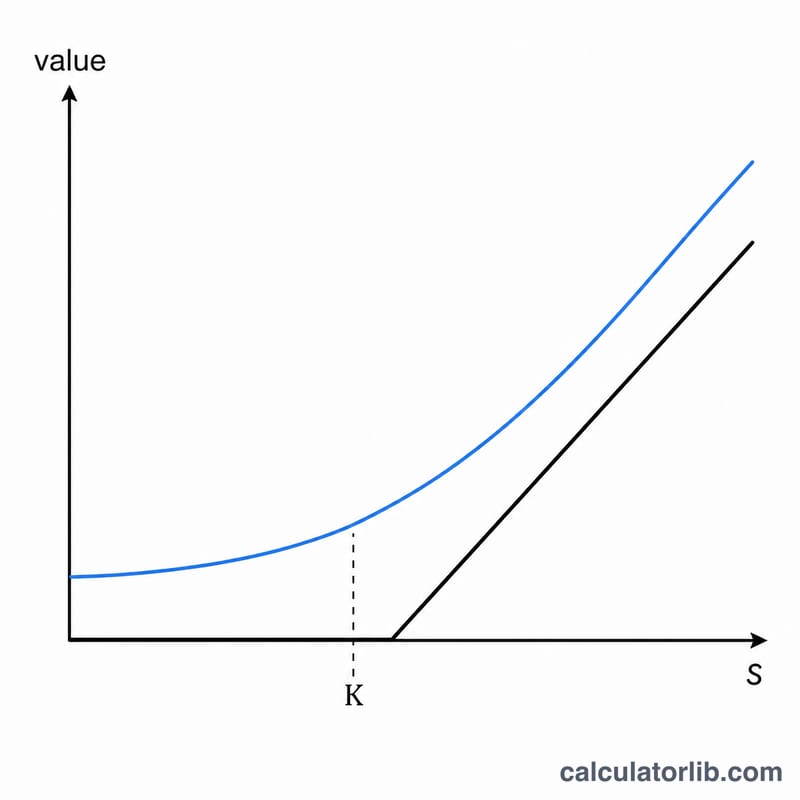

What Is the Black-Scholes Calculator?

The Black-Scholes model is the foundation of modern options pricing. It estimates the theoretical fair value of European-style call and put options — those that can only be exercised at expiry — assuming no dividends. This calculator takes five inputs and instantly returns the call price, put price, and the intermediate factors d1 and d2.

How to Use It

Enter the current spot price (S) of the underlying asset, the option strike price (K), the time to expiry in years (e.g. 0.5 for six months), the annualized risk-free interest rate as a percent, and the annualized volatility as a percent. The calculator converts the percentages to decimals internally and computes both option types at once.

The Formula Explained

The model first computes two standardized quantities:

$$d_1 = \dfrac{\ln(S/K) + \left(r + \sigma^2/2\right)\cdot T}{\sigma\cdot\sqrt{T}}, \quad\text{and}\quad d_2 = d_1 - \sigma\cdot\sqrt{T}.$$

Then the call value is $$C = S\cdot N(d_1) - K\cdot e^{-rT}\cdot N(d_2),$$ where \(N(\cdot)\) is the cumulative standard normal distribution. The put value follows from put-call parity: $$P = K\cdot e^{-rT}\cdot N(-d_2) - S\cdot N(-d_1).$$ Here \(e^{-rT}\) discounts the strike back to present value, and \(N(d_1)\), \(N(d_2)\) represent risk-adjusted probabilities tied to the option finishing in the money.

Worked Example

Suppose \(S = 100\), \(K = 100\), \(T = 1\) year, \(r = 5\%\), and \(\sigma = 20\%\). Then \(\sigma\sqrt{T} = 0.20\), $$d_1 = \frac{0 + (0.05 + 0.02)}{0.20} = 0.35, \quad\text{and}\quad d_2 = 0.15.$$ With \(N(0.35) \approx 0.6368\) and \(N(0.15) \approx 0.5596\), the call price $$\approx 100\cdot 0.6368 - 95.123\cdot 0.5596 \approx 10.45.$$ The put price \(\approx 5.57\).

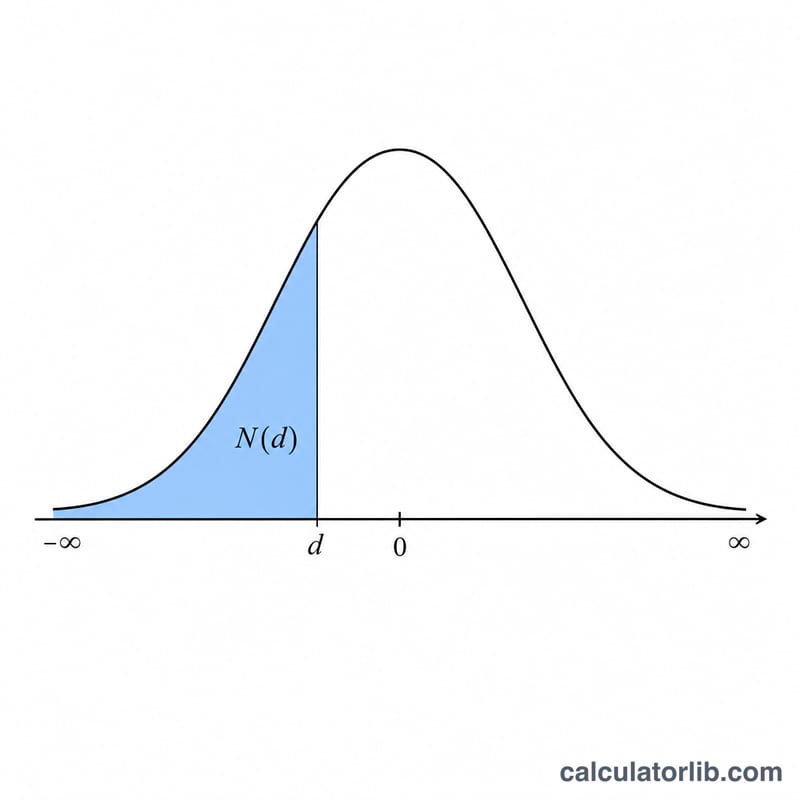

Standard Normal Distribution N(d) Reference Table

The Black-Scholes formula requires \(N(d_1)\) and \(N(d_2)\), the cumulative standard normal distribution function — the probability that a standard normal random variable is less than or equal to \(d\). The table below lists \(N(d)\) for \(d\) from \(-3.0\) to \(3.0\) in steps of \(0.1\).

| d | N(d) | d | N(d) |

|---|---|---|---|

| -3.0 | 0.0013 | 0.1 | 0.5398 |

| -2.9 | 0.0019 | 0.2 | 0.5793 |

| -2.8 | 0.0026 | 0.3 | 0.6179 |

| -2.7 | 0.0035 | 0.4 | 0.6554 |

| -2.6 | 0.0047 | 0.5 | 0.6915 |

| -2.5 | 0.0062 | 0.6 | 0.7257 |

| -2.4 | 0.0082 | 0.7 | 0.7580 |

| -2.3 | 0.0107 | 0.8 | 0.7881 |

| -2.2 | 0.0139 | 0.9 | 0.8159 |

| -2.1 | 0.0179 | 1.0 | 0.8413 |

| -2.0 | 0.0228 | 1.1 | 0.8643 |

| -1.9 | 0.0287 | 1.2 | 0.8849 |

| -1.8 | 0.0359 | 1.3 | 0.9032 |

| -1.7 | 0.0446 | 1.4 | 0.9192 |

| -1.6 | 0.0548 | 1.5 | 0.9332 |

| -1.5 | 0.0668 | 1.6 | 0.9452 |

| -1.4 | 0.0808 | 1.7 | 0.9554 |

| -1.3 | 0.0968 | 1.8 | 0.9641 |

| -1.2 | 0.1151 | 1.9 | 0.9713 |

| -1.1 | 0.1357 | 2.0 | 0.9772 |

| -1.0 | 0.1587 | 2.1 | 0.9821 |

| -0.9 | 0.1841 | 2.2 | 0.9861 |

| -0.8 | 0.2119 | 2.3 | 0.9893 |

| -0.7 | 0.2420 | 2.4 | 0.9918 |

| -0.6 | 0.2743 | 2.5 | 0.9938 |

| -0.5 | 0.3085 | 2.6 | 0.9953 |

| -0.4 | 0.3446 | 2.7 | 0.9965 |

| -0.3 | 0.3821 | 2.8 | 0.9974 |

| -0.2 | 0.4207 | 2.9 | 0.9981 |

| -0.1 | 0.4602 | 3.0 | 0.9987 |

| 0.0 | 0.5000 |

Symmetry note: the standard normal is symmetric about zero, so \(N(-d) = 1 - N(d)\). For example, \(N(-1.0) = 1 - N(1.0) = 1 - 0.8413 = 0.1587\). This lets you read any negative argument from the positive side of the table.

Key Terms & Variables

- Spot price (S)

- The current market price of the underlying asset, in currency units per share (e.g. dollars). The starting point for valuing the option.

- Strike price (K)

- The fixed price at which the option holder may buy (call) or sell (put) the underlying at expiry, in the same currency units as S.

- Time to expiry (T)

- The remaining life of the option, expressed in years (e.g. 6 months = 0.5, 90 days ≈ 0.2466). Black-Scholes prices European options that can only be exercised at expiry.

- Risk-free rate (r)

- The continuously compounded annual interest rate on a riskless investment over the option's life, as a decimal (5% = 0.05). Entered as a percent in the calculator and divided by 100.

- Volatility (σ)

- The annualized standard deviation of the underlying's continuously compounded returns, as a decimal (20% = 0.20). Higher volatility raises both call and put values.

- d1

- A dimensionless intermediate term, \(d_1 = \dfrac{\ln(S/K) + (r + \sigma^2/2)T}{\sigma\sqrt{T}}\). It feeds the \(N(d_1)\) term and equals the call's delta.

- d2

- \(d_2 = d_1 - \sigma\sqrt{T}\), also dimensionless. \(N(d_2)\) is the risk-neutral probability the call expires in the money.

- N(d) — cumulative normal

- The cumulative standard normal distribution function: the probability a standard normal variable is at most \(d\). It returns a value between 0 and 1 (a probability, unitless).

- Discount factor (e-rT)

- The present-value factor that discounts the strike paid at expiry back to today at the continuously compounded risk-free rate. Unitless, between 0 and 1.

How Inputs Affect the Price

The base case below holds four inputs fixed and varies one at a time, so each block isolates a single driver. Base case: spot \(S = 100\), strike \(K = 100\) (at the money), time \(T = 1\) year, risk-free rate \(r = 5\%\), volatility \(\sigma = 20\%\). At these values the call is worth about 10.45 and the put about 5.57.

| Variable changed | Value | Call price | Put price |

|---|---|---|---|

| Volatility σ | 10% | 6.80 | 1.92 |

| 20% (base) | 10.45 | 5.57 | |

| 40% | 18.02 | 13.14 | |

| Time to expiry T | 0.25 yr | 4.61 | 3.37 |

| 1 yr (base) | 10.45 | 5.57 | |

| 2 yr | 16.13 | 6.61 | |

| Moneyness (spot S) | 90 (OTM call) | 5.09 | 10.21 |

| 100 (ATM, base) | 10.45 | 5.57 | |

| 110 (ITM call) | 17.66 | 2.78 |

Patterns to note: higher volatility raises both calls and puts, since greater dispersion increases the value of the optional upside while the downside is floored at zero. Longer time generally raises the call (more chance to finish in the money plus a larger discount on the strike); the put rises with time too here, though its time sensitivity is weaker because discounting the strike works against it. Raising the spot increases the call and decreases the put. All figures use the same model and rounding; small differences from a live calculation can arise from intermediate rounding.

FAQ

Does this handle dividends? No — this is the basic non-dividend model. For dividend-paying stocks, reduce the spot by the present value of dividends or use the Black-Scholes-Merton extension.

European or American options? Black-Scholes prices European options. American options (early exercise allowed) require binomial or other numerical methods, though American calls on non-dividend stocks equal European calls.

Why are my inputs in percent? Rate and volatility are entered as percentages for convenience (e.g. 20 for 20%) and the calculator divides them by 100 automatically.