什麼是遠期利率計算機?

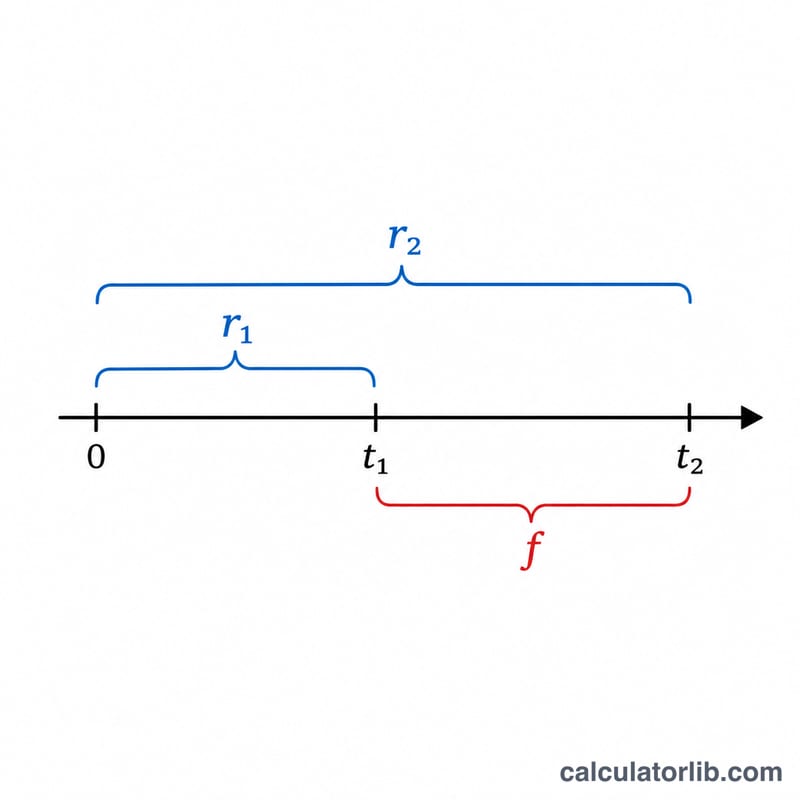

遠期利率(Forward Rate)是指今天就能由市場現有、不同到期期間的即期利率(Spot Rate)所推算出來、針對「未來某一段期間」的隱含利率。它要回答的問題是:「如果我已經知道投資 \(t_1\) 年與投資 \(t_2\) 年的報酬率,那麼介於 \(t_1\) 到 \(t_2\) 之間這段期間,所隱含的利率會是多少?」這個利率建立在「無套利」原則之上——投資較長期間所得到的報酬,必須等於先投資短期、再於遠期期間滾入續投所得到的報酬,否則就會出現套利空間。

如何使用

請以百分比輸入兩個年化即期利率(例如填 5 代表 5%),並分別填入各自以「年」為單位的到期期間。較長的到期期間 \(t_2\) 必須大於 \(t_1\)。計算機會回傳涵蓋這兩個時間點之間缺口的年化遠期利率。

公式解析

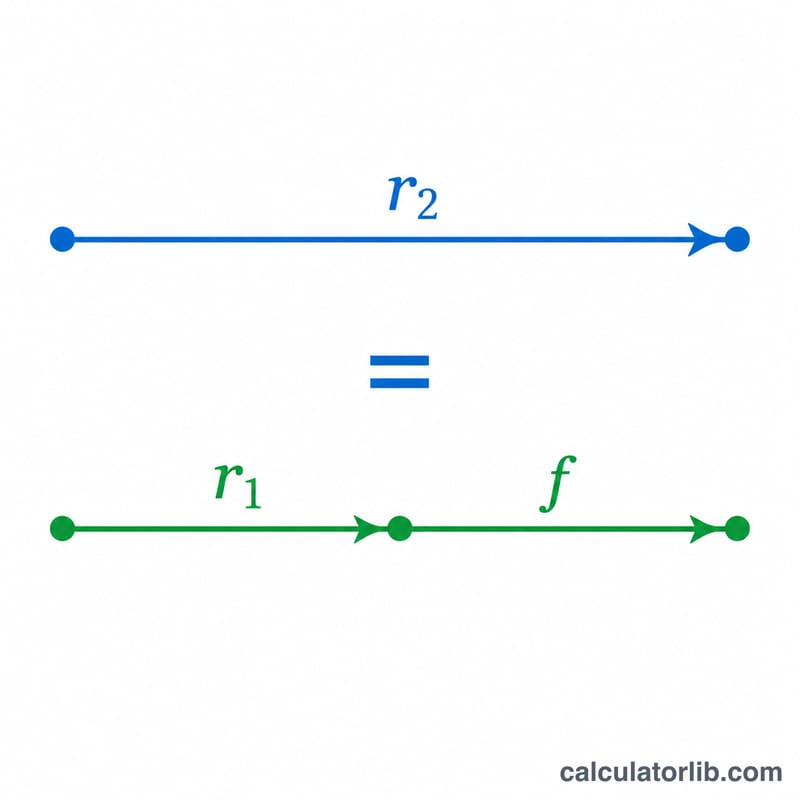

遠期利率 f 的計算方式如下:

$$f = \left( \frac{\left(1 + r_2\right)^{t_2}}{\left(1 + r_1\right)^{t_1}} \right)^{\frac{1}{t_2 - t_1}} - 1$$

分子代表資金在整段較長期間中的成長,分母則扣除短期間內已經賺到的部分,最外層的指數則把剩餘的成長攤平、換算成遠期期間(\(t_2 - t_1\))的年化利率。

實際範例

假設 1 年期即期利率為 5%、2 年期即期利率為 6%,則 $$f = \left( \frac{(1.06)^2}{(1.05)^1} \right)^{\frac{1}{1}} - 1 = \left( \frac{1.1236}{1.05} \right) - 1 = 1.070095 - 1 = 0.070095$$,約等於 7.01%。這就是「從現在起算一年後、為期一年」的隱含遠期利率。

常見問題

為什麼遠期利率會高於兩個即期利率?當殖利率曲線呈現上揚(正斜率)時,遠期利率會高於兩個即期利率,因為較後段的期間必須「補回」前段較低報酬所造成的落差。

利率一定要以年複利計算嗎?本計算機採用年複利假設。若改用連續複利,公式則會改以「利率 \(\times\) 時間」的指數函數來表示。

\(t_1\) 可以等於 0 嗎?可以。當 \(t_1 = 0\) 時,遠期利率就直接等於 \(t_2\) 期即期利率在 \(t_2\) 期間的年化結果。