What Is the AMT Calculator?

This calculator applies to the United States federal tax system. The Alternative Minimum Tax (AMT) is a parallel tax designed to ensure that taxpayers who claim large deductions or preference items still pay a minimum amount of tax. This tool gives a simplified estimate of any additional AMT you may owe on top of your regular tax liability. It is for planning only — exemption amounts, phase-outs and AMT rate brackets change each tax year, so confirm current figures with the IRS or a tax professional.

How to Use It

Enter your regular taxable income, the total of your AMT preference items and adjustments (such as certain ISO exercises, private-activity bond interest, or accelerated depreciation), your AMT exemption amount, your regular tax liability, and the applicable AMT rate (commonly 26% or 28%). The calculator computes your Alternative Minimum Taxable Income (AMTI), the tentative minimum tax, and how much, if any, AMT is added on top of your regular tax.

The Formula Explained

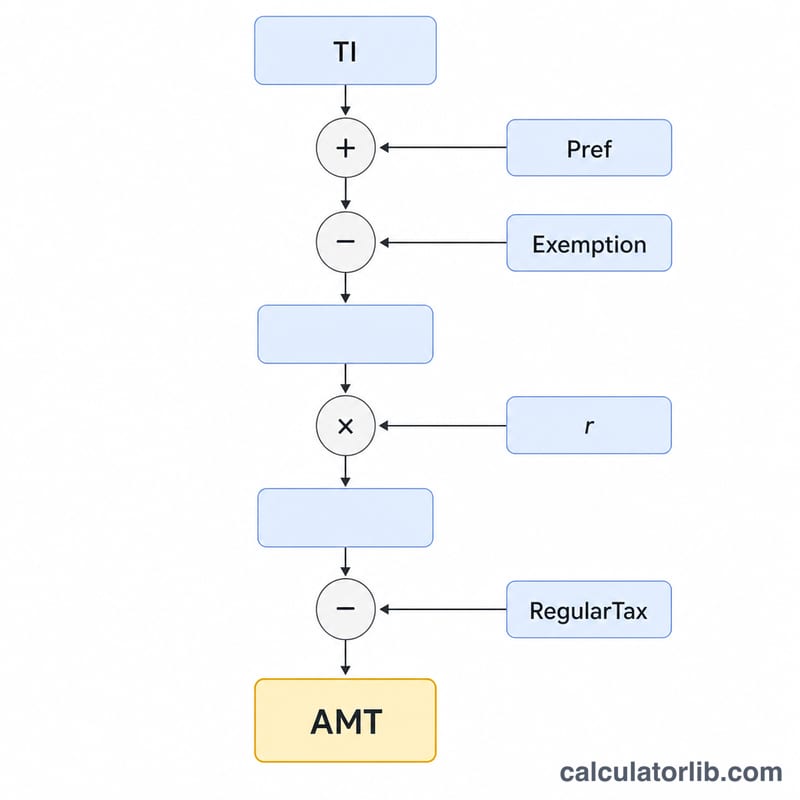

First, \(\text{AMTI} = \text{Taxable Income} + \text{Preferences} - \text{Exemption}\).

$$\text{AMTI} = \text{TI} + \text{Preferences} - \text{Exemption}$$The tentative minimum tax is \(\text{AMTI} \times \text{AMT rate}\). You owe AMT only when this tentative tax exceeds your regular tax:

$$\text{AMT} = \max\left(0,\; (\text{TI} + \text{Pref} - \text{Exemption}) \times r - \text{RegularTax}\right)$$Your total tax becomes regular tax plus that AMT amount.

Worked Example

Suppose taxable income is $200,000, preference items total $50,000, the exemption is $85,700, and the AMT rate is 26%.

$$\text{AMTI} = 200{,}000 + 50{,}000 - 85{,}700 = \$164{,}300$$Tentative minimum tax:

$$164{,}300 \times 0.26 = \$42{,}718$$If your regular tax is $38,000, then

$$\text{AMT} = 42{,}718 - 38{,}000 = \$4{,}718$$of additional tax, for a total of $42,718.

AMT Exemption Amounts and Phase-Out Thresholds

The Alternative Minimum Tax exemption shields a base amount of alternative minimum taxable income (AMTI) from the AMT. The exemption itself phases out at 25 cents per dollar of AMTI above the phase-out threshold, and a two-tier rate structure applies: 26% on AMTI up to a breakpoint and 28% on the portion above it.

| Tax Year / Filing Status | AMT Exemption | Phase-Out Begins (AMTI) | 26% / 28% Rate Breakpoint |

|---|---|---|---|

| 2024 Single / Head of Household | $85,700 | $609,350 | $232,600 |

| 2024 Married Filing Jointly | $133,300 | $1,218,700 | $232,600 |

| 2024 Married Filing Separately | $66,650 | $609,350 | $116,300 |

| 2023 Single / Head of Household | $81,300 | $578,150 | $220,700 |

| 2023 Married Filing Jointly | $126,500 | $1,156,300 | $220,700 |

| 2023 Married Filing Separately | $63,250 | $578,150 | $110,350 |

Above the phase-out threshold, the exemption is reduced by 25% of the excess AMTI and is fully eliminated once AMTI is large enough. The breakpoint shown is the AMTI level above which the 28% rate replaces the 26% rate. Note that this calculator uses a single AMT rate you supply; for a precise figure, the two-tier 26%/28% schedule on IRS Form 6251 applies.

Key AMT Terms Defined

- Alternative Minimum Taxable Income (AMTI)

- Your taxable income recalculated for AMT purposes — regular taxable income with certain deductions disallowed and preference items added back, before subtracting the AMT exemption.

- Preference Items / Adjustments

- Amounts that receive favorable treatment under the regular tax but must be added back (or recomputed) for AMT, such as the standard deduction, state and local tax deductions, certain depreciation, and incentive stock option spreads.

- Tentative Minimum Tax (TMT)

- The tax computed by applying the AMT rate(s) to AMTI after the exemption. AMT owed equals TMT minus your regular tax, but never less than zero.

- AMT Exemption

- A filing-status-based amount subtracted from AMTI before applying the AMT rate, which keeps most lower- and middle-income taxpayers out of AMT.

- Exemption Phase-Out

- The gradual reduction of the AMT exemption — 25 cents lost per dollar of AMTI above the phase-out threshold — until the exemption reaches zero for high earners.

- ISO Exercise Spread

- The difference between the fair market value and the exercise price when you exercise an incentive stock option (ISO) and hold the shares. It is invisible to the regular tax that year but is a major AMT preference item.

- Private-Activity Bond Interest

- Interest from certain tax-exempt municipal bonds that funds private projects; it is exempt from regular tax but added back as a preference item for AMT.

- Regular Tax Liability

- The income tax you compute under the ordinary rules. AMT applies only to the extent that the tentative minimum tax exceeds this amount.

What Your AMT Result Means

The calculator compares your tentative minimum tax (TMT) against your regular tax. There are two possible outcomes:

- AMT > 0: Your tentative minimum tax exceeded your regular tax, so the difference is added on top of your regular tax bill. For example, if AMTI is $300,000 at a 26% rate the TMT is $78,000; if your regular tax was $60,000, you owe an extra $18,000 in AMT.

- AMT = 0: Your regular tax already meets or exceeds the minimum, so no additional tax is due under the AMT system. This is the case for most taxpayers.

Keep in mind this is a simplified estimate. It applies the single AMT rate you enter and does not automatically model the exemption phase-out, the two-tier 26%/28% schedule, the AMT foreign tax credit, the separate capital-gains and qualified-dividend rate treatment, or AMT-specific depreciation. These factors can move your actual liability up or down significantly.

Treat the output as a planning indicator only. The authoritative calculation is IRS Form 6251, Alternative Minimum Tax — Individuals. Confirm any meaningful AMT exposure with Form 6251 or a qualified tax professional. This is general information, not professional tax advice, and no personal tax recommendation is being made.

FAQ

Who has to pay AMT? Taxpayers whose tentative minimum tax exceeds their regular tax — typically those with high incomes plus large preference items or deductions.

What rate should I use? The 2024 AMT rate is 26% on AMTI up to a threshold and 28% above it. Use 26% for a quick estimate at moderate income levels.

Is this an official figure? No. This is a simplified estimate that ignores exemption phase-outs, capital-gain treatment, and AMT credits. Use IRS Form 6251 for an exact calculation.