What is the effective interest rate with a compensating balance?

When a bank grants a loan but requires the borrower to keep a restricted deposit (a "compensating balance") at the same institution, the borrower does not actually get the full use of the borrowed money. Part of it is locked up as a low-yield deposit. As a result, the true cost of the funds you can actually use is higher than the nominal loan rate. This calculator returns both the nominal loan rate and the effective rate so you can see the difference clearly.

How to use it

Enter four amounts, all measured over the same time period and all in the same currency unit (the original Japanese tool uses 10,000-yen units, but any consistent unit works because it cancels in the ratio): the loan interest charged, the average loan balance, the deposit interest earned, and the average restricted deposit balance. Pick the matching period from the dropdown for context. The calculator outputs the nominal loan rate and the effective interest rate on your net usable funds.

The formula explained

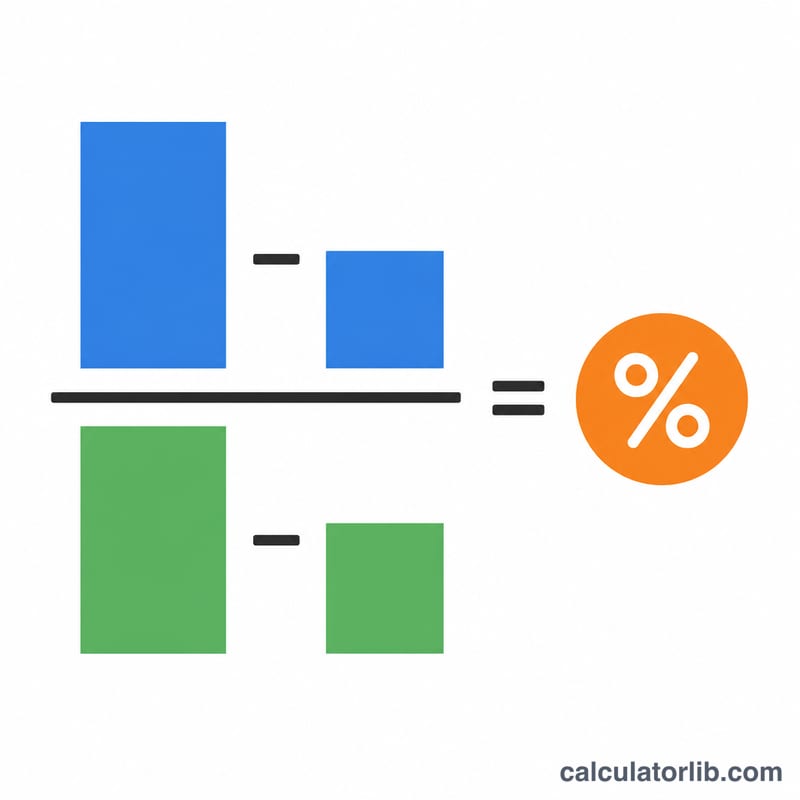

The effective rate measures net interest cost against net usable funds:

$$\text{Effective Rate} = \frac{\text{Loan Interest} - \text{Deposit Interest}}{\text{Loan Balance} - \text{Deposit Balance}} \times 100\%$$

You really pay (loan interest minus the interest you earn back on the deposit), and you really have access to only (loan balance minus deposit balance). Dividing one by the other gives the true cost. The nominal loan rate is simply \(\text{Loan Interest} / \text{Loan Balance} \times 100\).

Worked example

Suppose loan interest = 100, loan balance = 5000, deposit interest = 1, and deposit balance = 2000 over one year. The nominal loan rate is \(100 / 5000 \times 100 = 2.0\%\). But the effective rate is $$\frac{100 - 1}{5000 - 2000} \times 100 = \frac{99}{3000} \times 100 = 3.30\%.$$ Although the headline rate is 2.0%, locking up 2000 of the 5000 borrowed as a low-yield deposit raises the real cost of the usable 3000 to 3.30%.

FAQ

Does the period annualize the rate? No. The result is the rate over the period you entered. With the default 1-year period it already reads as an annual rate. To annualize a shorter period, multiply by \(12 / \text{months}\).

Why is the effective rate higher than the nominal rate? Because tying up funds at a deposit yield lower than the loan rate raises the net cost of the money you can actually use.

What if the deposit balance equals or exceeds the loan balance? Then net usable funds are zero or negative and the effective rate is undefined; the calculator shows a notice instead of a number.