What is a Bond?

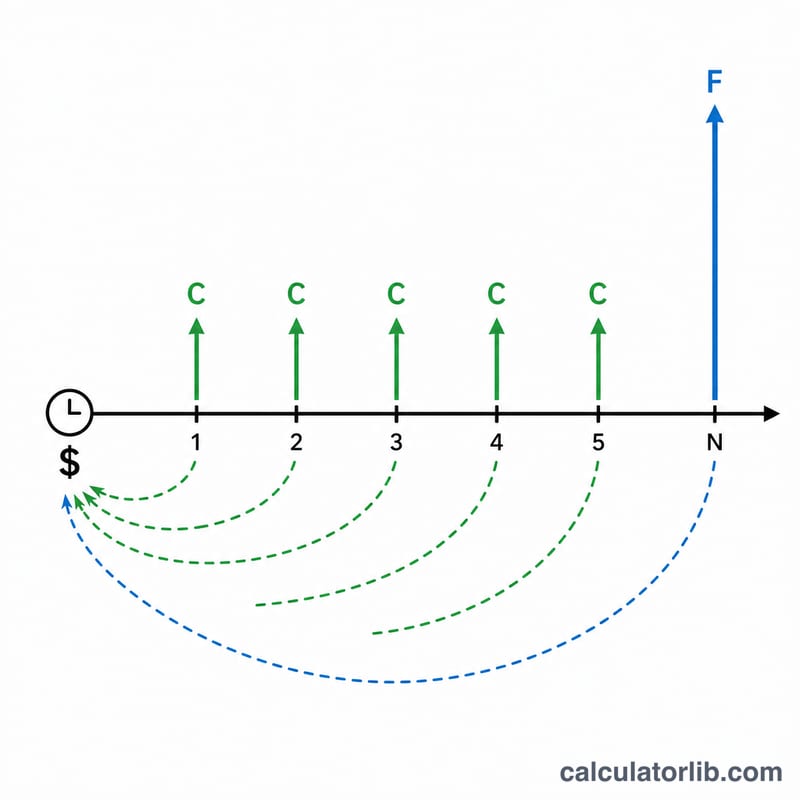

A bond is a fixed-income security — a loan from the investor to the issuer (a government or corporation) in exchange for periodic interest payments (coupons) and the return of principal (face value) at maturity. Because cashflows are predetermined, a bond's value can be computed exactly given its yield, or its yield computed exactly given its price.

The Two Modes

- Quick Bond Pricing assumes the bond settles exactly on a coupon date — useful for back-of-envelope analysis. Choose to solve for either the price (given yield) or the yield (given price).

- Date-aware Pricing takes a settlement date and a maturity date and produces the dirty price (full PV including accrued interest), the clean price (quoted price excluding accrued), and the accrued interest. This is what you actually pay or receive when buying a bond mid-period.

Bond Pricing Formula

The price of a bond is the present value of its future cashflows discounted at the yield:

$$\text{Price} = C \times \frac{1-(1+y)^{-N}}{y} + F \times (1+y)^{-N}$$

- \(C\) = coupon payment per period (annual coupon ÷ frequency)

- \(y\) = periodic yield (annual yield ÷ frequency)

- \(N\) = total number of coupon periods (years × frequency)

- \(F\) = face value (par)

Solving for Yield

The yield-from-price problem has no closed-form solution because y appears in both the discount factor and the denominator of the annuity term. This calculator uses the bisection method — iteratively narrowing a range of possible yields by checking which half contains the target price — converging to high precision in around 80 iterations.

Coupon Frequency

Coupons can be paid annually (1/year), semi-annually (2/year, the U.S. standard), quarterly (4/year), or monthly (12/year). Higher frequency means earlier cashflows and slightly higher present value for any given yield. The annual yield is divided by the frequency to obtain the periodic yield.

Worked Example — Quick Mode

$1,000 face, 4% annual coupon paid annually, 5% yield, 10 years to maturity:

- \(C = \$1{,}000 \times 4\% = \$40\) per year

- \(N = 10\) periods (annual)

- \(y = 5\%\) per period

- $$\text{Price} = 40 \times \frac{1-1.05^{-10}}{0.05} + 1{,}000 \times 1.05^{-10}$$

- $$\text{Price} = 40 \times 7.7217 + 1{,}000 \times 0.6139 = \mathbf{\$922.78}$$

Dirty Price, Clean Price, and Accrued Interest

When a bond is bought between coupon dates, the buyer compensates the seller for interest already earned but not yet paid — the accrued interest. The full amount paid (the dirty price) equals the bond's true present value. The clean price is what's quoted on trading screens: dirty minus accrued. Accrued is computed as the periodic coupon multiplied by the fraction of the current coupon period that has elapsed.

Day-count Conventions

Different bond markets calculate "fraction of period" differently. This calculator supports the four conventions used by Excel's PRICE function:

- 30/360 (Bond basis) — treats every month as 30 days and every year as 360 days. Default for U.S. corporate and municipal bonds.

- Actual/360 — uses actual elapsed days but assumes 360-day years. Common for money-market instruments.

- Actual/365 — actual days, 365-day year.

- Actual/Actual — actual days, with each year's actual length (365 or 366). Standard for U.S. Treasuries.

The choice of convention can shift the dirty price by a few basis points — small but material when trading large sizes.

Bond Pricing Caveats

- Yield is a single rate — real bonds discount each cashflow at the spot rate for that maturity, not a single yield. The bond's "yield to maturity" is the constant rate that makes PV equal to the market price — useful but a simplification.

- Default risk — this calculator assumes coupons and principal are paid in full and on time. Risky bonds trade at a higher yield to compensate for default probability.

- Reinvestment risk — the implicit assumption is that coupons are reinvested at the same yield, which rarely holds in practice.

- Embedded options — callable, putable, or convertible bonds need option-adjusted spread analysis, beyond what this calculator covers.

Interpreting Your Bond Price and Yield

A bond's price is the present value (PV) of its remaining cash flows — the stream of coupon payments plus the face value returned at maturity — discounted at the yield. The relationship between the coupon rate and the yield tells you immediately whether the bond trades above, below, or at par.

- Premium (price > par): When the coupon rate is higher than the yield, investors pay more than face value because the above-market coupons are worth a premium. A $1,000 bond might trade at $1,085.

- Discount (price < par): When the coupon rate is lower than the yield, the bond trades below face value to compensate the buyer for the below-market coupon — e.g. a price of $920 on a $1,000 bond.

- Par (price = par): When the coupon rate equals the yield exactly, the price equals the face value (par), since each coupon is discounted at precisely the rate it pays.

Yield to maturity (YTM) is the single discount rate \(y\) that makes the present value of all future cash flows equal the current price. It is an internal rate of return assuming you (1) hold the bond to maturity and (2) reinvest every coupon at that same YTM. If reinvestment occurs at a different rate, your realized return will differ from the quoted YTM.

Price and yield move inversely: as the required yield rises, the PV of fixed future cash flows falls, so the price drops — and vice versa. The size of that price move grows with maturity (longer bonds are more sensitive), an effect measured by duration.

Finally, the price you compute splits into two figures. The clean price is what is quoted in the market and excludes interest earned since the last coupon. The dirty price (clean price + accrued interest) is what you actually pay on the settlement date. Accrued interest is the portion of the next coupon that has built up since the last payment, calculated using the bond's day-count convention.

Price Across Yield and Maturity Scenarios

The table below prices a $1,000 face-value bond with a 4% annual coupon paid semi-annually, at several yields to maturity and maturities. It shows how price diverges from par as yields move away from the 4% coupon, and how that divergence grows with maturity — the essence of interest-rate sensitivity (duration).

| Yield (YTM) | 2 yrs | 5 yrs | 10 yrs | 30 yrs | Status |

|---|---|---|---|---|---|

| 3% | $1,019.27 | $1,046.11 | $1,085.84 | $1,196.85 | Premium |

| 4% | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | Par |

| 5% | $981.19 | $956.24 | $922.05 | $845.57 | Discount |

| 6% | $962.83 | $914.70 | $851.23 | $722.74 | Discount |

Two patterns stand out. First, at the 4% yield the price equals par at every maturity because coupon equals yield. Second, for a given yield change away from par, the price moves much more for long maturities than short ones: a shift from 4% to 6% costs only about $37 on the 2-year bond but roughly $277 on the 30-year bond — longer duration means greater price sensitivity.

Key Bond Terms

- Face (par) value

- The principal amount repaid to the holder at maturity, and the base on which coupons are calculated — commonly $1,000.

- Coupon rate

- The annual interest rate stated on the bond, applied to face value to determine the total annual coupon payment.

- Coupon frequency

- How many times per year coupons are paid — annual (1), semi-annual (2), quarterly (4), or monthly (12). Each period pays the annual coupon divided by the frequency.

- Yield to maturity (YTM)

- The single annualized discount rate that equates the present value of all future cash flows to the bond's price, assuming it is held to maturity and coupons are reinvested at that rate.

- Periodic yield

- The YTM divided by the number of coupon periods per year (\(y = \text{YTM}/k\)); this is the rate actually used to discount each period's cash flow.

- Clean price

- The quoted market price of a bond, excluding any interest accrued since the last coupon payment.

- Dirty price

- The full amount paid by the buyer on settlement: clean price plus accrued interest.

- Accrued interest

- The share of the upcoming coupon that has accumulated between the last coupon date and the settlement date, computed using the day-count convention.

- Settlement date

- The date on which the trade settles and ownership (and payment) actually transfers — the date as of which the price is calculated.

- Maturity date

- The date the bond's principal (face value) is repaid and coupon payments cease.

- Day-count convention

- The rule for counting days between dates when computing accrued interest and period fractions — e.g. 30/360, Actual/360, Actual/365, or Actual/Actual.

- Present value (PV)

- The current worth of a future cash flow, found by discounting it back at the periodic yield; a bond's price is the sum of the PVs of all its cash flows.