What the Lease Fixed Rate Calculator Does

This calculator estimates the monthly payment on a fixed-rate finance lease — the type used for vehicles and equipment. Unlike a straight loan, a lease only finances the portion of the asset's value that you actually "use up" during the term, because the asset still has a residual (resale) value at the end. You enter five things and the tool returns your monthly payment, total interest, and total cost.

The Inputs You Enter

- Asset Value – the cash price of the vehicle or equipment.

- Residual Value – its estimated worth at the end of the lease (the part you are not paying off).

- Lease Term (months) – the length of the lease, e.g. 36 months.

- Annual Interest Rate (%) – the fixed yearly rate, converted internally to a monthly rate.

- Down Payment – any upfront amount, subtracted from the asset value before financing.

- Payment Timing – choose End of Period (Ordinary) or Beginning of Period (Advance).

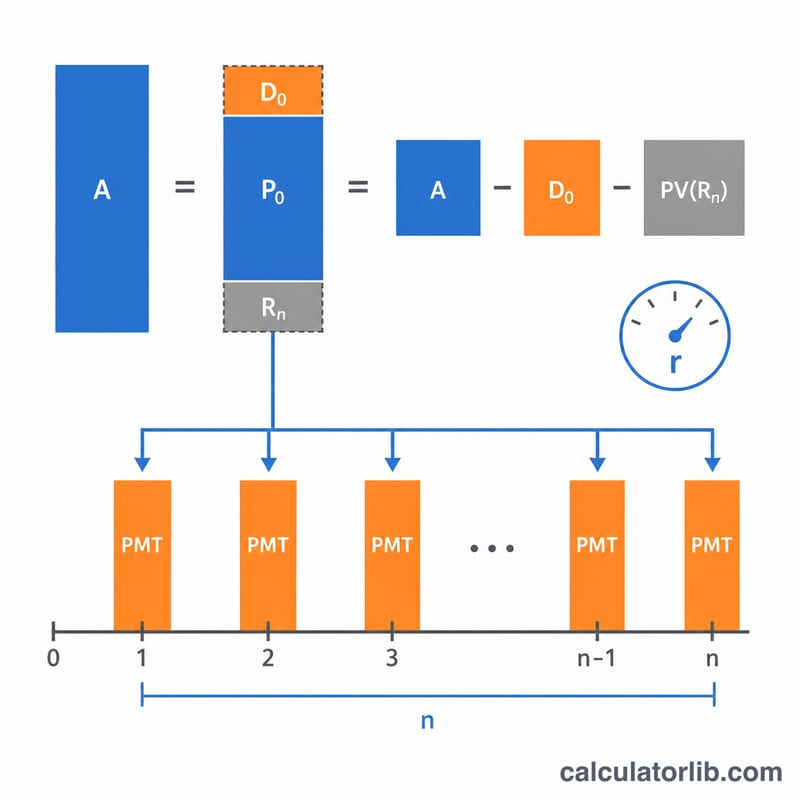

The Formula Explained

First, the monthly rate is \(r = \text{annual rate} / 100 / 12\). The financed amount is the asset value minus the down payment. The calculator then discounts the residual to its present value: \(\text{PV residual} = \text{residual} / (1 + r)^n\), and subtracts it to get the amount actually amortized through payments.

The payment uses the standard annuity (PMT) formula:

$$\text{PMT} = \frac{\text{amortized} \times r \times (1+r)^{n}}{(1+r)^{n} - 1}$$

If you select beginning-of-period payments, the result is divided by \((1 + r)\) to reflect paying in advance (annuity due). When the rate is 0%, the payment is simply the amortized amount divided by the term.

Worked Example

Asset $50,000, residual $10,000, 36 months, 6.5% annual, no down payment, end-of-period. Monthly rate = \(0.0054167\). PV of residual ≈ $8,231, so the amortized amount ≈ $41,769. Plugging into the PMT formula gives roughly $1,280 per month. Over 36 payments that totals about $46,082, meaning roughly $4,313 in interest on top of the depreciation financed.

FAQ

Why does a higher residual lower my payment? Because you only finance the difference between the asset value and the residual. A higher residual means less to amortize, so payments drop.

What does choosing "Beginning of Period" change? Paying in advance reduces each payment slightly, since the lender holds your money for less time — the result is divided by \((1 + r)\).

Is this an exact quote? No. It is an estimate ignoring taxes, fees, and acquisition charges. Use it to compare scenarios, then confirm exact figures with your lessor.