What is the APR to APY Calculator?

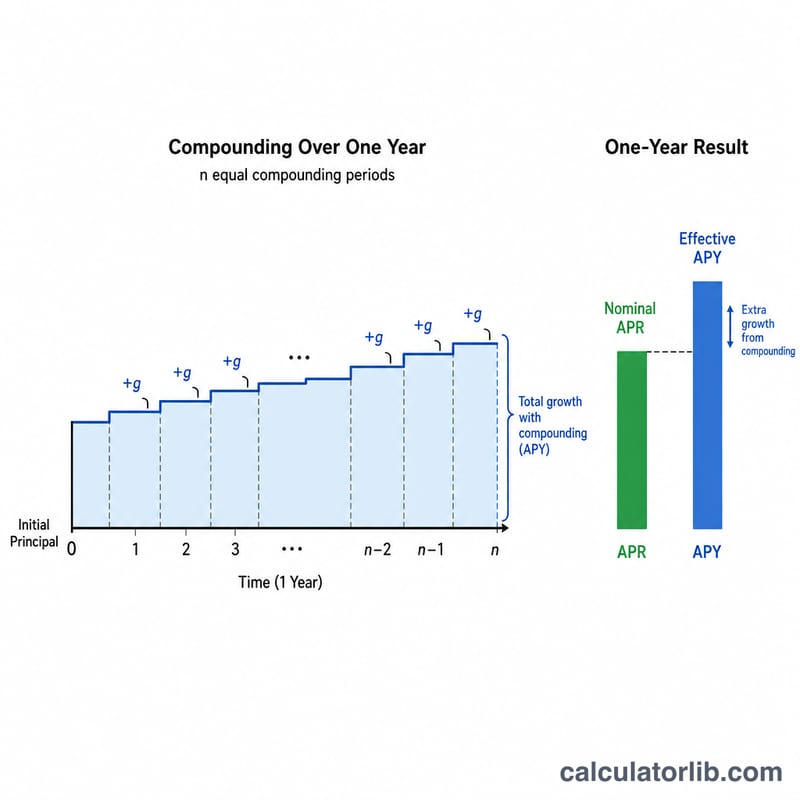

This tool converts a nominal Annual Percentage Rate (APR) into the Annual Percentage Yield (APY), also called the effective annual rate. APR is a simple stated rate, while APY accounts for the effect of compounding within the year. Because interest earned (or charged) is itself reinvested or accrued more than once a year, the APY is always equal to or greater than the APR — and the gap widens as the compounding frequency increases.

How to use it

Enter the nominal APR as a percentage (for example, 6 for 6%) and choose how many times the interest compounds per year: 12 for monthly, 4 for quarterly, 365 for daily, or 1 for annual. The calculator instantly returns the equivalent APY along with the difference between the two figures, so you can compare offers on an apples-to-apples basis.

The formula explained

The conversion uses:

$$\text{APY} = \left(1 + \frac{\text{APR}}{n}\right)^{n} - 1$$

Here APR is written as a decimal and \(n\) is the number of compounding periods per year. Each period applies a rate of \(\text{APR}/n\), and compounding it n times produces the effective annual growth factor. Subtracting 1 converts the growth factor back to a rate.

Worked example

Suppose an account quotes a 6% APR compounded monthly (\(n = 12\)). The monthly rate is \(0.06 / 12 = 0.005\). Then $$\text{APY} = (1 + 0.005)^{12} - 1 = 1.0616778 - 1 = 0.0616778,$$ or about 6.1678%. So a 6% APR actually yields roughly 6.17% per year — about 0.17 percentage points more than the stated APR.

APR to APY Across Compounding Frequencies

The effective annual yield (APY) grows as compounding becomes more frequent, even though the stated APR is unchanged. The discrete formula is:

$$\text{APY} = \left(1 + \frac{\text{APR}/100}{n}\right)^{n} - 1$$As \(n \to \infty\) the result approaches the continuous-compounding limit \(e^{\text{APR}/100} - 1\). The two tables below hold the APR fixed and vary the number of compounding periods per year.

APR fixed at 6%

| Compounding | Periods per year (n) | Resulting APY |

|---|---|---|

| Annual | 1 | 6.0000% |

| Semi-annual | 2 | 6.0900% |

| Quarterly | 4 | 6.1364% |

| Monthly | 12 | 6.1678% |

| Daily | 365 | 6.1831% |

| Continuous | ∞ | 6.1837% |

APR fixed at 12% (wider gap)

| Compounding | Periods per year (n) | Resulting APY |

|---|---|---|

| Annual | 1 | 12.0000% |

| Semi-annual | 2 | 12.3600% |

| Quarterly | 4 | 12.5509% |

| Monthly | 12 | 12.6825% |

| Daily | 365 | 12.7475% |

| Continuous | ∞ | 12.7497% |

At 6% APR the spread between annual and daily compounding is about 0.18 percentage points; at 12% APR it widens to roughly 0.75 points, because compounding effects scale with the size of the periodic rate.

Key Terms Defined

- APR (Annual Percentage Rate)

- The nominal annual interest rate, stated without accounting for intra-year compounding. It is the figure most often quoted on loans and credit cards. By itself the APR does not tell you the true yearly cost unless you also know how often interest compounds.

- APY / Effective Annual Yield

- The Annual Percentage Yield (also called the effective annual rate or effective annual yield) is the actual annual rate after compounding is included. It is always greater than or equal to the APR, and the two are equal only when interest compounds exactly once per year.

- Compounding frequency (n)

- The number of times per year interest is calculated and added to the balance: 1 (annual), 2 (semi-annual), 4 (quarterly), 12 (monthly), 52 (weekly), or 365 (daily). A larger \(n\) produces a higher APY for the same APR.

- Nominal vs. effective rate

- The nominal rate (APR) is the simple stated rate; the effective rate (APY) reflects interest earned on previously credited interest. The conversion between them is \(\text{APY} = \left(1 + \tfrac{\text{APR}/100}{n}\right)^{n} - 1\).

- Periodic rate (APR/n)

- The interest rate applied in a single compounding period — the APR divided by the number of periods per year. For example, an 18% APR compounded monthly has a periodic rate of \(18\%/12 = 1.5\%\) per month.

FAQ

Is APY always higher than APR? Yes, whenever there is more than one compounding period per year. With annual compounding (\(n = 1\)) they are equal.

Which should I compare when shopping for savings? APY, because it reflects the true return after compounding and lets you compare accounts with different compounding schedules fairly.

Does this include fees? No. APR sometimes bundles fees in lending contexts, but this calculator treats APR purely as a nominal interest rate and converts it mathematically to APY.