What Is a Debt-to-Income (DTI) Ratio?

Your debt-to-income ratio compares how much you owe each month to how much you earn before taxes. Expressed as a percentage, it is one of the key metrics lenders use to decide whether you can comfortably take on a new loan or mortgage. A lower DTI signals that you have plenty of income left after covering your obligations, while a higher DTI suggests you may be financially stretched.

How to Use This Calculator

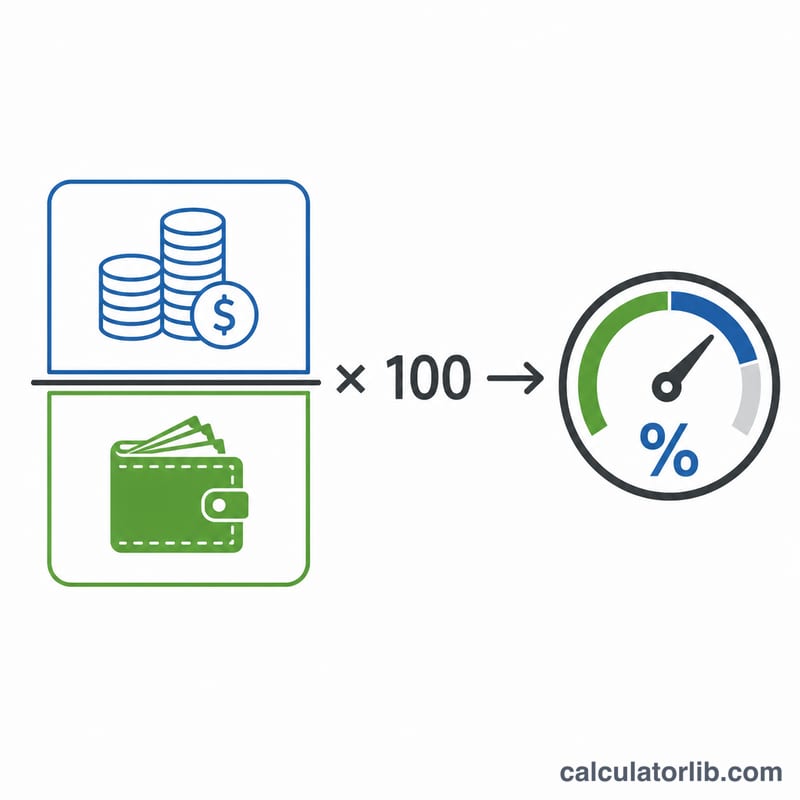

Add up all of your recurring monthly debt payments — mortgage or rent, car loans, student loans, credit card minimums, and personal loans — and enter the total in the first field. Then enter your gross (pre-tax) monthly income. The calculator divides your debt by your income and multiplies by 100 to produce your DTI percentage, along with a quick risk category.

The Formula Explained

The math is simple:

$$\text{DTI} = \left(\frac{\text{Total Monthly Debt Payments}}{\text{Gross Monthly Income}}\right) \times 100$$Because both figures are monthly amounts, the units cancel and you are left with a clean percentage that's easy to compare against lender guidelines.

Worked Example

Suppose your monthly debt payments total $1,500 and your gross monthly income is $5,000. Dividing 1,500 by 5,000 gives 0.30, and multiplying by 100 yields a DTI of 30%:

$$\text{DTI} = \left(\frac{1{,}500}{5{,}000}\right) \times 100 = 30\%$$That falls in the "healthy" range that most lenders view favorably.

FAQ

What is a good DTI ratio? Many lenders prefer a DTI of 36% or lower, though qualified mortgage rules often allow up to 43%. Below 35% is generally considered healthy.

Should I use gross or net income? Use gross income — your earnings before taxes and deductions — because that is what lenders use in their calculations.

Does rent count as debt? For most lender calculations, housing costs (rent or mortgage) are included in the front-end DTI. This calculator lets you include whatever monthly obligations you choose.