What Is Yield to Maturity?

Yield to maturity (YTM) is the total annual return an investor can expect if a bond is held until it matures, assuming all coupon payments are made on schedule and reinvested. It combines the income from coupons with any capital gain or loss between the purchase price and the face value repaid at maturity. Because YTM accounts for both income and price, it is the most common way to compare bonds with different prices, coupons, and terms.

How to Use This Calculator

Enter the bond's face value (the amount repaid at maturity, often $1,000), the current market price you would pay, the annual coupon rate as a percentage, and the number of years to maturity. The calculator returns the approximate YTM along with the annual coupon payment and the current yield for comparison.

The Formula Explained

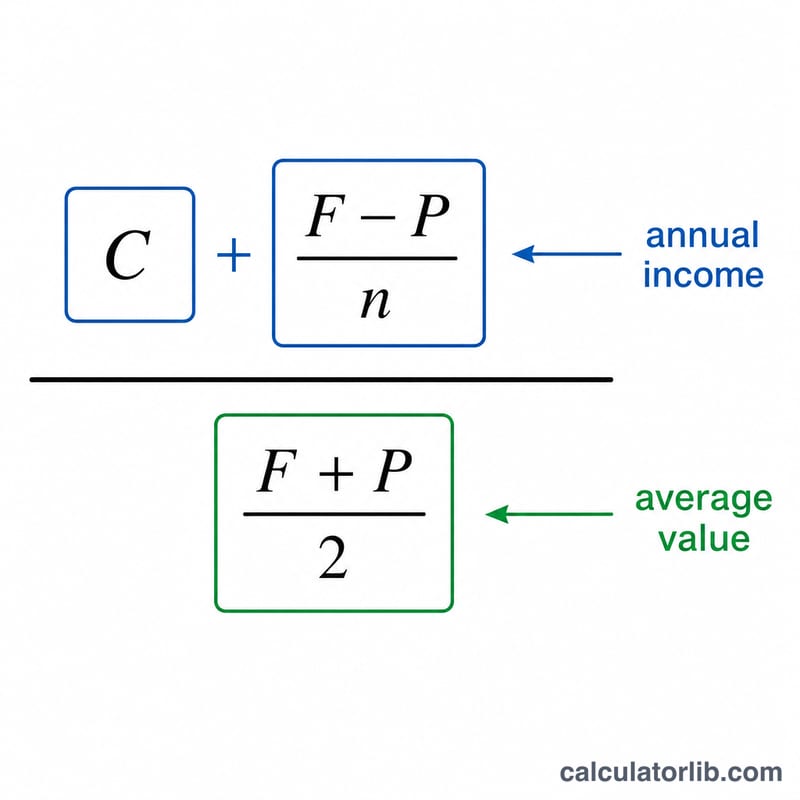

This tool uses the widely taught approximate (or "shortcut") YTM formula:

$$\text{YTM} \approx \frac{C + \dfrac{F - P}{n}}{\dfrac{F + P}{2}}$$

Here \(C\) is the annual coupon payment, \(F\) is the face value, \(P\) is the current price, and \(n\) is the number of years remaining. The numerator adds the coupon income to the average annual capital gain or loss, while the denominator is the average of the face value and price. The result is an estimate that is very close to the true (internal-rate-of-return) YTM for bonds trading near par.

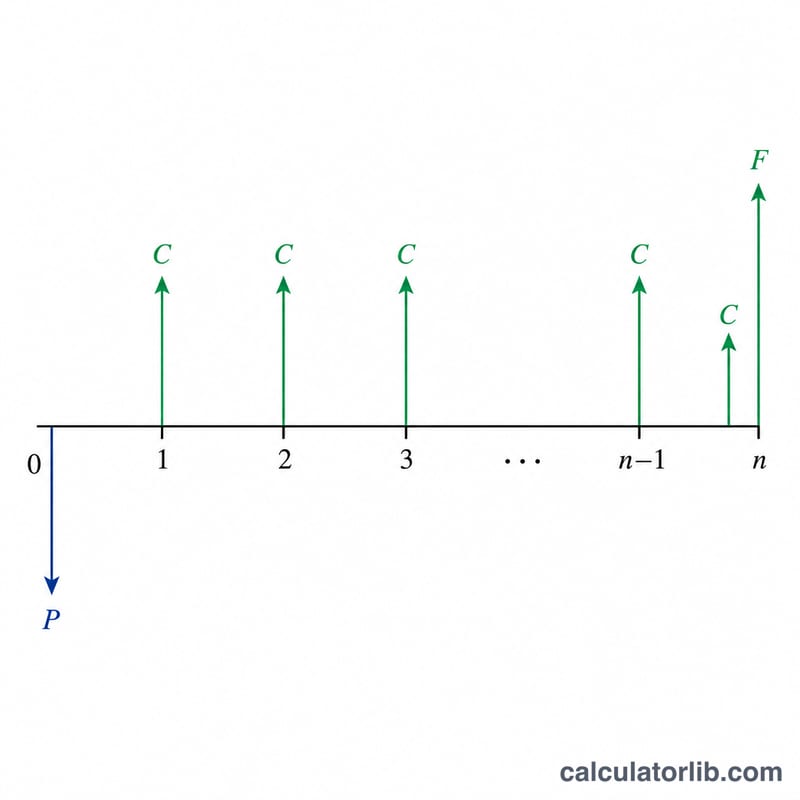

Worked Example

Suppose a bond has a $1,000 face value, currently trades at $920, pays a 6% coupon, and matures in 12 years. The annual coupon is \(\$1{,}000 \times 6\% = \$60\). Then $$\text{YTM} \approx \frac{60 + \dfrac{1000 - 920}{12}}{\dfrac{1000 + 920}{2}} = \frac{60 + 6.667}{960} = \frac{66.667}{960} \approx 6.94\%.$$

Interpreting Your YTM Result

Yield to maturity is the single annualized return you earn if you buy a bond at its current price and hold it to maturity, collecting every coupon and the final face value. Its relationship to the coupon rate depends entirely on the price you pay relative to par:

- Discount bond (P < F): YTM > coupon rate. You receive the coupons and a capital gain as the price pulls toward par at maturity, so your total return exceeds the stated coupon.

- Par bond (P = F): YTM = coupon rate. There is no capital gain or loss, so the only return is the coupon.

- Premium bond (P > F): YTM < coupon rate. The price declines toward par over time, and that capital loss drags total return below the coupon rate.

YTM vs. current yield. Current yield is simply the annual coupon divided by price; it measures only the income return at today's price and ignores any gain or loss at maturity. YTM incorporates that pull-to-par effect. As a result, current yield always lies between the coupon rate and the YTM. Comparing the two tells you how much of your expected return comes from coupons versus from price convergence.

On the approximation. This calculator uses the standard approximate-YTM formula, which spreads the total price-to-par gain or loss evenly across the years rather than discounting each cash flow precisely. It is accurate near par but drifts further from the true (internal-rate-of-return) YTM the further the price moves away from face value, and the gap widens with longer maturities. For deep discounts or large premiums, treat the figure as a close estimate and confirm with a full present-value bond calculation.

This is general educational information about how bond yields are calculated, not investment advice.

FAQ

Is this the exact YTM? No — it is a fast approximation. The exact YTM requires solving for the discount rate that equates the bond's price to the present value of all its cash flows, which has no closed-form solution. The approximation is typically within a few basis points for bonds near par.

What is the difference between YTM and current yield? Current yield is just the annual coupon divided by the price and ignores capital gain or loss at maturity. YTM includes that gain or loss, making it a fuller measure of return.

Why is YTM higher when a bond trades below face value? Buying below par means you also earn the difference between price and face value at maturity, which boosts your total return above the coupon rate.