What Is the ACB Compound Interest Deposit Calculator?

This calculator shows how much a one-time deposit will grow over time when interest compounds. Compound interest means you earn interest not only on your original principal but also on the interest already added — so your balance accelerates the longer the money stays invested.

How to Use It

Enter your initial deposit (principal), the annual interest rate as a percentage, the term in years, and how often interest is compounded (annually, semi-annually, quarterly, monthly, or daily). The calculator instantly returns the future value at maturity along with the total interest earned.

The Formula Explained

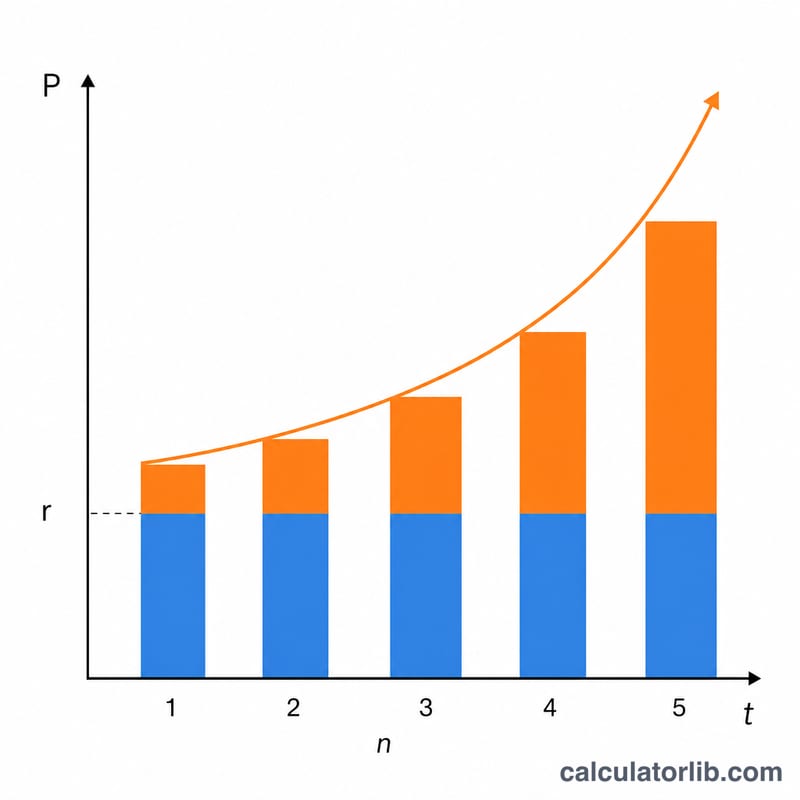

The future value is calculated as $$FV = P \times \left(1 + \dfrac{r/100}{n}\right)^{n \cdot t}$$ where P is the principal, r is the annual rate in percent, n is the number of compounding periods per year, and t is the number of years. Dividing the rate by \(n\) gives the per-period rate, and the exponent \(n \cdot t\) is the total number of compounding periods. More frequent compounding produces slightly higher returns.

Worked Example

Suppose you deposit $10,000 at a 5% annual rate, compounded monthly for 10 years. Here n = 12 and t = 10, so the monthly rate is \(0.05/12 \approx 0.0041667\) and there are 120 periods. $$FV = 10{,}000 \times (1.0041667)^{120} \approx \$16{,}470.09$$ meaning you earn about $6,470.09 in interest.

Key Terms Defined

- Principal (P)

- The initial amount deposited — the starting balance on which interest first accrues.

- Annual interest rate (r)

- The stated, or nominal, yearly rate quoted as a percentage (e.g. 5%). In the formula it is used as a decimal, \(r = 0.05\).

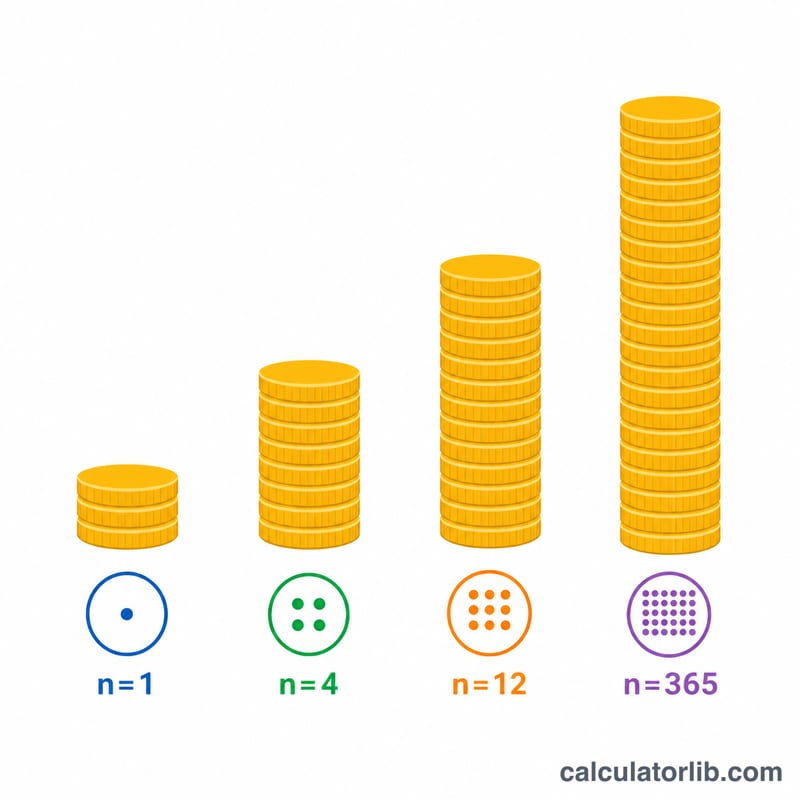

- Compounding frequency (n)

- How many times per year interest is calculated and added to the balance: 1 (annual), 2 (semi-annual), 4 (quarterly), 12 (monthly), or 365 (daily). Each period applies a rate of \(r/n\).

- Term (t)

- The length of the deposit in years. The total number of compounding periods is \(n \times t\).

- Future value (A)

- The total balance at the end of the term, including the original principal plus all accumulated interest.

- Interest earned

- The growth attributable to interest alone: \(A - P\). It excludes the principal you contributed.

- Maturity

- The date the term ends and the future value becomes available. For a CD or term deposit, withdrawing before maturity may forfeit interest.

- Nominal rate vs. effective annual yield (APY)

- The nominal rate is the quoted annual figure ignoring within-year compounding. The effective annual yield (APY) reflects compounding and is always \(\geq\) the nominal rate: \(\text{APY} = \left(1+\frac{r}{n}\right)^{n} - 1\). Two accounts with the same nominal rate but different \(n\) have different APYs.

Understanding Your Result

The calculator returns two figures. The future value \(A\) is everything you would hold at maturity — your original deposit plus interest. The interest earned is just the gain, \(A - P\), which is the number to compare against inflation or alternative investments.

From nominal rate to effective yield. Because interest compounds \(n\) times a year, the rate you actually realize exceeds the quoted rate. For 5% compounded monthly:

$$\text{APY} = \left(1 + \frac{0.05}{12}\right)^{12} - 1 = 0.05116 = 5.116\%$$So a "5% monthly" account behaves like a 5.116% account compounded once a year. When comparing offers, always compare APY, not nominal rate — it is the only figure that fairly accounts for differing compounding schedules.

Results are gross. The future value shown is pre-tax and pre-inflation. Interest is typically taxable in the year it is credited, so your after-tax yield is lower; a 5% return taxed at 25% nets roughly 3.75%. Separately, inflation erodes purchasing power — if prices rise 3% a year, a 5% nominal return delivers only about 2% in real terms. To gauge true growth, subtract your marginal tax rate and expected inflation from the nominal rate.

Why nominal and realized yield diverge. The more frequently interest compounds, the sooner earned interest itself starts earning interest, so the realized (effective) yield climbs above the nominal rate. The gap widens with higher rates and higher \(n\), but it has a ceiling: as \(n \to \infty\), growth approaches continuous compounding, \(A = Pe^{rt}\). That is why the jump from monthly to daily compounding is barely noticeable.

This is general educational information, not financial advice. Confirm rates, compounding terms, and tax treatment with your financial institution before relying on any projection.

FAQ

Does more frequent compounding always pay more? Yes, but with diminishing returns. Daily compounding earns only marginally more than monthly at the same rate.

Does this account for taxes or fees? No. The result is a gross figure before any taxes, fees, or inflation adjustments.

Can I use a fractional term? Yes — enter values like 2.5 years to model partial periods.