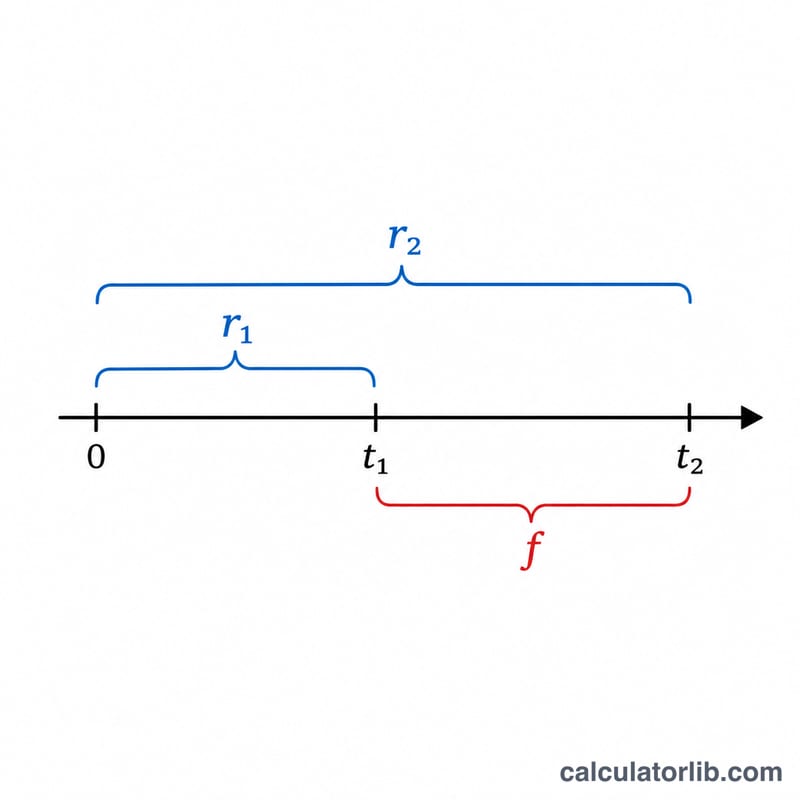

What Is the Forward Rate Calculator?

The forward rate is the interest rate implied today for a future period, derived from current spot rates of different maturities. It answers the question: "If I know the yield for investing over t1 years and over t2 years, what rate is implied for the interval between t1 and t2?" This rate is built on the no-arbitrage principle — investing for the longer period must yield the same as investing short then rolling into the forward period.

How to Use It

Enter the two annual spot rates as percentages (for example 5 for 5%), along with their respective maturities in years. The longer maturity t2 must be greater than t1. The calculator returns the annualized forward rate covering the gap between the two dates.

The Formula Explained

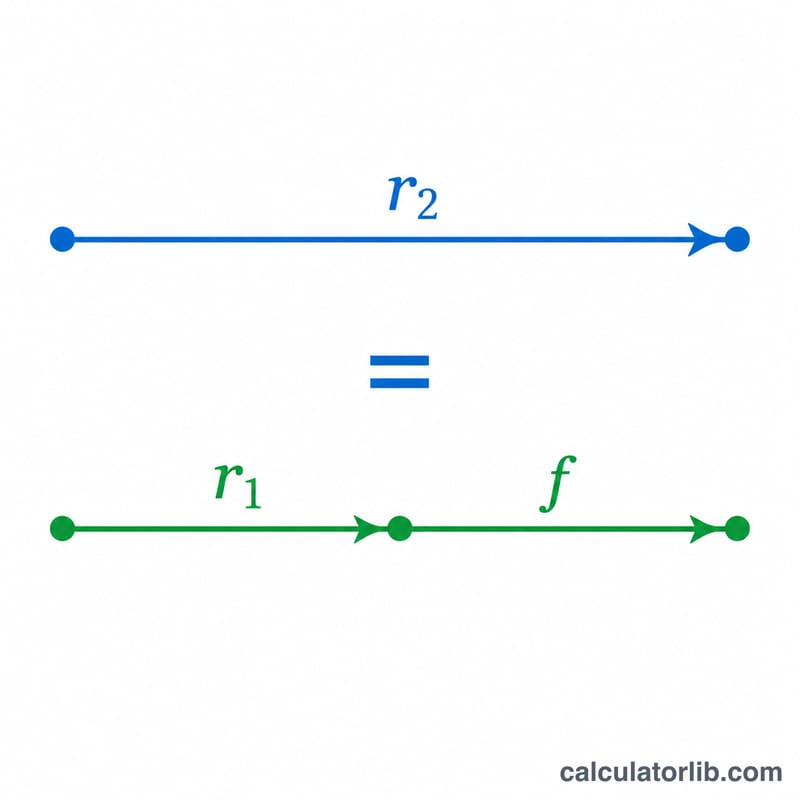

The forward rate f is calculated as:

$$f = \left( \frac{\left(1 + r_2\right)^{t_2}}{\left(1 + r_1\right)^{t_1}} \right)^{\frac{1}{t_2 - t_1}} - 1$$

The numerator grows your money over the full long period, the denominator removes the growth already earned in the short period, and the outer exponent annualizes the leftover growth across the forward window (t2 − t1).

Worked Example

Suppose the 1-year spot rate is 5% and the 2-year spot rate is 6%. Then $$f = \left( \frac{(1.06)^2}{(1.05)^1} \right)^{\frac{1}{1}} - 1 = \left( \frac{1.1236}{1.05} \right) - 1 = 1.070095 - 1 = 0.070095,$$ or about 7.01%. This is the implied 1-year rate, one year from now.

FAQ

Why is the forward rate higher than the spot rates? When the yield curve slopes upward, the forward rate exceeds both spot rates because the later period must "make up" for the lower early returns.

Do the rates need to be compounded annually? This calculator assumes annual compounding. For continuous compounding the formula uses exponentials of rate × time instead.

Can t1 be zero? Yes — if t1 = 0, the forward rate simply equals the t2 spot rate annualized over t2.