\) periods is what produces the APY.

- Compounding frequency

- How often accrued interest is added to the balance so that it begins earning interest itself. Common frequencies are annual, semi-annual, quarterly, monthly, and daily. Higher frequency raises the APY for a fixed APR, though with diminishing additional benefit as frequency increases.

- n (periods per year)

- The number of compounding periods in one year — the exponent in the APY formula. Typical values: 1 (annual), 2 (semi-annual), 4 (quarterly), 12 (monthly), and 365 (daily). As \(n\) grows without bound, the APY approaches the continuous-compounding limit \(e^{\text{APR}/100} - 1\).

FAQ

What's the difference between APR and APY? APR is the simple nominal rate; APY includes the effect of compounding within the year, so \(\text{APY} \geq \text{APR}\) (equal only when compounding is annual).

Why does more frequent compounding give a higher APY? Because interest is calculated and added to the balance more often, each subsequent period earns interest on a slightly larger amount.

Is this useful for savings and loans? Yes. For savings it shows your true earnings; for loans it shows the true effective cost of borrowing.