What is the ACB Term Deposit Maturity Calculator?

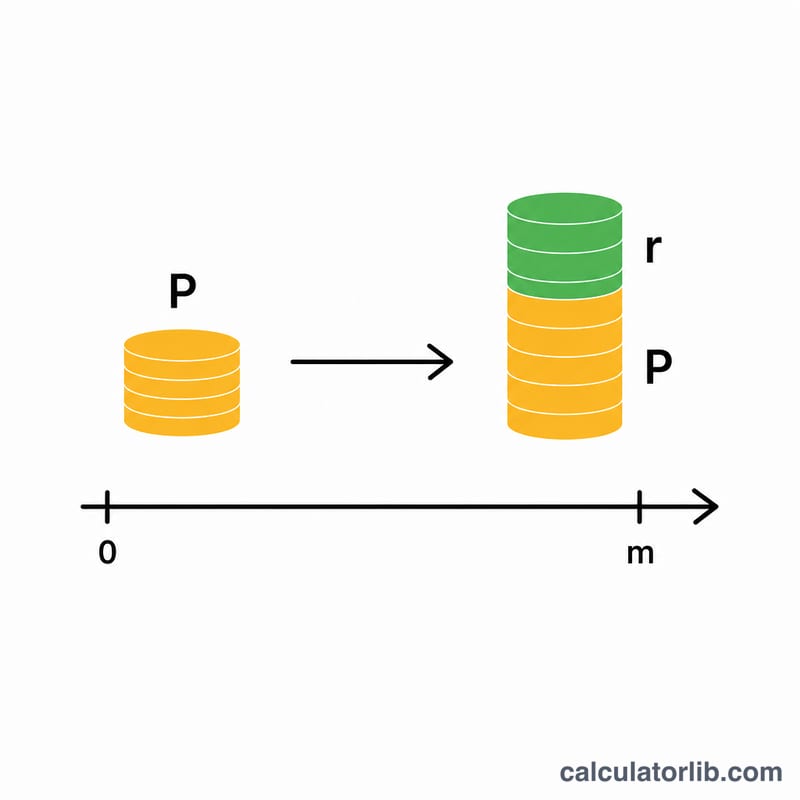

This calculator estimates how much a term deposit (also called a fixed deposit or time deposit) will be worth when it matures. It uses the simple-interest method, where interest is calculated only on the original principal over the agreed term. Enter your deposit amount, the quoted annual interest rate, and the term length in months to see both the total maturity value and the interest you will earn.

How to use it

Type the principal you intend to deposit, the bank's advertised annual percentage rate, and how many months your money will be locked away. The calculator instantly returns the maturity amount you will receive at the end of the term, along with the breakdown of principal versus interest earned.

The formula explained

The maturity value is given by $$\text{Maturity} = \text{Principal} \times \left(1 + \frac{\text{AnnualRate}}{100} \times \frac{\text{Months}}{12}\right)$$. The rate is divided by 100 to convert a percentage into a decimal, and the term in months is divided by 12 to express it in years. Multiplying these gives the fraction of a full year's interest, which is added to the principal.

Worked example

Suppose you deposit 10,000 at an annual rate of 5% for a 12-month term. $$\text{Interest} = 10{,}000 \times 0.05 \times \frac{12}{12} = 500$$ The maturity value is \(10{,}000 + 500 = 10{,}500\). If the same deposit ran for only 6 months, the interest would be $$10{,}000 \times 0.05 \times 0.5 = 250$$ giving a maturity value of \(10{,}250\).

Maturity Across Different Terms and Rates

The table below shows the simple interest earned and the total maturity value for a range of realistic ACB term deposit scenarios. All figures use the simple-interest formula \(\text{Maturity} = P\left(1 + \frac{r}{100}\cdot\frac{m}{12}\right)\), where \(P\) is principal, \(r\) is the annual rate in percent, and \(m\) is the term in months. Interest earned is simply \(\text{Maturity} - P\).

| Principal | Annual Rate | Term (months) | Interest Earned | Maturity Value |

|---|---|---|---|---|

| 10,000 | 4% | 3 | 100.00 | 10,100.00 |

| 10,000 | 5% | 6 | 250.00 | 10,250.00 |

| 10,000 | 6% | 12 | 600.00 | 10,600.00 |

| 10,000 | 6% | 24 | 1,200.00 | 11,200.00 |

| 50,000 | 4% | 6 | 1,000.00 | 51,000.00 |

| 50,000 | 5% | 12 | 2,500.00 | 52,500.00 |

| 50,000 | 6% | 12 | 3,000.00 | 53,000.00 |

| 50,000 | 6% | 24 | 6,000.00 | 56,000.00 |

Notice that with simple interest, doubling the term exactly doubles the interest earned (compare the 12- and 24-month rows), because no interest is paid on previously accrued interest.

Key Terms Explained

- Principal

- The original amount of money you place into the term deposit. It is the base on which interest is calculated and is returned to you in full at maturity.

- Annual interest rate

- The stated yearly rate of return expressed as a percentage. For a deposit shorter or longer than one year, the rate is scaled by the fraction of a year the deposit is held.

- Term (tenor)

- The length of time the deposit is locked in, here measured in months. Funds are generally not available for withdrawal without penalty before the term ends.

- Maturity value

- The total amount payable at the end of the term — principal plus all interest earned.

- Simple interest

- Interest calculated only on the original principal, not on accumulated interest. It grows linearly with time rather than exponentially.

- Fixed (term) deposit

- A deposit committed for a set period at an agreed rate. In exchange for locking the funds away, the rate is typically higher and fixed for the term.

- Withholding tax

- Tax that a bank may deduct from interest income at source before paying it to the depositor. The actual interest you receive can therefore be lower than the gross figure this calculator shows.

Understanding Your Maturity Result

The maturity value shown by this calculator is the gross amount: principal plus simple interest, before any tax or fees are applied. If your jurisdiction or the bank applies a withholding tax on interest income, the cash you actually receive will be reduced by that amount. Always check the deposit terms for any account fees as well.

This tool uses simple interest, meaning interest accrues only on the original principal. A deposit that instead pays compound interest reinvests earned interest, so over the same period it yields more — and the gap widens with longer terms and more frequent compounding. If your deposit credits and reinvests interest periodically, a tool such as the ACB Compound Interest Deposit Calculator or a general compound interest calculator will model it more accurately.

Finally, the figure here is a nominal return. Your real (purchasing-power) return depends on inflation over the term: if prices rise faster than your interest rate, the real value of your money can fall even though the nominal balance grows. A real return on deposit after inflation calculator can help you gauge that effect.

This is general information for understanding how the calculation works, not financial or tax advice. Confirm current rates, tax treatment, and terms with ACB before making a decision.

FAQ

Does this use simple or compound interest? It uses simple interest, which is the most common method for short fixed-term deposits where interest is paid at maturity.

Can I enter a term that is not a whole number of years? Yes. The term is measured in months, so any duration from 1 month upward is supported.

Is tax deducted from the result? No. The figure shown is the gross maturity value before any withholding tax or fees your bank may apply.