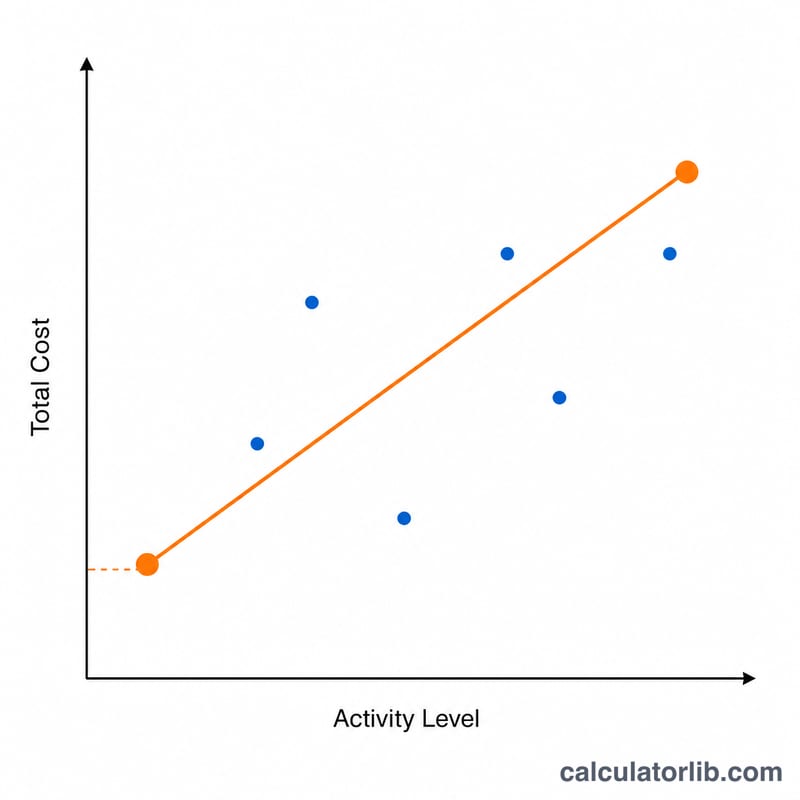

What Is the High-Low Method?

The high-low method is a cost accounting technique used to split a mixed (semi-variable) cost into its variable and fixed components. It uses only two data points — the period with the highest activity and the period with the lowest activity — making it a quick way to estimate a cost equation of the form Total Cost = Fixed Cost + (Variable Cost per Unit × Activity).

How to Use This Calculator

Enter the activity level (units, hours, machine time, etc.) and the total cost for both your highest-activity and lowest-activity periods. The calculator returns the variable cost per unit, the estimated fixed cost per period, and a check of the total cost equation at the high point.

The Formula Explained

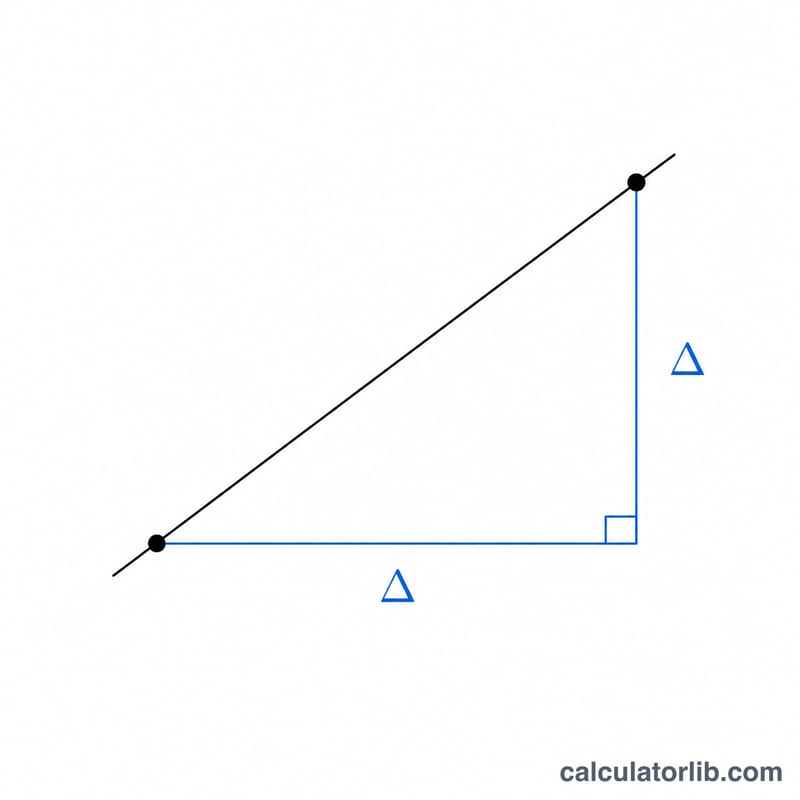

First, the variable rate is found by dividing the difference in cost by the difference in activity: (High Cost − Low Cost) ÷ (High Units − Low Units). This isolates the cost that changes with activity. Then the fixed cost is found by subtracting the variable portion from total cost at either point: Fixed Cost = Total Cost − (Variable Cost per Unit × Units). Both the high and low points should yield the same fixed cost.

$$V = \frac{\text{High Cost} - \text{Low Cost}}{\text{High Units} - \text{Low Units}}$$

$$\text{where}\quad \left\{ \begin{aligned} V &= \text{Variable Cost per Unit} \\ F &= \text{High Cost} - V \cdot \text{High Units} \end{aligned} \right.$$

Worked Example

Suppose at high activity you produced 1,200 units costing $9,000, and at low activity 400 units costing $5,000. Variable cost per unit =

$$V = \frac{9{,}000 - 5{,}000}{1{,}200 - 400} = \frac{4{,}000}{800} = \$5.00 \text{ per unit}$$Fixed cost =

$$F = 9{,}000 - (5.00 \times 1{,}200) = 9{,}000 - 6{,}000 = \$3{,}000 \text{ per period}$$The cost equation is therefore Total Cost = $3,000 + $5.00 × units.

FAQ

Why only two data points? The method is intentionally simple. It trades precision for speed, ignoring all intermediate observations.

What are its limitations? Because it relies on the extreme points, outliers or unusual periods can distort the estimate. Regression analysis is more accurate for noisy data.

Can activity be hours instead of units? Yes — activity can be any cost driver such as labor hours, machine hours, or miles, as long as cost and activity are measured consistently.