What Is a Bond Price Calculator?

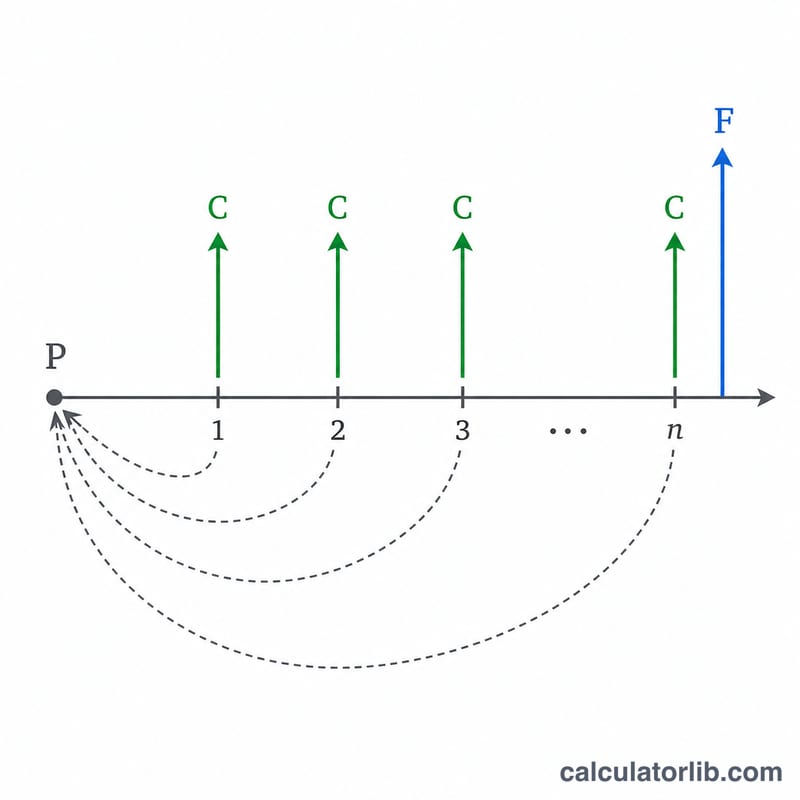

A bond price calculator estimates the fair market value of a fixed-coupon bond by discounting all of its future cash flows back to today. A bond pays periodic interest (coupons) and returns the face value at maturity. Because money received in the future is worth less than money today, each payment is discounted at the required market yield. The sum of those present values is the price an investor should pay.

How to Use It

Enter the bond's face value (par, typically 1,000), the annual coupon rate, the required yield or current market rate, the number of years until maturity, and how many coupon payments are made each year. Click calculate to see the present value, the periodic coupon, the number of periods and whether the bond trades at a premium or discount to par.

The Formula Explained

The price is split into two parts. The coupon stream is an annuity: \(C \cdot (1 - (1+r)^{-n}) / r\), where C is the coupon per period, r is the periodic yield and n is the total number of periods. The repayment of principal is a single lump sum discounted as \(F \cdot (1+r)^{-n}\). Annual values are converted to periodic ones: \(r = \text{yield} \div m\), \(C = \text{face} \times \text{coupon} \div m\), and \(n = \text{years} \times m\), where m is payments per year.

$$P = C \cdot \frac{1 - (1+r)^{-n}}{r} + F \cdot (1+r)^{-n}$$

Worked Example

A 1,000 bond pays a 5% annual coupon semi-annually, matures in 10 years, and the market yield is 6%. Then \(C = 1000 \times 0.05 / 2 = 25\), \(r = 0.06 / 2 = 0.03\), and \(n = 20\). Price:

$$P = 25 \times \frac{1 - 1.03^{-20}}{0.03} + 1000 \times 1.03^{-20} \approx 371.93 + 553.68 \approx 925.61$$Because the yield exceeds the coupon, the bond trades at a discount.

Bond Price Across Yield Scenarios

The table below holds a single bond fixed — \(F = \$1{,}000\) face value, a 5% annual coupon paid semiannually (\(m = 2\)), and 10 years to maturity (\(n = 20\) periods) — while varying only the market (required) yield. Each price is computed with

$$P = C \cdot \frac{1 - (1+r)^{-n}}{r} + F \cdot (1+r)^{-n}$$where the periodic coupon is \(C = \$1{,}000 \times 0.05 / 2 = \$25\) and the periodic yield is \(r = \text{(market rate)}/2\). As yield falls below the coupon the bond trades at a premium; as yield rises above the coupon it trades at a discount; when yield equals the coupon it prices exactly at par.

| Market yield | Periodic yield \(r\) | Bond price \(P\) | Status |

|---|---|---|---|

| 3% | 1.50% | $1,171.69 | Premium |

| 4% | 2.00% | $1,081.76 | Premium |

| 5% | 2.50% | $1,000.00 | Par |

| 6% | 3.00% | $925.61 | Discount |

| 7% | 3.50% | $857.88 | Discount |

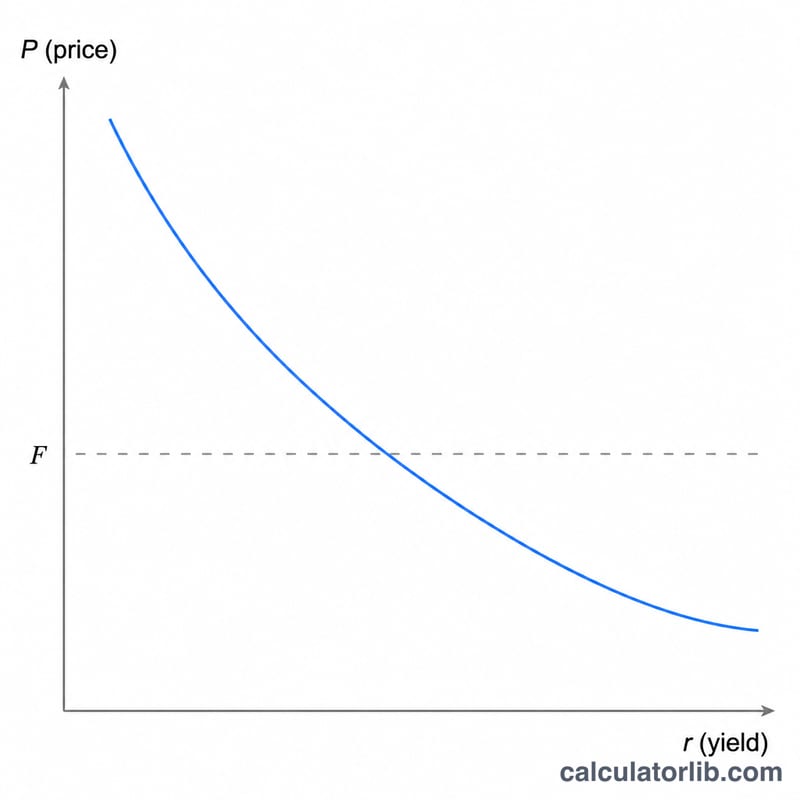

Notice the inverse relationship: higher required yields push the price down, lower yields push it up. The price moves more for a given yield change the longer the maturity and the lower the coupon.

Key Bond Terms Defined

- Face value (par value), \(F\)

- The principal amount repaid to the holder at maturity, commonly $1,000. It also forms the base on which coupon interest is calculated.

- Coupon rate

- The annual interest rate stated on the bond, applied to face value to determine the total yearly coupon income. It is fixed for a conventional bond and does not change with market conditions.

- Coupon payment, \(C\)

- The cash paid each period: \(C = (F \times \text{coupon rate}) / m\). A $1,000 bond with a 5% coupon paid semiannually pays \(C = \$25\) every six months.

- Market (required) yield

- The annual return investors currently demand for bonds of comparable risk and maturity. It is the discount rate applied to the bond's cash flows and drives the price.

- Periodic yield, \(r\)

- The market yield expressed per payment period: \(r = \text{(market rate)} / m\). With a 6% annual yield paid semiannually, \(r = 0.03\).

- Number of periods, \(n\)

- The total count of coupon periods until maturity: \(n = \text{years} \times m\). A 10-year semiannual bond has \(n = 20\).

- Payment frequency, \(m\)

- How many coupon payments occur per year — 1 (annual), 2 (semiannual), 4 (quarterly), or 12 (monthly).

- Premium

- A price above face value, occurring when the coupon rate exceeds the market yield.

- Discount

- A price below face value, occurring when the market yield exceeds the coupon rate.

- Clean price

- The bond price excluding any interest accrued since the last coupon — this is what the present-value formula produces.

- Dirty price

- The clean price plus accrued interest — the actual cash amount a buyer pays between coupon dates.

Interpreting Your Bond Price

The number this calculator returns is the present value of all future coupons plus the repayment of face value, discounted at the market yield. How it compares to par tells you the bond's pricing regime:

- Price above par (premium): the bond's fixed coupon rate is higher than the yield investors currently require, so its above-market income stream is worth a premium.

- Price below par (discount): the coupon rate is lower than the required yield, so the price falls until the total return matches the market.

- Price equal to par: the coupon rate and the market yield are equal, so each coupon exactly compensates for the time value of money.

This relationship is the core of bond pricing: coupon > yield → premium; coupon < yield → discount; coupon = yield → par. Price and yield always move in opposite directions.

The result is a clean, theoretical price — it assumes valuation on a coupon date and excludes accrued interest. Between coupon payments the actual settlement (dirty) price adds the interest earned so far, which you can estimate separately with an accrued-interest calculation.

Comparing price to par is also the mirror image of yield-to-maturity (YTM): the discount rate that makes the present value of the cash flows equal the market price is the YTM. A bond priced at a premium has a YTM below its coupon rate, a bond at a discount has a YTM above its coupon rate, and a bond at par has a YTM equal to its coupon rate. If you know the market price and want to solve for the implied return instead, use a yield-to-maturity calculation.

This is general educational information about bond mathematics, not investment advice. Actual market prices depend on credit risk, liquidity, taxes, day-count conventions and other factors not captured by a single discounting formula.

FAQ

Why does price fall when yields rise? Higher discount rates shrink the present value of fixed future cash flows, so the bond is worth less.

What does premium or discount mean? If the price is above face value the bond trades at a premium (coupon > yield); below face value it trades at a discount (coupon < yield).

Does this account for accrued interest? No — this gives the clean theoretical price on a coupon date. Add accrued interest for the dirty price between coupon dates.