What Is the Effective Corporate Tax Rate?

The effective corporate tax rate (ETR) is the percentage of a company's pre-tax profit that it actually pays in income taxes. Unlike the statutory rate set by law, the effective rate reflects deductions, credits, deferred taxes, and other adjustments that reduce or increase the real tax burden. Analysts use it to compare profitability and tax efficiency across companies and over time.

How to Use This Calculator

Enter two figures from the income statement: the income tax expense (often labeled "provision for income taxes") and the pre-tax income (earnings before taxes, or EBT). The calculator divides the two and multiplies by 100 to give the effective rate as a percentage. It also shows your after-tax income for context.

The Formula Explained

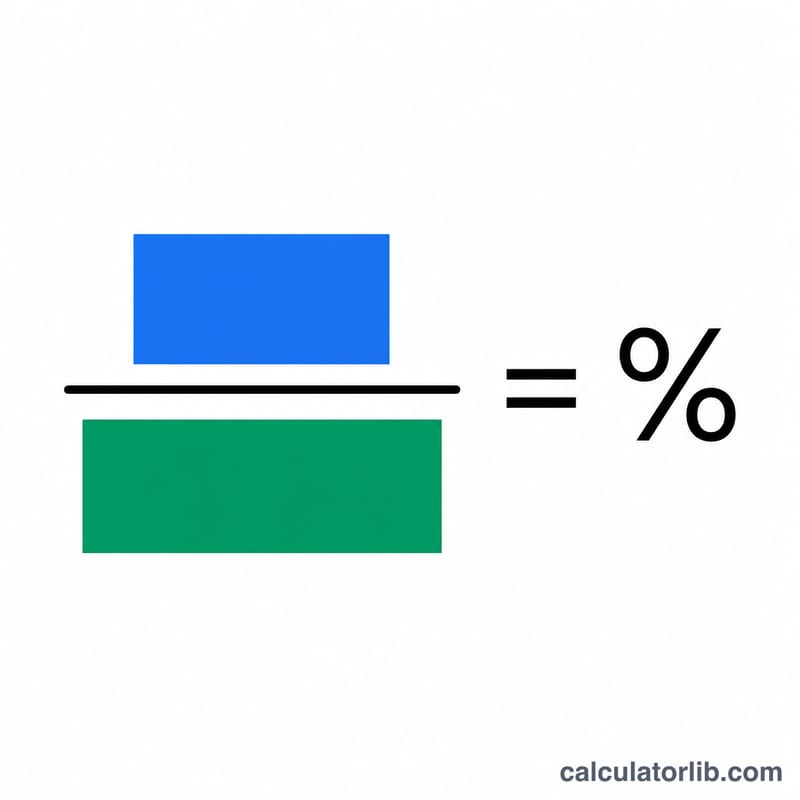

The calculation is simple:

$$\text{Effective Tax Rate} = \frac{\text{Income Tax Expense}}{\text{Pre-Tax Income}} \times 100\%$$

The income tax expense includes both current and deferred taxes reported on the income statement. Pre-tax income is revenue minus all operating and non-operating expenses except taxes.

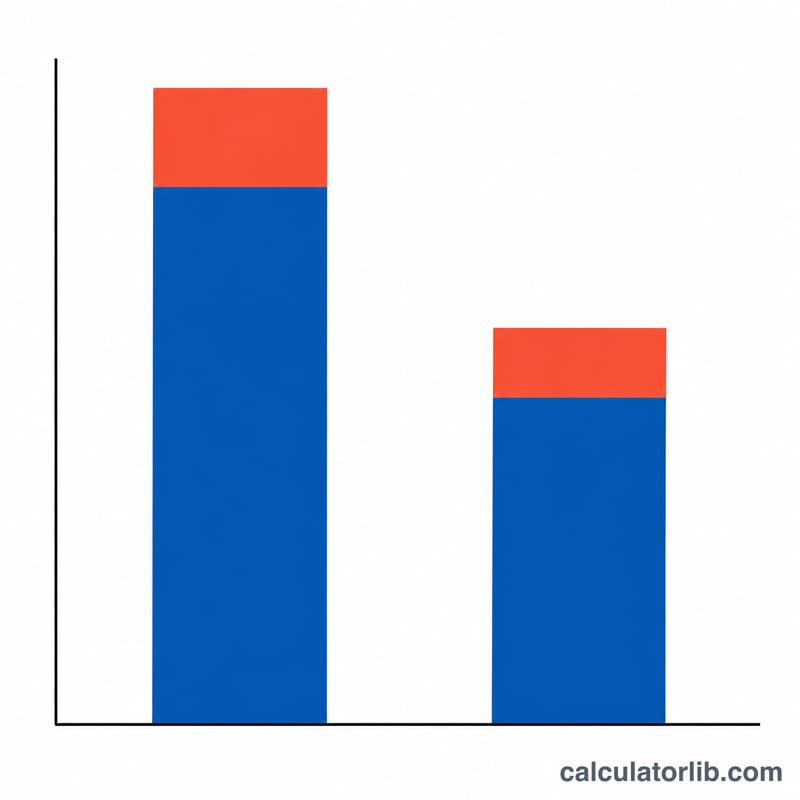

Worked Example

Suppose a company reports pre-tax income of $1,000,000 and an income tax expense of $210,000. The effective tax rate is:

$$(\$210{,}000 \div \$1{,}000{,}000) \times 100 = \textbf{21\%}$$

After-tax income would be \(\$1{,}000{,}000 - \$210{,}000 = \$790{,}000\).

FAQ

Why does the effective rate differ from the statutory rate? Tax credits, accelerated depreciation, foreign income taxed at lower rates, and deferred tax adjustments all cause the effective rate to diverge from the headline statutory rate.

Where do I find these numbers? Both appear on a company's income statement; pre-tax income is the line before the tax provision, and the tax expense is the provision itself.

Can the effective rate be negative? Yes — if a company records a net tax benefit (e.g., from loss carryforwards) it can show a negative effective rate.