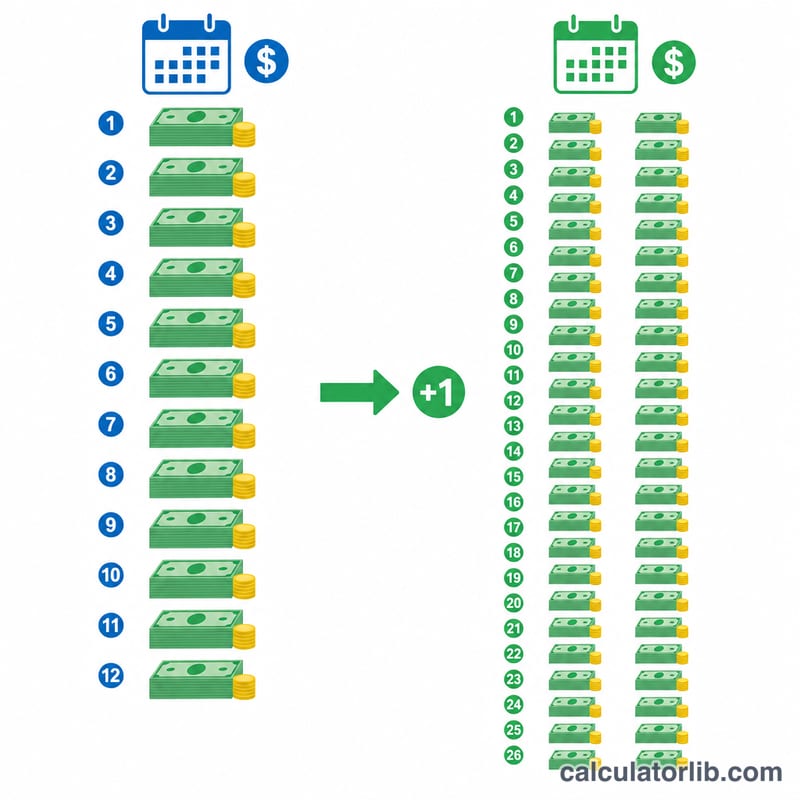

What Is a Biweekly Mortgage Payment?

A biweekly mortgage plan splits your normal monthly payment in half and pays that amount every two weeks. Because there are 52 weeks in a year, you make 26 half-payments — the equivalent of 13 full monthly payments instead of 12. That one extra payment per year goes straight to principal, shortening your loan and cutting total interest.

How to Use This Calculator

Enter your loan amount, annual interest rate, and term in years. The calculator computes your standard monthly payment, then halves it to find the biweekly amount. It also simulates the biweekly payoff to estimate how many years sooner you'll be mortgage-free and how much interest you save.

The Formula Explained

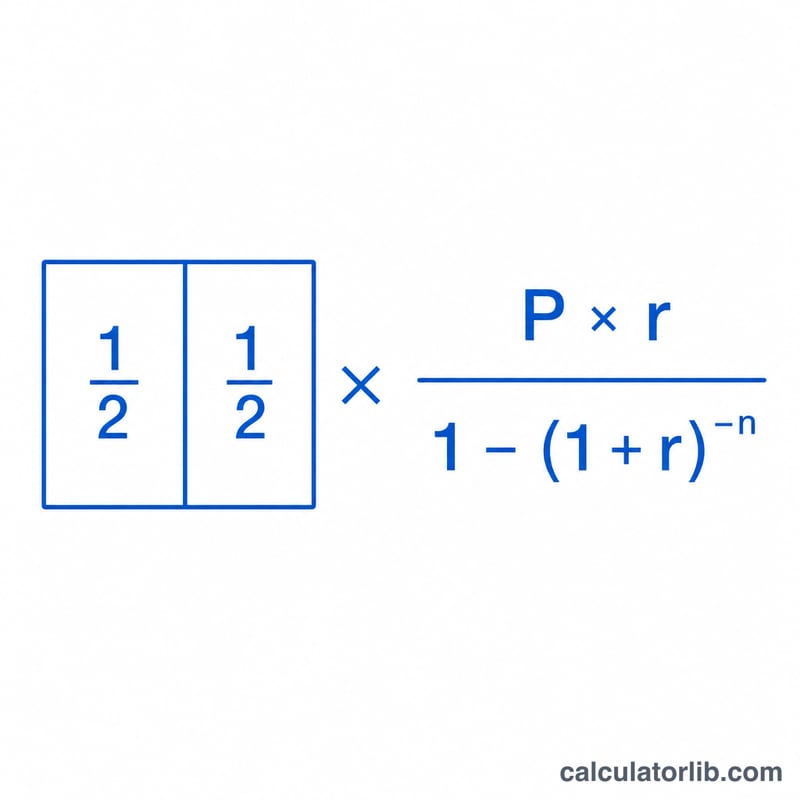

The monthly payment uses the standard amortization formula $$M = \frac{P\cdot r}{1-(1+r)^{-n}}$$ where \(P\) is the principal, \(r\) is the monthly interest rate (annual rate \(\div\) 12), and \(n\) is the total number of monthly payments (years \(\times\) 12). The biweekly payment is simply $$B = \frac{M}{2}$$

Worked Example

For a $300,000 loan at 6.5% over 30 years: \(r = 0.065/12 \approx 0.0054167\) and \(n = 360\). The monthly payment is about $1,896.20, so the biweekly payment is about $948.10. By paying that every two weeks, the loan is paid off years earlier and total interest drops substantially.

Biweekly vs. Monthly: Savings Across Loan Scenarios

The table below compares a standard monthly mortgage with a true biweekly plan (half the monthly payment paid every two weeks, which equals 26 half-payments — the equivalent of 13 monthly payments — per year). The extra payment each year goes straight to principal, cutting both total interest and the payoff time. Figures are principal-and-interest only and are rounded.

| Loan / Rate / Term | Monthly P&I | Biweekly payment | Total interest (monthly) | Total interest (biweekly) | Interest saved | Time shaved |

|---|---|---|---|---|---|---|

| $200,000 · 6% · 30 yr | $1,199.10 | $599.55 | $231,676 | $182,700 | ~$49,000 | ~5 yr |

| $300,000 · 6.5% · 30 yr | $1,896.20 | $948.10 | $382,633 | $297,800 | ~$84,800 | ~5.5 yr |

| $400,000 · 7% · 30 yr | $2,661.21 | $1,330.61 | $558,036 | $425,900 | ~$132,100 | ~6 yr |

| $250,000 · 6% · 15 yr | $2,109.64 | $1,054.82 | $129,735 | $114,200 | ~$15,500 | ~1.3 yr |

The biweekly payment is always exactly half the monthly payment; the savings come from making 26 of those half-payments (13 full payments) per year instead of 12. Note that higher rates and longer terms produce the largest dollar savings.

Key Mortgage Terms Defined

- Principal (P)

- The amount you borrow — the loan balance on which interest is charged. In the formula it is the starting figure that gets paid down over time.

- Annual interest rate

- The stated yearly rate on the loan (e.g. 6%). It is the quoted nominal rate before it is broken into per-period charges.

- Periodic (monthly) rate (r)

- The annual rate divided by the number of compounding periods per year. For a monthly mortgage, \(r = \frac{\text{annual rate}}{100 \times 12}\). A 6% loan has a monthly rate of \(0.06/12 = 0.005\).

- Term

- The length of the loan, usually expressed in years (commonly 15 or 30). It sets how long the schedule runs if you make only the scheduled payments.

- Number of periods (n)

- The total count of scheduled payments, equal to the term in years times the periods per year. A 30-year monthly loan has \(n = 30 \times 12 = 360\).

- Amortization

- The process of paying off a loan through regular payments, where each payment covers the period's interest first and applies the remainder to principal. Early payments are mostly interest; later ones are mostly principal.

- Escrow

- An account your lender may use to collect and hold money for property taxes and homeowners insurance, paid alongside principal and interest. Escrow is not part of the P&I figures this calculator produces.

- Biweekly vs. bimonthly

- Biweekly means every two weeks — 26 payments a year, which equals 13 monthly payments and creates the extra annual principal payment. Bimonthly means twice a month — 24 payments a year, totaling exactly 12 monthly payments with no extra payment and no acceleration.

Understanding Your Biweekly Results

The interest savings and shortened term shown here come from a single mechanism: paying half your monthly amount every two weeks produces 26 half-payments per year, which is the equivalent of 13 full monthly payments instead of 12. That one extra payment each year is applied directly to principal, so the balance falls faster and less interest accrues over the life of the loan.

These results assume each biweekly payment is credited to your loan the moment it is received. Some lenders instead hold biweekly payments and disburse them monthly, or only post the extra payment once or twice a year — which reduces or eliminates the modeled savings. Confirm how your servicer applies payments before relying on the projection.

The figures cover principal and interest only. Property taxes, homeowners insurance, HOA dues, and mortgage insurance are excluded, even though your lender may collect them through escrow. Some banks also charge setup or per-payment fees to enroll in a formal biweekly program; over time those fees can offset part of the interest you save.

If your goal is simply to pay down principal faster, you can usually achieve the same effect for free by dividing your monthly payment by 12 and adding that amount as extra principal each month, or by making one additional full payment per year — no special program required. This is general educational information, not personalized financial advice; consult your loan servicer or a financial professional about your specific mortgage.

FAQ

Does my lender have to allow biweekly payments? Many lenders offer biweekly programs, but you can often replicate the savings by adding 1/12 of your payment to each monthly payment.

Why 26 payments and not 24? Two payments per month would equal exactly 12 monthly payments. Paying every two weeks gives 26 half-payments — the equivalent of 13 monthly payments.

Are taxes and insurance included? No. This calculator covers principal and interest only; escrow for taxes and insurance is separate.