What Is Yield to Maturity?

Yield to maturity (YTM) is the total annualized return an investor earns if a bond is held until it matures, assuming all coupon payments are received on schedule. The exact YTM is the discount rate that sets the present value of all future cash flows equal to the bond's current market price, which requires iterative solving. This calculator uses the well-known approximation formula to give you a fast, close estimate without iteration.

How to Use This Calculator

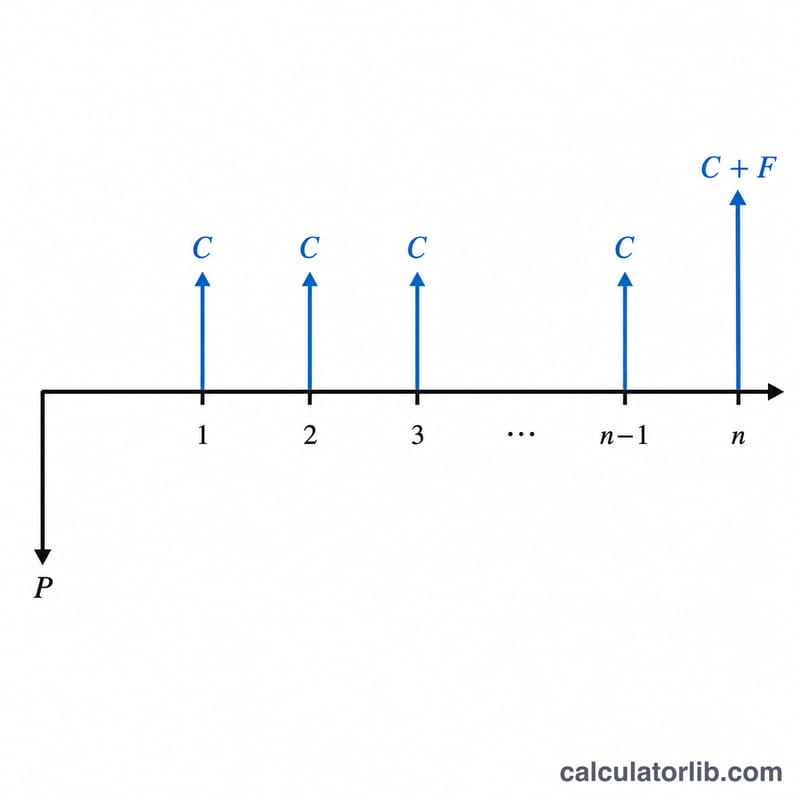

Enter four values: the bond's annual coupon rate (as a percentage), its face (par) value, the current market price you paid or would pay, and the number of years remaining until maturity. The tool computes the annual coupon payment and then plugs everything into the approximation formula to return an estimated YTM as a percentage.

The Formula Explained

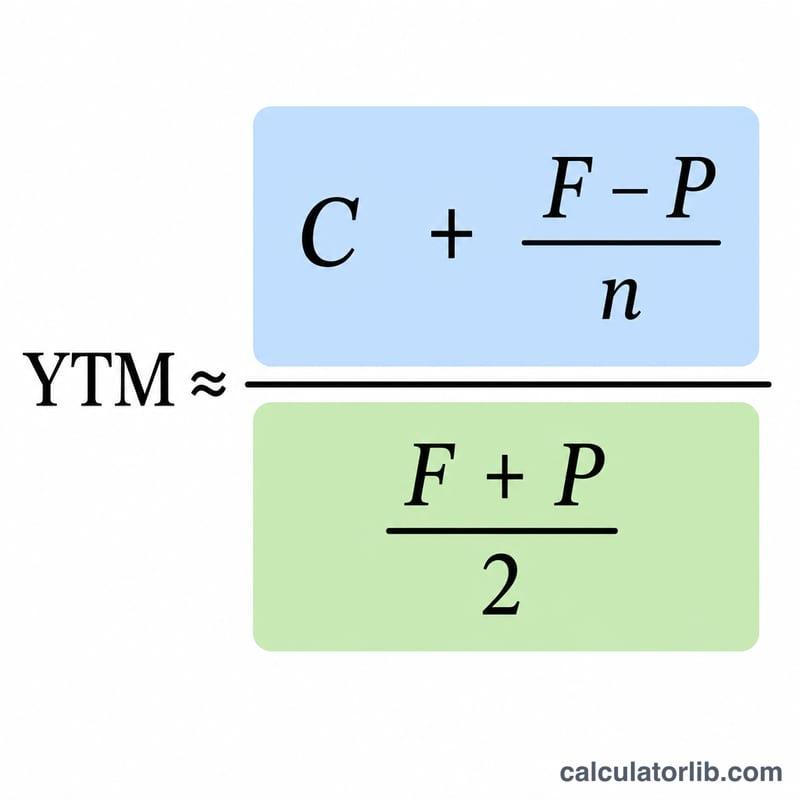

The approximate YTM is calculated as:

$$\text{YTM} \approx \frac{C + \dfrac{F - P}{n}}{\dfrac{F + P}{2}}$$

Here C is the annual coupon payment (face value \(\times\) coupon rate), F is face value, P is current price, and n is years to maturity. The numerator adds the coupon income to the annualized capital gain or loss. The denominator is the average of face value and price, used as a proxy for the average invested capital.

Worked Example

Suppose a bond has a face value of $1,000, an 8% annual coupon ($80 per year), a current price of $950, and 10 years to maturity. The numerator is \(80 + (1000 - 950)/10 = 80 + 5 = 85\). The denominator is \((1000 + 950)/2 = 975\). So $$\text{YTM} \approx 85 / 975 = 0.08718,$$ or about 8.72%.

FAQ

Is this the exact YTM? No — it is an approximation. It is typically within a few basis points of the true YTM and is widely taught as a quick estimate.

Why is YTM higher than the coupon rate when the bond trades at a discount? Because you also gain the difference between the higher face value you receive at maturity and the lower price you paid, which boosts your total return.

What if the bond trades at a premium? If price exceeds face value, the \((F - P)\) term is negative, lowering the YTM below the coupon rate.