What Is a Position Size Calculator?

A position size calculator tells you exactly how many shares (or units) to buy on a trade so that, if your stop-loss is triggered, you lose no more than a fixed, predetermined slice of your account. Position sizing is the single most important habit in risk management: it keeps a string of losing trades from wiping out your capital and removes emotion from how big each trade should be.

How to Use It

Enter four values: your total account size, the risk per trade as a percentage (most professionals use 0.5%–2%), your planned entry price, and your stop-loss price. The calculator returns the number of shares to buy, the dollar amount at risk, the risk per share, and the total capital the position will tie up.

The Formula Explained

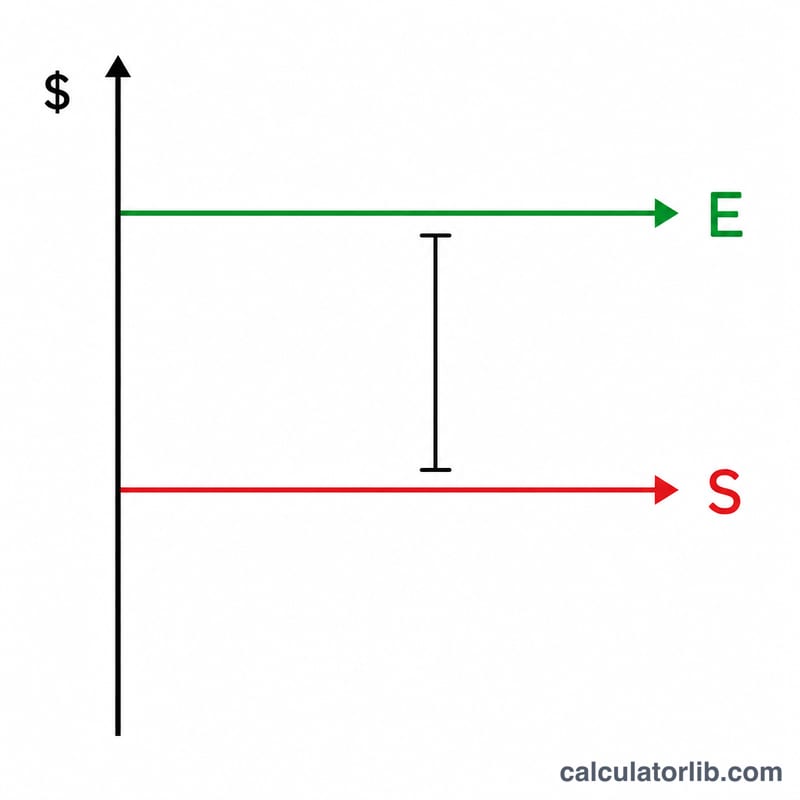

First, the dollar risk is your account multiplied by your risk percentage: \(\text{Risk Amount} = \text{Account} \times \dfrac{\text{Risk \%}}{100}\). Next, the risk per share is the distance between your entry and your stop-loss: \(\left|\,\text{Entry} - \text{Stop-Loss}\,\right|\). Dividing the dollar risk by the per-share risk gives the share count:

$$\text{Shares} = \dfrac{\text{Account} \times \dfrac{\text{Risk \%}}{100}}{\left|\,\text{Entry} - \text{Stop-Loss}\,\right|}$$

This works for both long and short trades because the absolute value handles either direction.

Worked Example

Suppose you have a $10,000 account and risk 1% per trade ($100). You plan to enter a stock at $50 with a stop-loss at $48, so your risk per share is $2. $$\text{Shares} = \dfrac{\$100}{\$2} = \textbf{50 shares}$$ That position costs \(50 \times \$50 = \$2{,}500\) to open, yet your maximum loss is held to just $100.

FAQ

What risk percentage should I use? Many traders cap risk at 1%–2% of account equity per trade to survive losing streaks.

Does this work for short selling? Yes. Enter the entry and stop-loss as you plan them; the formula uses the absolute price distance.

Does it account for fees or slippage? No. Commissions and slippage are not included, so consider risking slightly less to leave a buffer.