What Is the Nominal to Effective Interest Rate Calculator?

This tool converts a nominal annual interest rate (often quoted as an APR) into the effective annual interest rate (APY). The nominal rate is the simple yearly rate stated on a loan or savings product, but it ignores how often interest is compounded. The effective rate reflects the true cost or return once compounding is taken into account, making it the fairest figure for comparing different products.

How to Use It

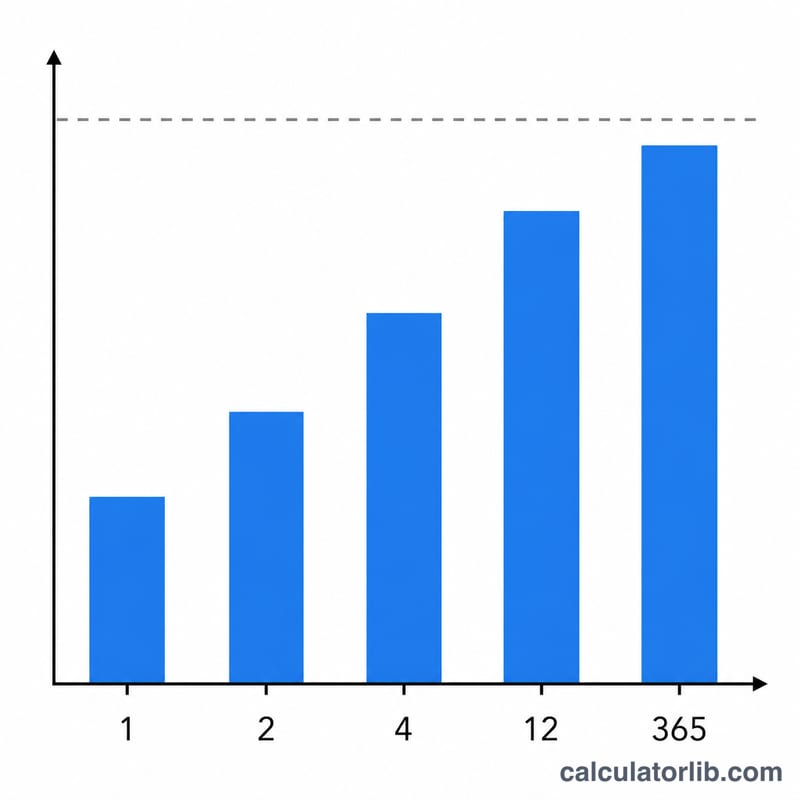

Enter the nominal annual rate as a percentage, then pick how often interest compounds during the year — annually, semi-annually, quarterly, monthly, weekly or daily. The calculator instantly returns the effective annual rate and shows how much extra the compounding adds on top of the nominal figure.

The Formula Explained

The effective rate is found with:

$$i_{eff} = \left(1 + \frac{i_{nom}}{m}\right)^{m} - 1$$Here i_nom is the nominal rate expressed as a decimal (6% = 0.06) and m is the number of compounding periods per year. Dividing by m gives the periodic rate; raising to the power of m compounds it across the year; subtracting 1 strips out the original principal to leave the pure growth rate.

Worked Example

Suppose a credit card quotes a nominal rate of 6% compounded monthly (\(m = 12\)). Then $$i_{eff} = \left(1 + \frac{0.06}{12}\right)^{12} - 1 = (1.005)^{12} - 1 \approx 0.061678,$$ or about 6.1678%. The monthly compounding adds roughly 0.17 percentage points over the stated 6%.

FAQ

What is the difference between APR and APY? APR is the nominal rate without compounding; APY is the effective rate that includes compounding. APY is always equal to or greater than APR.

Why does more frequent compounding raise the effective rate? Because interest earned (or charged) starts earning interest sooner, so the more often it compounds, the higher the effective rate.

What if compounding is annual? When \(m = 1\), the nominal and effective rates are identical, since there is no intra-year compounding.