What This Calculator Does

The Mortgage Total Interest Calculator shows how much interest you will pay over the entire life of a fixed-rate loan. Many borrowers focus only on the monthly payment, but the cumulative interest can rival or even exceed the original loan amount on a long term. This tool reveals that hidden cost so you can compare loans, terms, and prepayment strategies.

How to Use It

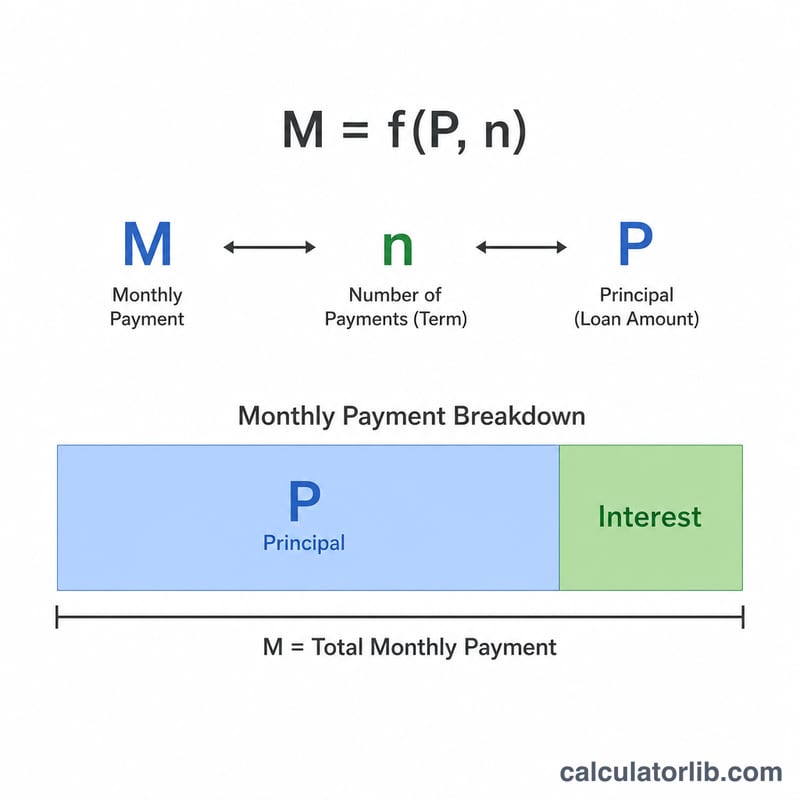

Enter three values: the loan amount (principal), the annual interest rate as a percentage, and the loan term in years. The calculator first computes the standard amortized monthly payment, then multiplies it by the total number of payments and subtracts the principal to reveal the total interest.

The Formula Explained

The monthly payment is $$M = P \cdot \frac{i\,(1+i)^{n}}{(1+i)^{n}-1}$$ where \(P\) is the principal, \(i\) is the monthly interest rate (annual rate \(\div 12 \div 100\)), and \(n\) is the number of monthly payments (years \(\times 12\)). Once \(M\) is known, the total interest is simply $$\text{Total Interest} = M \times n - P$$ — every dollar paid beyond the original loan balance is interest.

Worked Example

For a $300,000 loan at 6% for 30 years: the monthly rate is \(0.005\), \(n = 360\), and the monthly payment works out to about $1,798.65. Total of payments $$= 1{,}798.65 \times 360 \approx 647{,}514$$ so the total interest is roughly $347,514 — more than the amount borrowed.

Interpreting Your Total Interest Result

The total interest figure is the sum of every interest charge across all scheduled payments — it is what the loan costs you above and beyond the amount you actually borrowed. Comparing it to the principal gives the interest-to-principal ratio. A ratio of 0.5 means you pay 50 cents of interest for every dollar borrowed; a ratio above 1.0 means you pay more in interest than the home loan itself. In the table above, the 30-year loan at 7% has a ratio of about 1.40, while the 15-year loan at 5% sits near 0.42.

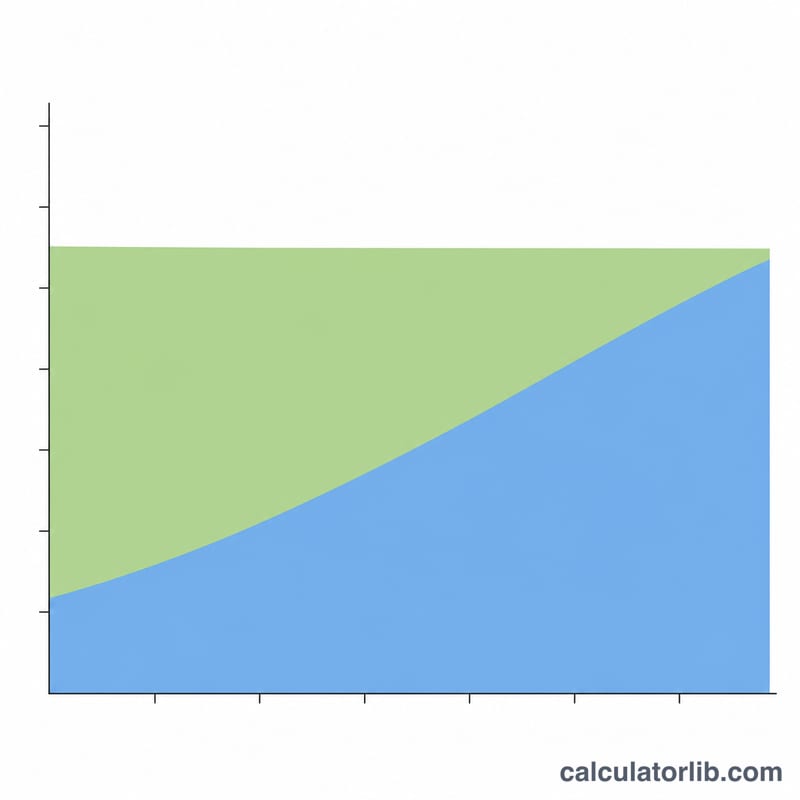

Long terms push interest higher for a simple reason: interest accrues on the outstanding balance every month, so the longer that balance stays large, the more total interest accumulates. Stretching repayment over 360 months instead of 180 keeps a high balance in place far longer, which is why total interest can exceed the original principal even at moderate rates.

Mortgages are also front-loaded with interest. Because each month's interest is the current balance times the monthly rate, the earliest payments are mostly interest and only a small slice goes to principal. As the balance falls, the interest portion shrinks and the principal portion grows, but the shift is gradual — in the first years of a 30-year loan the majority of each payment is interest. This is why making extra principal payments early, or choosing a shorter term, has an outsized effect on lifetime interest.

The total cost column (principal plus total interest) represents the full amount you would repay over the life of the loan if you make exactly the scheduled payments and never refinance or prepay. It does not include property taxes, homeowners insurance, mortgage insurance, closing costs, or fees — a payment calculator that includes taxes and insurance captures those separately. These figures are general illustrations of how loan math works and are not personal financial advice; consult a qualified professional for guidance on your own situation.

FAQ

Does this include taxes and insurance? No. It covers only principal and interest. Escrow items like property tax, homeowners insurance, and PMI are separate.

Why is the interest so high on long loans? Early payments are mostly interest. A longer term lowers the monthly payment but greatly increases lifetime interest.

How can I reduce total interest? Choose a shorter term, secure a lower rate, or make extra principal payments to shrink the balance faster.