What is the real interest rate?

The real interest rate is the return you actually earn on a deposit or savings account once inflation is stripped out. A bank may quote a 5% nominal rate, but if prices rise 3% over the same period, your money only buys roughly 2% more goods than before. This calculator uses the exact Fisher equation to show your true purchasing-power return.

How to use this calculator

Enter the nominal interest rate offered on your deposit (the advertised annual rate) and the expected inflation rate over the same period. Both are entered as percentages. The calculator returns the real interest rate, plus the common quick approximation (nominal minus inflation) so you can compare the two methods.

The formula explained

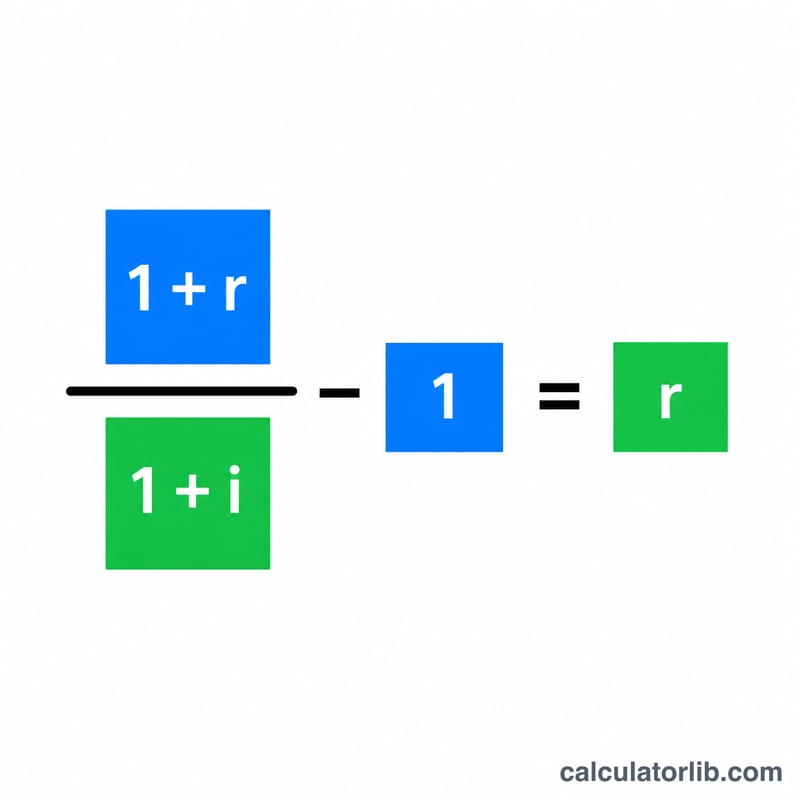

The exact relationship is:

$$\text{Real Rate} = \left( \frac{1 + \dfrac{\text{Nominal Rate (\%)}}{100}}{1 + \dfrac{\text{Inflation Rate (\%)}}{100}} - 1 \right) \times 100$$

Here the rates are expressed as decimals. Dividing the growth factor of your money (1 + nominal) by the growth factor of prices (1 + inflation) isolates the genuine gain in buying power. The simple subtraction nominal − inflation is a close approximation only when both rates are small.

Worked example

Suppose your deposit earns a nominal rate of 5% while inflation runs at 3%. The exact real rate is $$\left( \frac{1.05}{1.03} - 1 \right) = 0.019417,$$ or about 1.94%. The quick approximation gives \(5\% - 3\% = 2\%\). The small difference (0.06 percentage points) is exactly the error introduced by ignoring compounding between rates.

FAQ

Can the real rate be negative? Yes. If inflation exceeds your nominal rate, your real return is negative, meaning your savings lose purchasing power over time.

Why not just subtract inflation from the nominal rate? Subtraction is a handy estimate but slightly overstates the true real rate. The Fisher equation is exact and preferred for larger rates.

Should I use before-tax or after-tax nominal rates? For the most accurate picture of buying power, use the nominal rate after any tax on interest, since taxes reduce what you actually keep.