What this calculator does

This tool computes the simple final yield (simple yield to maturity) of a coupon bond held until redemption, and produces a table of yields across a range of purchase prices. It uses the simple-yield, non-compounding convention widely used in Japan for quoting bond yields ("saishu rimawari", final yield), rather than the internal-rate-of-return (IRR) discounting method. The face/redemption value is fixed at 100, the standard quoting base, and all prices are expressed per 100 of face value.

How to use it

Enter the bond's coupon rate (surface rate) as a percent of face, the number of years remaining until maturity, the rounding mode for the displayed yield, and the price step and half-width that define the table range. The table is centred on par (price = 100) and runs from 100 - width to 100 + width in increments of the chosen step. Each row shows the resulting final yield, rounded to three decimal places.

The formula explained

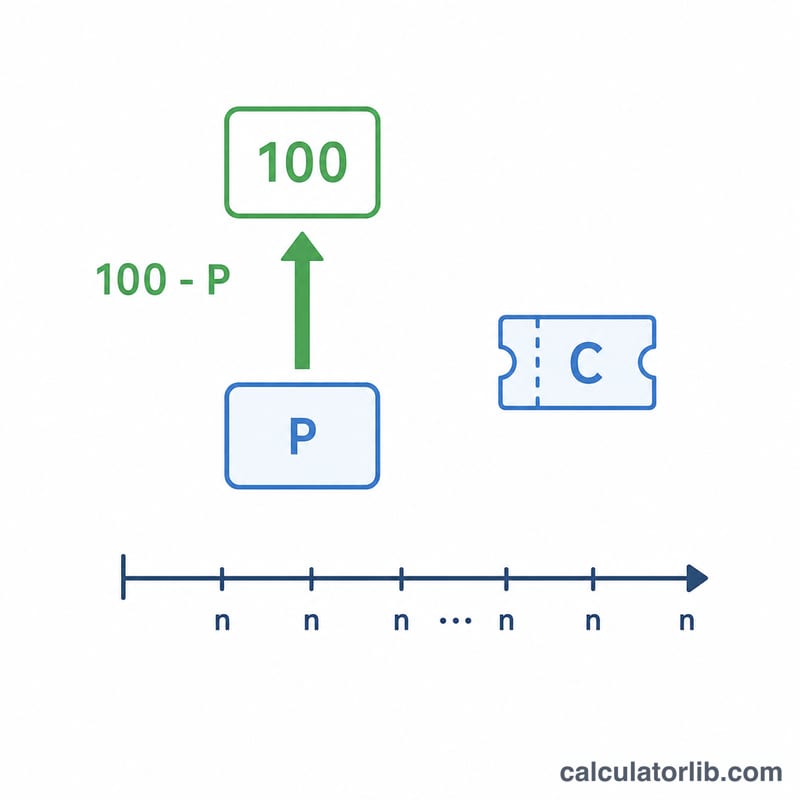

For face value \(F = 100\), annual coupon \(C\) (in yen per 100 face, numerically equal to the coupon percent), purchase price \(P\) and years to maturity \(n\), the simple final yield is: $$\text{Yield} = \frac{C + \dfrac{100 - P}{n}}{P} \times 100$$ The term \(\dfrac{100 - P}{n}\) is the linear (straight-line) annualized capital gain or loss between the purchase price and redemption at 100. Dividing by \(P\) expresses the total annual return as a percent of the price actually invested.

Worked example

With coupon rate 2%, 5 years to maturity and truncation rounding: at a price of 90 the yield is $$\frac{2 + \dfrac{100 - 90}{5}}{90} \times 100 = \frac{4}{90} \times 100 = 4.444\%.$$ At par (100) the yield equals the coupon, 2.000%. At 110 it is $$\frac{2 + \dfrac{100 - 110}{5}}{110} \times 100 = 0.000\%.$$ Below par the yield exceeds the coupon; above par it is lower.

Key Terms Defined

- Coupon (surface) rate

- The fixed annual interest the bond pays, expressed as a percentage of face value. On a face of 100 a 2% coupon pays 2 per year. In Japan this is the hyomen rimawari or surface rate.

- Face / redemption value (100)

- The amount repaid at maturity. By convention this calculator normalizes face value to 100, so prices, coupons and yields are all stated per 100 of redemption value.

- Purchase price \(P\)

- The clean price actually paid per 100 of face value. Below 100 is a discount, above 100 is a premium.

- Years to maturity

- The remaining time, in years, from purchase until the bond is redeemed at face value. The capital gain or loss \((100 - P)\) is spread evenly over these years in the simple-yield convention.

- Simple final yield (saishu rimawari)

- The Japanese quoting convention that adds the annual coupon to the straight-line amortized price difference, then divides by the purchase price. It does not compound and is not an internal rate of return.

- Par

- A price equal to face value (100). At par the simple yield equals the coupon rate.

- Discount

- A price below face value (\(P < 100\)). The investor gains \((100 - P)\) at redemption, raising the yield above the coupon.

- Premium

- A price above face value (\(P > 100\)). The investor loses \((P - 100)\) at redemption, lowering the yield below the coupon.

- IRR-based YTM

- The true yield to maturity: the single discount rate that sets the present value of all future coupons and the redemption value equal to the purchase price. It compounds and generally differs slightly from the simple final yield.

Interpreting Your Result

Compare the computed simple final yield with the coupon rate:

- Yield > coupon: you bought at a discount (\(P < 100\)). The expected redemption gain of \((100 - P)\) adds to the coupon income, so the total return per 100 invested exceeds the surface rate.

- Yield < coupon: you bought at a premium (\(P > 100\)). The redemption loss of \((P - 100)\) is subtracted from coupon income, pulling the yield below the surface rate.

- Yield = coupon: you bought at par (\(P = 100\)), where the \((100 - P)\) term is zero and yield equals the coupon rate exactly.

Keep in mind that the simple final yield is a quoting convention. It amortizes the price difference on a straight-line basis and divides by the purchase price rather than solving for a compounding internal rate of return. As a result it will differ slightly from the IRR-based yield to maturity — typically by a small amount that grows with longer maturities and larger discounts or premiums. For an apples-to-apples figure, run the same inputs through a true YTM calculator and compare.

This calculator describes a pricing convention and is general information only; it is not investment advice. Actual returns depend on reinvestment, taxes, fees, accrued interest, credit risk and whether the bond is held to maturity.

FAQ

Is this the same as the true YTM? No. The true IRR-based YTM discounts each cash flow and gives slightly different figures. This calculator intentionally uses the simpler straight-line "final yield" convention.

Why is face value 100? It is the standard quoting base for bonds, so prices and yields are comparable per 100 of face value.

What if years to maturity is zero? The formula divides by \(n\), so \(n\) must be greater than zero; otherwise the yield is undefined and an error is shown.