What Is a Loan Amortization Schedule?

An amortization schedule is the plan that shows how a fixed-rate loan is paid off over time. Every payment is the same amount, but the split between interest and principal changes each month. Early on, most of your payment goes toward interest; as the balance shrinks, more of each payment goes toward principal. This calculator computes your fixed monthly payment and summarizes the total interest you will pay over the life of the loan.

How to Use It

Enter three values: the loan amount (principal), the annual interest rate as a percentage, and the loan term in years. The calculator converts the annual rate to a monthly rate and the term to a number of months, then returns your monthly payment, the total amount repaid, and the total interest.

The Formula Explained

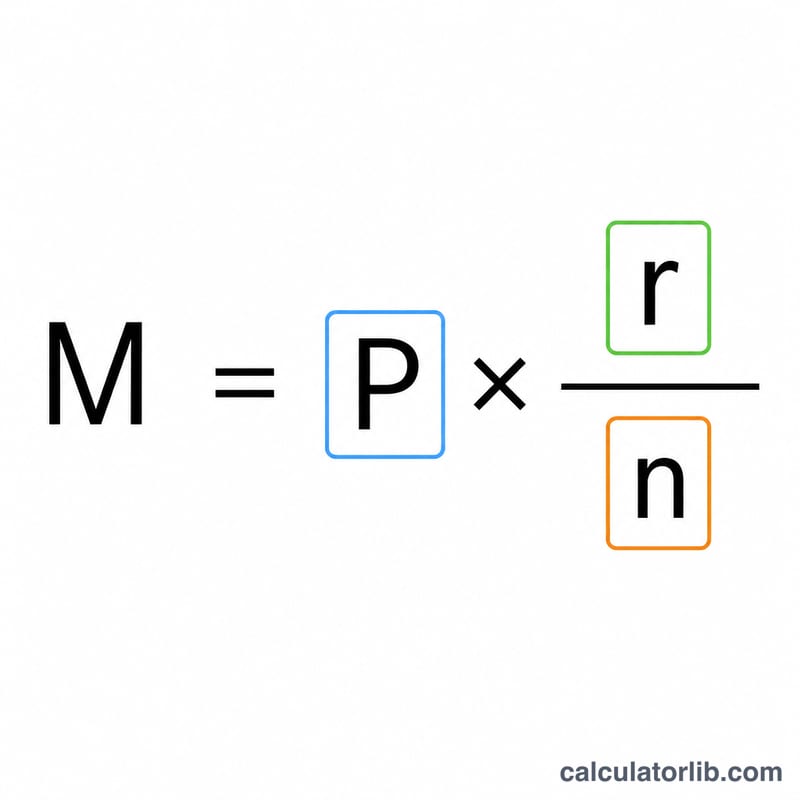

The standard amortizing-loan payment formula is

$$M = P \cdot \frac{r}{1 - (1 + r)^{-n}}$$where \(P\) is the principal, \(r\) is the monthly interest rate (annual rate divided by 12 and by 100), and \(n\) is the total number of payments. For each period, interest equals the current balance times \(r\), and the principal portion is the payment minus that interest:

$$\text{interest} = \text{balance} \cdot r, \quad \text{principal} = M - \text{interest}$$The balance falls by the principal portion until it reaches zero on the final payment. If the rate is 0%, the payment is simply \(P\) divided by \(n\).

Worked Example

Suppose you borrow $200,000 at 6% annual interest for 30 years. The monthly rate is \(0.06 / 12 = 0.005\) and \(n = 360\). The payment is

$$200{,}000 \times \frac{0.005}{1 - 1.005^{-360}} \approx \$1{,}199.10$$Over 360 months you repay about $431,676, of which roughly $231,676 is interest.

Monthly Payment Across Loan Scenarios

The table below shows how the monthly payment, total amount repaid, and total interest change when you vary the loan amount, the annual interest rate, and the term. All figures assume a fixed-rate, fully amortizing loan using the formula \(M = P \cdot \frac{r(1+r)^{n}}{(1+r)^{n}-1}\), where \(r\) is the monthly rate and \(n\) is the number of monthly payments.

| Loan Amount | Annual Rate | Term | Monthly Payment | Total Repaid | Total Interest |

|---|---|---|---|---|---|

| $200,000 | 4% | 15 years | $1,479.38 | $266,288 | $66,288 |

| $200,000 | 4% | 30 years | $954.83 | $343,739 | $143,739 |

| $200,000 | 6% | 15 years | $1,687.71 | $303,788 | $103,788 |

| $200,000 | 6% | 30 years | $1,199.10 | $431,677 | $231,677 |

| $200,000 | 8% | 15 years | $1,911.30 | $344,034 | $144,034 |

| $200,000 | 8% | 30 years | $1,467.53 | $528,310 | $328,310 |

Two patterns are visible at a glance: raising the rate increases every column, and doubling the term from 15 to 30 years lowers the monthly payment substantially but roughly doubles (or more) the total interest paid over the life of the loan.

Key Terms & Variables

- Principal (P)

- The original amount borrowed — the loan balance at the start before any payments are made. In the form this is the Loan Amount.

- Annual interest rate

- The stated yearly rate on the loan, entered as a percent (e.g. 6 for 6%). It is the Annual Rate (%) field.

- Monthly interest rate (r)

- The annual rate converted to a per-month decimal: \(r = \frac{\text{annual rate \%}}{1200}\). For a 6% loan, \(r = 6/1200 = 0.005\).

- Term & number of payments (n)

- The term is the loan length in years; the number of payments is \(n = 12 \times \text{years}\). A 30-year loan has \(n = 360\) monthly payments.

- Amortization

- The process of paying off a loan through equal periodic payments, where each payment covers the interest accrued that period plus a portion of principal, gradually reducing the balance to zero by the final payment.

- Monthly payment (M)

- The fixed amount paid each month, computed from \(P\), \(r\), and \(n\). It stays constant for a fixed-rate loan even though the interest/principal split shifts over time.

- Total interest

- The sum of all interest paid over the life of the loan: \(\text{Total Interest} = (M \times n) - P\) — the difference between everything you repay and the amount you originally borrowed.

Interpreting Your Amortization Results

Total interest vs. principal ratio. Dividing total interest by the principal tells you how much extra you pay per dollar borrowed. A ratio near 0.3 means you pay about 30 cents of interest for every dollar borrowed; a ratio above 1.0 means you pay more in interest than you borrowed in the first place. High ratios come from high rates, long terms, or both.

Front-loaded interest. Because interest each month is charged on the remaining balance, early payments are mostly interest and only a small slice goes to principal. As the balance falls, the interest portion shrinks and the principal portion grows, so later payments retire the balance much faster. This is why paying extra early in a loan saves disproportionately more interest than paying extra near the end.

Total repaid relative to amount borrowed. Total repaid equals the monthly payment multiplied by the number of payments \((M \times n)\). Comparing it to the principal shows the true lifetime cost of the loan. For example, a $200,000 loan at 6% over 30 years repays about $431,677 in total — more than twice the amount borrowed.

Longer terms: lower payment, higher total interest. Extending the term spreads the principal over more payments, which lowers each monthly payment but also means the balance accrues interest for longer. As a factual rule, for the same loan amount and rate a longer term always reduces the monthly payment and increases the total interest paid. Choosing a term is therefore a trade-off between monthly affordability and lifetime cost.

This is general educational information, not financial advice. Confirm exact figures and terms with your lender before making borrowing decisions.

FAQ

Why is so much of my early payment interest? Interest is calculated on the outstanding balance, which is largest at the start, so the interest portion is highest early and declines over time.

Does extra payment shorten the loan? Yes. Any amount above the scheduled payment reduces principal directly, lowering future interest and shortening the term.

What if my rate is 0%? With no interest, each payment is just the principal divided by the number of months, and total interest is zero.