What is the Black-Scholes Call Calculator?

This tool prices a European call option on a non-dividend-paying underlying using the Black-Scholes (Black-Scholes-Merton) model. It is universal financial math — the formula applies identically in any market and currency. Continuous compounding of the risk-free rate is assumed, and time to maturity is expressed in years.

How to Use It

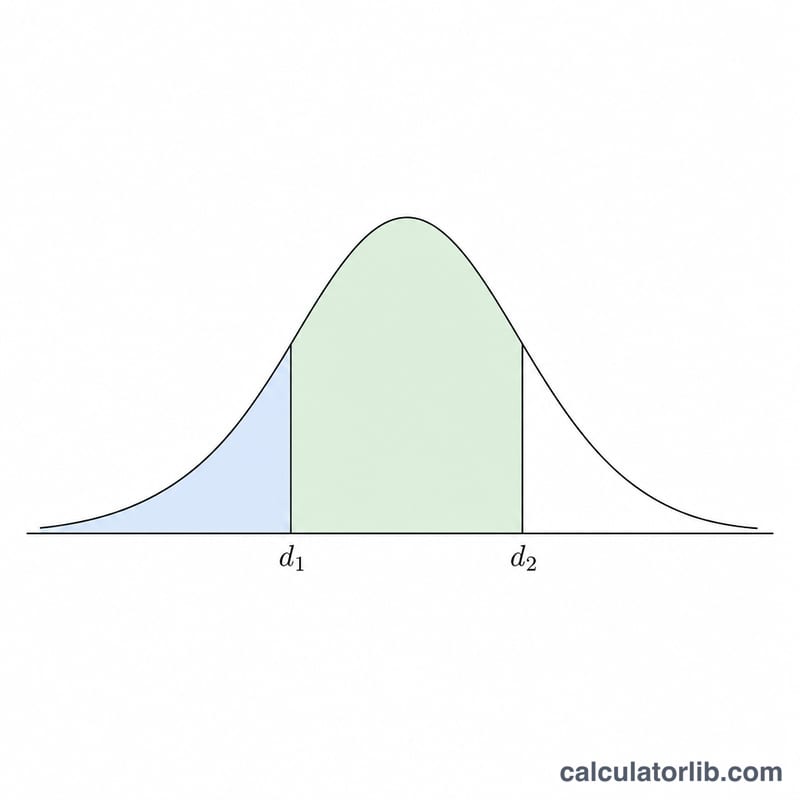

Enter the current spot price \(S\) of the underlying, the strike (exercise) price \(X\), the annual risk-free rate \(r\) in percent per year, the time to maturity \(T\) in years (e.g. two months = 0.16667), and the annualized volatility (standard deviation) \(\sigma\) in percent per year. The calculator returns the theoretical call premium plus the intermediate \(d_1\), \(d_2\), \(N(d_1)\) and \(N(d_2)\) terms.

The Formula Explained

With \(r\) and \(\sigma\) converted from percent to decimals:

$$d_1 = \frac{\ln(S/X) + \left(r + \tfrac{\sigma^2}{2}\right)T}{\sigma\sqrt{T}}$$ $$d_2 = d_1 - \sigma\sqrt{T}$$ $$C = S\,N(d_1) - X\,e^{-rT}\,N(d_2)$$Here \(N(\cdot)\) is the standard normal cumulative distribution function, computed as \(N(x) = 0.5\left(1 + \operatorname{erf}\!\left(x/\sqrt{2}\right)\right)\) with a rational erf approximation accurate to about \(10^{-7}\).

Worked Example

Take \(S = 14500\), \(X = 14000\), \(r = 6\%\), \(T = 2/12 = 0.16667\) years, \(\sigma = 38\%\). Then \(\sigma\sqrt{T} = 0.15513\), \(\ln(S/X) = 0.035091\), \(d_1 = 0.36823\), \(d_2 = 0.21310\), \(N(d_1) = 0.6437\), \(N(d_2) = 0.5844\), \(e^{-rT} = 0.99005\). The call price

$$C = 14500 \times 0.6437 - 14000 \times 0.99005 \times 0.5844 \approx 1233.1$$currency units.

Definitions & Glossary

- Spot price \(S\)

- The current market price of the underlying asset.

- Strike price \(X\)

- The fixed price at which the holder may buy the underlying at expiration.

- Risk-free rate \(r\)

- The continuously compounded annual interest rate on a risk-free investment over the option's life, expressed as a decimal in the formula.

- Time to maturity \(T\)

- The time remaining until expiration, measured in years (e.g. six months = 0.5).

- Volatility \(\sigma\)

- The annualized standard deviation of the underlying's continuously compounded returns, expressed as a decimal.

- \(d_1\)

- The standardized term \(d_1=\dfrac{\ln(S/X)+(r+\sigma^2/2)T}{\sigma\sqrt{T}}\); \(N(d_1)\) is the call's delta (sensitivity of premium to spot).

- \(d_2\)

- Defined as \(d_2=d_1-\sigma\sqrt{T}\).

- \(N(d_1)\), \(N(d_2)\)

- Values of the standard normal cumulative distribution function at \(d_1\) and \(d_2\), each between 0 and 1.

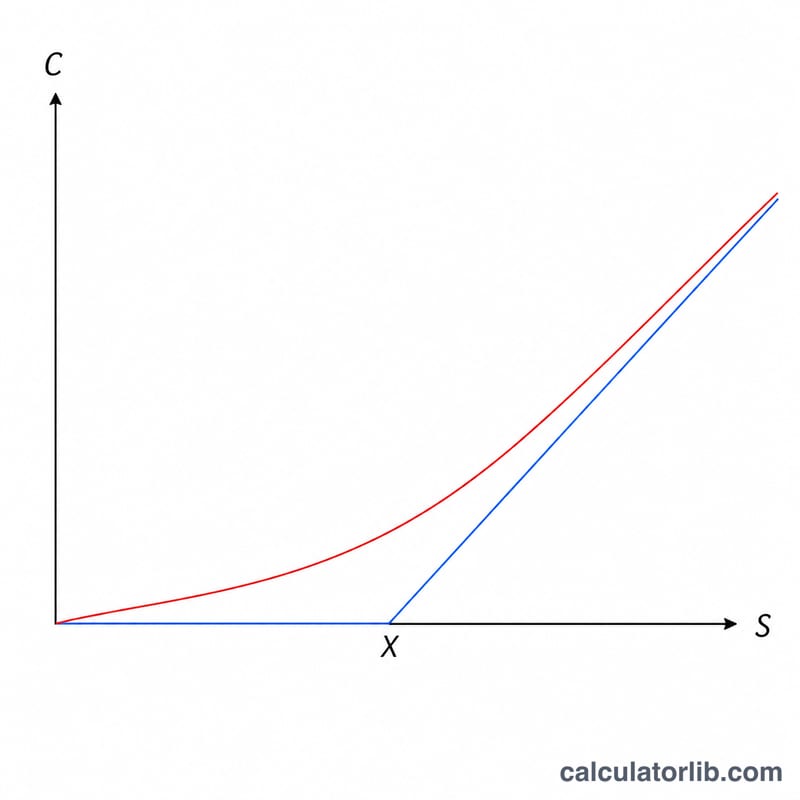

- European call

- An option giving the right, but not the obligation, to buy the underlying at the strike, exercisable only at expiration (not earlier).

- Premium \(C\)

- The theoretical fair value (price) of the call, the output of the formula.

- Intrinsic value

- The value if exercised immediately, \(\max(S-X,0)\) for a call.

- Time value

- The portion of the premium above intrinsic value, reflecting the remaining chance of further favorable moves: \(C-\max(S-X,0)\).

Interpreting Your Result

The output \(C\) is the theoretical fair premium for one unit of the underlying. To value a standard contract you multiply by the contract multiplier (commonly 100 shares per equity option contract).

In the formula, \(N(d_2)\) is the risk-neutral probability that the option finishes in-the-money (spot above strike at expiration), while \(N(d_1)\) is the option's delta — roughly how much the premium moves for a small change in spot, and the hedge ratio. The term \(X\,e^{-rT}\) is the strike discounted to present value at the continuously compounded risk-free rate.

You can split the premium into two parts:

- Intrinsic value \(=\max(S-X,0)\): what the call would be worth if exercised right now.

- Time value \(=C-\max(S-X,0)\): the remainder, reflecting the possibility of further favorable movement before expiration. Time value is largest when the option is near at-the-money and shrinks toward zero as maturity approaches.

Keep the model's assumptions in mind. The Black-Scholes European call price assumes no dividends, a constant volatility and risk-free rate, continuous trading with no transaction costs, lognormally distributed returns, and exercise only at expiration (European style). Real markets violate these assumptions to varying degrees, so the result is a benchmark estimate rather than a guaranteed market price. This is general educational information, not trading or investment advice.

FAQ

Does this handle dividends? No — it values a call on a non-dividend-paying underlying. For dividend-paying assets, use a continuous dividend yield variant.

How do I get the put price? Use put-call parity: \(P = C - S + X\,e^{-rT}\).

What does "standard deviation" mean here? It is the annualized volatility (often the implied volatility) of the underlying's returns, not a price standard deviation. Enter it as a percent per year.