What Is a Call Option Payoff Calculator?

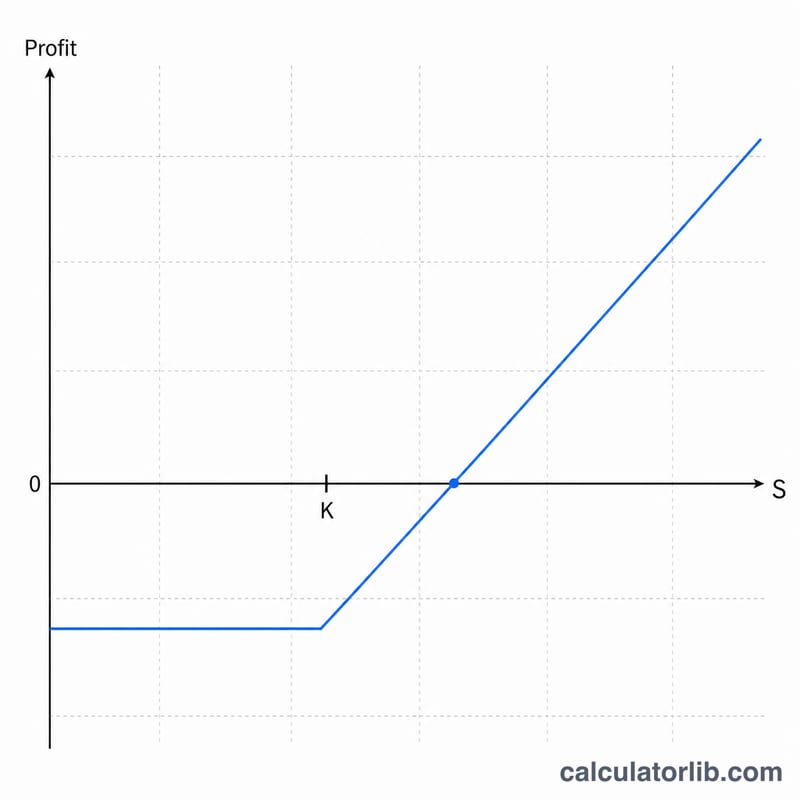

A call option gives the holder the right (not the obligation) to buy an underlying asset at a fixed strike price (\(K\)) before or at expiration. This calculator shows the payoff and profit or loss of a long call position at expiration based on the underlying's price (\(S\)), the strike price, and the premium you paid. It also reports the breakeven price and scales results across multiple contracts (each standard equity contract covers 100 shares).

How to Use It

Enter the underlying price at expiration, the strike price, the premium paid per share, and the number of contracts. The calculator returns the per-share payoff (intrinsic value), the per-share profit after premium, the total profit/loss for your position, and the breakeven price. Use it to compare scenarios before or after entering a trade.

The Formula Explained

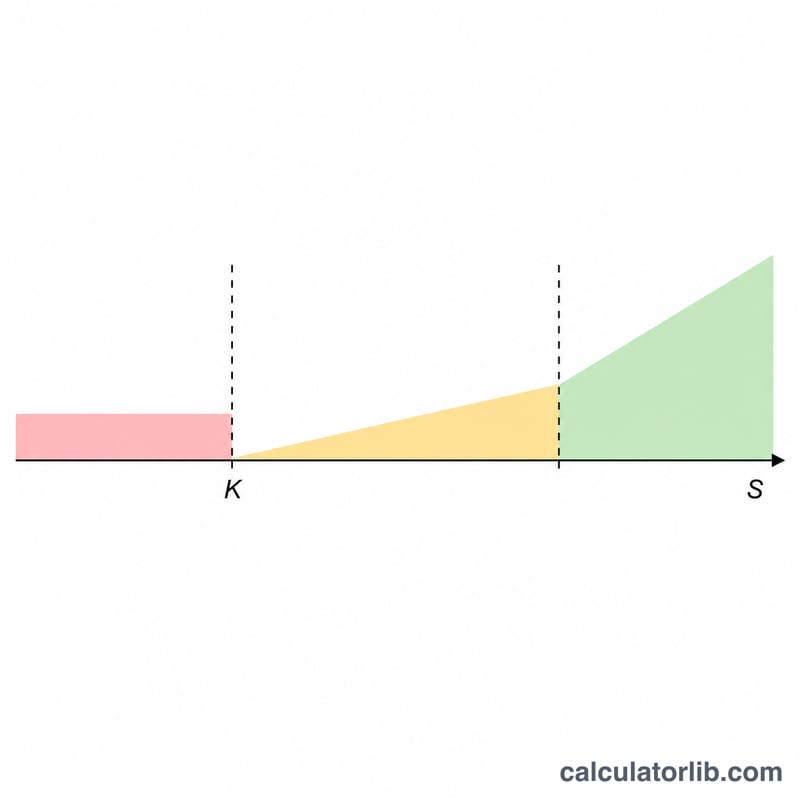

The payoff of a call at expiration is the intrinsic value: $$\text{Payoff} = \max(0,\ S - K)$$ If the underlying finishes above the strike, the option is worth \(S - K\); otherwise it expires worthless (payoff 0). Profit subtracts the upfront cost: $$\text{Profit} = \max(0,\ S - K) - \text{Premium}$$ The breakeven price — where profit is zero — is simply \(K + \text{Premium}\). Totals multiply per-share figures by shares \(= \text{contracts} \times 100\).

$$\text{Total Profit} = \Big[\max\!\big(0,\ S - K\big) - P\Big] \times 100 \times C$$

Worked Example

Suppose you buy 1 call with strike \(K = 100\) for a premium of 5, and at expiration the stock trades at \(S = 110\). Payoff per share \(= \max(0,\ 110 - 100) = 10\). Profit per share \(= 10 - 5 = 5\). With 100 shares, total profit \(= 5 \times 100 = \$500\). Breakeven \(= 100 + 5 = 105\).

$$\text{Total Profit} = \big[\max(0,\ 110 - 100) - 5\big] \times 100 \times 1 = \$500$$

FAQ

What if the stock ends below the strike? The call expires worthless, so your loss equals the total premium paid.

Does this include commissions or time value? No — it shows the payoff at expiration only; trading fees and pre-expiration time value are excluded.

What is the maximum loss? For a long call, the maximum loss is limited to the premium paid (\(\text{Premium} \times \text{shares}\)).