What Is a Call Option Payoff?

A call option gives its holder the right (not the obligation) to buy an underlying asset at a fixed strike price (\(K\)) before or at expiry. This calculator shows the value and profit of a long call position at expiry, based on where the underlying price (\(S\)) ends up. It works for stock options, index options or any asset quoted with a contract multiplier.

How to Use It

Enter the underlying price at expiry, the strike price, the premium you paid per share, the number of contracts and the shares per contract (typically 100 for US equity options). The calculator returns the payoff per share, profit per share, total intrinsic value, total premium cost, your overall profit or loss and the breakeven price.

The Formula Explained

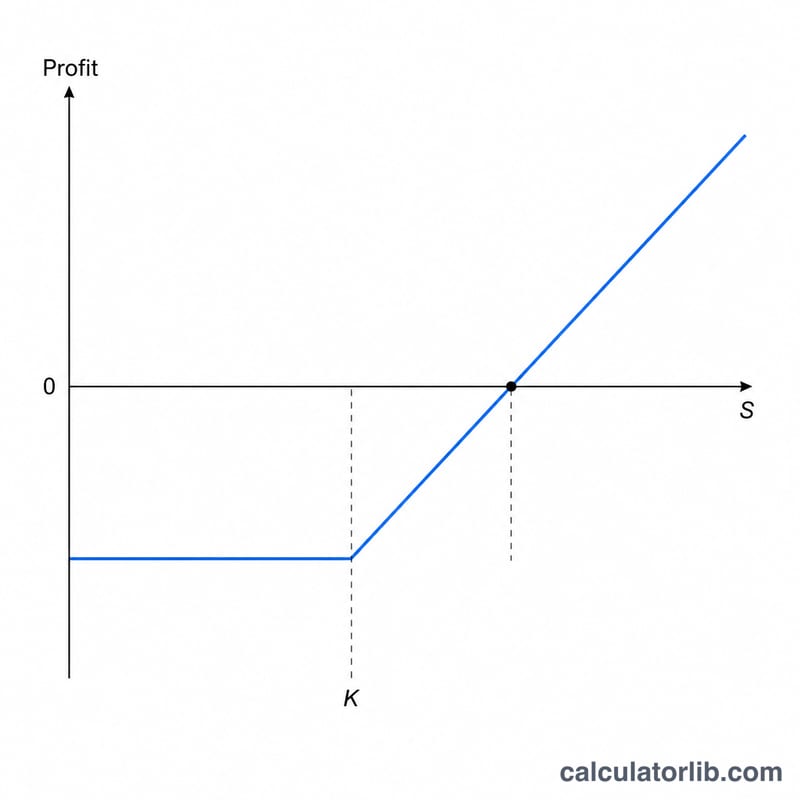

At expiry a call is worth its intrinsic value: $$\text{Payoff} = \max\!\left(S - K,\,0\right)$$ If the underlying finishes above the strike, the option is "in the money" and worth \(S - K\); otherwise it expires worthless at 0. Subtract the premium you originally paid to get profit per share: $$\text{Profit} = \max\!\left(S - K,\,0\right) - \text{Premium}$$ Multiply by shares (contracts \(\times\) multiplier) for the total. The position breaks even when \(S = K + \text{Premium}\).

Worked Example

Suppose you buy 1 contract (100 shares) of a call with strike $100 for a $5 premium, and the stock closes at $110. Payoff per share = \(\max(110 - 100,\,0) = \$10\). Profit per share = \(10 - 5 = \$5\). Total profit = \(5 \times 100 =\) $500. Breakeven = \(100 + 5 = \$105\).

Payoff Across Different Expiry Prices

The table below traces a single long call with a strike of \(K = \$100\) bought for a premium of \(P = \$5\) per share. A standard equity option controls \(M = 100\) shares, so one contract costs \(\$5 \times 100 = \$500\). At expiry the per-share payoff is \(\max(S - K,\,0)\), the per-share profit subtracts the premium, and the total P/L per contract multiplies by 100.

| Spot at Expiry \(S\) | Payoff / Share \(\max(S-K,0)\) |

Profit / Share \(\max(S-K,0)-P\) |

Total P/L per Contract | Zone |

|---|---|---|---|---|

| $90 | $0.00 | −$5.00 | −$500.00 | Worthless (max loss) |

| $100 | $0.00 | −$5.00 | −$500.00 | Worthless (at strike) |

| $105 | $5.00 | $0.00 | $0.00 | Breakeven |

| $110 | $10.00 | $5.00 | $500.00 | Profit |

| $120 | $20.00 | $15.00 | $1,500.00 | Profit |

The loss is capped at the premium paid (−$500) for any expiry price at or below the $100 strike — the worthless zone. Profit turns positive once the spot rises above the breakeven of \(K + P = \$100 + \$5 = \$105\), and gains then climb dollar-for-dollar with the underlying, giving the long call its theoretically unlimited upside.

FAQ

What happens if the stock finishes below the strike? The call expires worthless, payoff is 0, and your loss equals the total premium paid.

What is the breakeven price? It is the strike plus the premium per share — the underlying must exceed this for the trade to profit.

Does this account for time value or fees? No. This is the expiry payoff (intrinsic value only) and excludes commissions; before expiry an option may trade above its intrinsic value due to time value.